A stagflationary shock, but of what magnitude and for how long?

Link

What are the key takeaways from the market news on March 27, 2026? Xavier Chapard provides some insights.

Overview

► As we approach the end of the fourth week of the war in Iran (the U.S. administration had indicated 4–5 weeks), uncertainty remains extremely high regarding what matters for global markets, i.e., the duration and magnitude of the energy shock. Will we know more after this weekend—either because the escalation reaches a new level or because de-escalation begins? Nothing is less certain.

►Indeed, D. Trump extended by 10 days the deadline he had announced on Monday for negotiating before resuming strikes on Iranian energy infrastructure, which was originally set to end tomorrow. According to the U.S. administration, advanced negotiations toward a deal with Iran are underway, and Vice President Vance was expected to take part in the talks this weekend. This suggests a U.S. willingness to find a swift exit strategy. But at the same time, the United States is maintaining the threat of a ground intervention by sending thousands of elite troops to the region, which would mark a significant escalation. And let us hope that the postponement of Trump’s trip to China from late March to mid-May does not reflect a newly anticipated duration of the conflict on the American side.

►At the same time, Iran continues to deny any negotiations and has put forward very tough conditions for accepting a cease-fire (including security guarantees against a new Israeli‑American attack, war reparations, an end to attacks on Lebanon, and recognition of Iran’s authority over the Strait of Hormuz). But pressure from China and India on Iran to allow oil to flow toward Asia is increasing.

►Under these conditions, markets were very volatile but directionless this week after their sharp decline last week. For risk assets, which have fallen significantly but have not overreacted given the scale of the shock and the prevailing uncertainty, the potential for both upside and downside remains substantial. We remain relatively optimistic over the medium term, given our scenario of de‑escalation after a few weeks of conflict and a decline in energy prices during the second quarter. However, the risks of a much more negative scenario remain significant.

Conversely, we believe that the levels reached by interest rates offer opportunities, especially after markets priced in much more restrictive monetary policies following last week’s central bank meetings. A de‑escalation would reduce inflationary risks and the likelihood of substantial policy rate increases, whereas a further escalation would heighten recession risks and increase demand for safe‑haven assets. And markets have already priced in rapid and forceful central bank reactions following last week’s meetings.

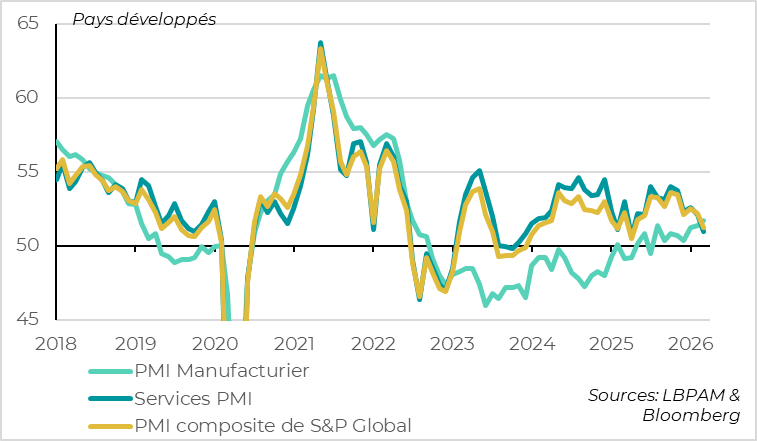

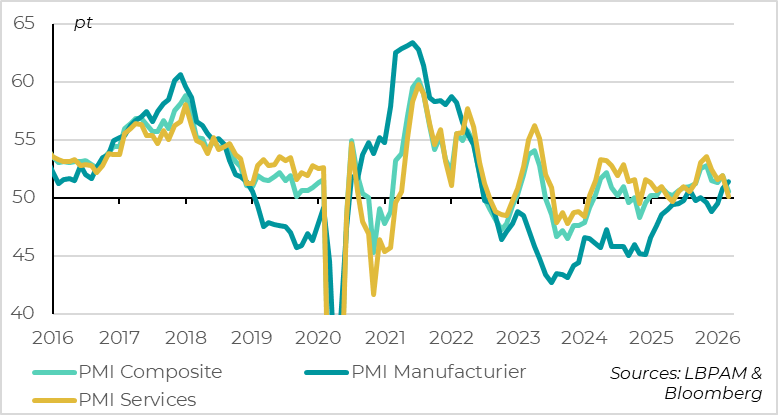

►The first surveys for March confirm the stagflationary nature of the shock—significant, but not yet decisive for the cycle. Indeed, PMIs have fallen slightly more than expected in developed countries, down 1 point to 51.2, and leading components are trending unfavorably, even if they are declining less than at the start of the war in Ukraine. At the same time, cost and price indicators are rising sharply, and signs of strain in production chains are already emerging.

