According to D. Trump, the war is coming to an end

Link

What are the key takeaways from the market news on march 10, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► The war in Iran continues and has now spread to other countries in the region. The fighting, marked in particular by mutual bombardments between the United States–Israel coalition and Iran, goes on. While coalition strikes remain intense, the U.S.–Israeli strategy appears to have slightly shifted, now targeting not only military objectives but also civilian infrastructure, especially those related to water and oil supply.

►At the same time, the Iranian authorities have appointed Mojtaba Khamenei to replace his father, Ali Khamenei—who was killed last week—as Supreme Leader. Little known, Mojtaba Khamenei is considered a supporter of the hard‑line faction of the Islamist regime. His appointment highlights how difficult a rapid regime change in Iran would be. On the contrary, backed by the Revolutionary Guards, the regime appears determined to hold on to power