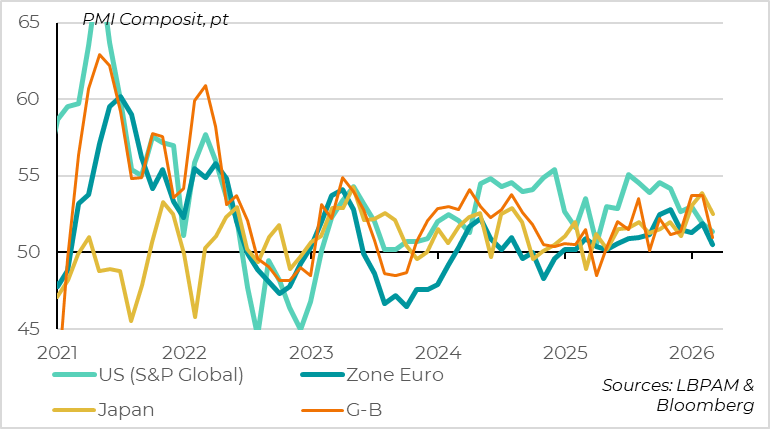

►At the country level, the shock is particularly severe for Europe, which is not surprising given the region’s oil and gas imports. The Eurozone PMI fell from 51.9 to 50.5, its lowest level since the announcement of U.S. tariffs last spring, even though it remains just within expansion territory. Price indicators increased sharply, reaching their highest levels in two years, confirming the delicate position in which the ECB finds itself—facing upside risks to short‑term inflation, but clearly downside risks to economic prospects. This may be one of the reasons why Christine Lagarde struck a slightly less hawkish tone this week when she said that the ECB would wait to gather sufficient information on the shock before taking action.

►The decline in cyclical indicators is more limited in the United States, with the S&P Global PMI slipping from 51.9 to 51.4 and jobless claims remaining low in mid‑March. But the U.S. economy is not immune, as price indicators have also accelerated sharply. This reduces the Fed’s ability to cut rates in the short term, even if its incoming chair wished to do so.

Going further

World: Early signs of a sharp slowdown in activity in March

PMIs in developed countries fell sharply in March, particularly in services

The preliminary PMIs for March—the first since the start of the war in Iran and the energy shock—confirm the very negative impact on global growth, even though activity is still holding up for now.

The composite PMI for developed countries fell by 1 point in March to 51.2. It remains above the 50‑point threshold that separates expansion from contraction in private‑sector activity, but it is at its lowest level since the announcement of reciprocal tariffs last April. And the leading indicators (confidence, orders, etc.) are pointing in the wrong direction for April.

By sector, the loss of momentum comes from services, whose PMI dropped to 50.9, falling back below the manufacturing PMI for the first time since the post‑Covid rebound. Rising energy costs are weighing on household purchasing power, and weak confidence is prompting consumers to cut discretionary spending.

The manufacturing PMI, by contrast, rose slightly by 0.3 points to 51.7, its highest level since mid‑2022. It may seem surprising that industry is holding up, as it is normally more cyclical than services. But this is not unusual during supply‑side shocks, which tend to encourage firms to bring forward purchases of goods and build up inventories before prices rise and supply chains become disrupted. There is little doubt that the manufacturing PMI will fall much more sharply in the coming months if the energy shock does not subside quickly.

The decline in PMIs is broad‑based, but more pronounced in Europe

PMIs declined in March across all major developed economies. But the drop is particularly pronounced in Europe, which is especially exposed to the rise in energy costs. The Eurozone PMI fell from 51.9 to 50.5, and the UK PMI dropped from 53.7 to 51. Japan is also highly exposed—especially as it imports even more energy from the Middle East than Europe—but it had been benefiting from a stronger cyclical recovery earlier in the year. Its PMI therefore fell from 53.9 to 52.5.

U.S. indicators held up somewhat better in March

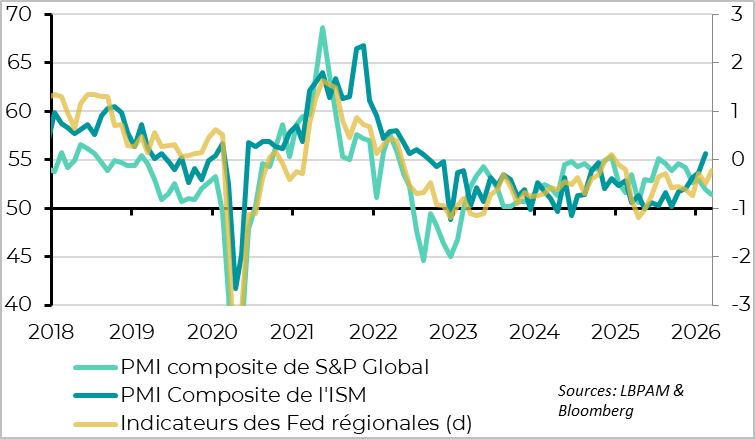

The U.S. PMI published by S&P Global also declined in March, but to a lesser extent. The composite PMI fell from 51.9 to 51.4. This is its lowest level since last spring, but it remains in expansion territory, and leading indicators are holding up better than in the rest of the world (with stable orders and business confidence). This resilience in activity, at least in early March, also appears to be confirmed by regional surveys. This suggests that the recessionary impact of the energy shock is less severe in the United States than in Europe or Asia, although it is unlikely to be absent if the shock persists.

Moreover, as was the case following the 2025 trade shock, this resilience comes at the cost of rising inflationary pressures. U.S. firms report that their input costs are increasing at a pace similar to last spring—after tariff hikes—and that they are raising selling prices at the fastest rate since mid‑2022. Since inflation was already too high before March, this heightens the risk that inflation will remain above target even if the energy shock fades relatively quickly.

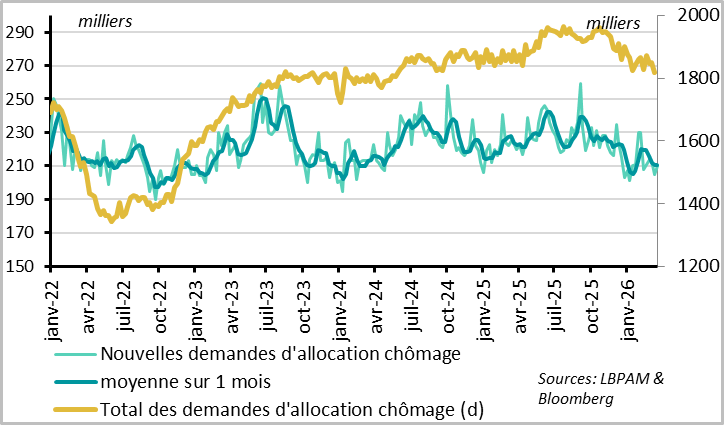

And the U.S. labor market remains stable

On the employment front, weekly jobless claims remained very low in mid‑March, which is reassuring after February’s weak official employment figures and the start of the war against Iran in early March. New unemployment claims remain well below their level of last year, indicating that layoffs are still limited. And continuing claims declined again in mid‑March, falling back below their level prior to the trade war, suggesting that the unemployment rate should not rise sharply in the short term.

The more inflationary than recessionary impact of the energy shock on the United States, combined with signs of stability in the labor market, should reinforce the Fed’s caution before considering further rate cuts in the coming quarters.

Eurozone: More inflation, but above all less activity

Activity stagnates in services in March

The Eurozone PMI fell from 51.9 to 50.5 in March, suggesting barely positive growth for the month (between 0% and 0.1% quarter‑on‑quarter according to our models). This decline—which brings the PMI back to its May level—comes from the services sector, which stagnated in March (at 50.1). In contrast, the manufacturing PMI increased, as in other regions. At 51.4, it is even at its highest level since mid‑2022 and the previous energy shock. But the outlook is worsening markedly in both sectors, with industrial orders falling back into contraction territory and the sharpest drop in business confidence since the start of the war in Ukraine.

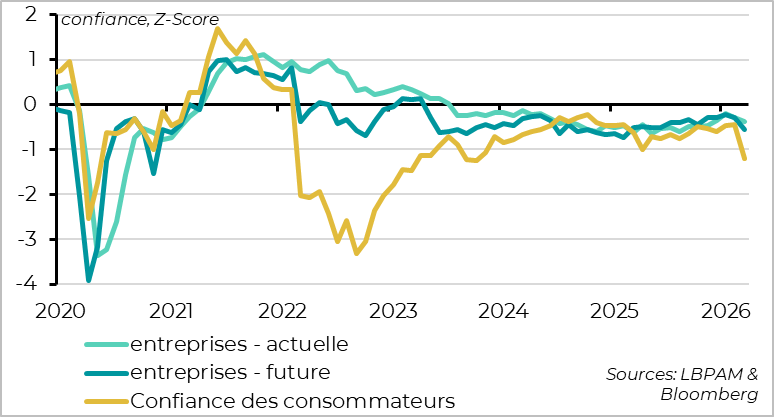

Confidence drops sharply but less than in early 2022

Household confidence also fell sharply in March, reaching its lowest level since 2023. This confirms the very negative impact of the energy shock and the uncertainty surrounding the Eurozone’s activity outlook, even though national business surveys (IFO, INSEE) suggest that activity was still holding up in March. It is worth noting, however, that the scale of the confidence shock is far smaller than at the beginning of the war in Ukraine—thankfully.

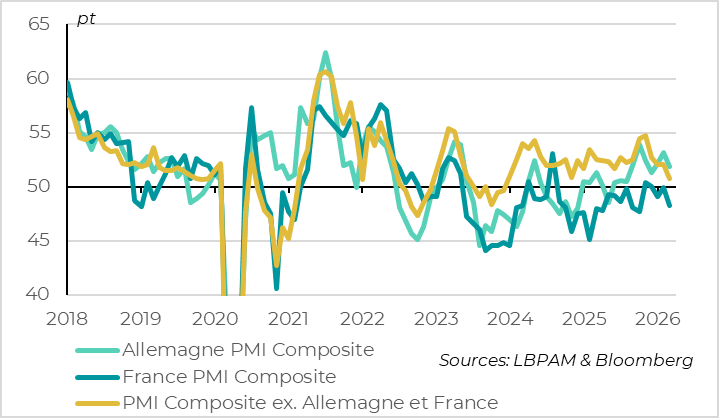

The decline in PMIs is widespread and is also affecting the southern Eurozone

Across countries, the decline in Eurozone PMIs is broad‑based. The French PMI has clearly fallen back into contraction territory after oscillating around 50 in recent months. The German PMI is declining from higher levels, supported until recently by the surge in public spending since late last year. Finally, the PMI for the rest of the Eurozone has fallen to its lowest level since 2023, showing that Spain and Italy are particularly exposed to the risk of an energy shock. This is why the governments of these countries acted quickly by announcing fiscal support measures to limit the impact of rising fuel prices.

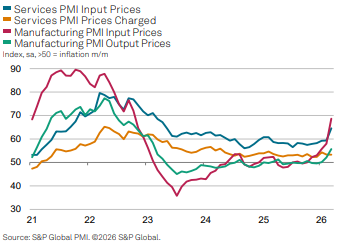

Costs are accelerating sharply, while selling prices are rising more moderately

Alongside the negative energy shock, the March PMIs confirm a sharp increase in price pressures—something that will not reassure the ECB. Input costs for firms (including energy) are rising rapidly as early as March, in both manufacturing and services, reaching their highest level since early 2023. This is pushing companies to raise their selling prices, which overall are increasing at the fastest pace since early 2024.

However, selling‑price increases remain much more limited than the surge in input costs, particularly in the services sector, which reflects domestic pricing power. This suggests that firms are absorbing a larger share of the cost increases in their margins to avoid discouraging demand—reducing the risk of second‑round effects and persistent inflation after the energy shock. This is consistent with our view that conditions are less conducive to a sustained rise in inflation than in 2022 in the Eurozone, and that the ECB should therefore avoid raising rates too aggressively in this context.

Xavier Chapard

Strategist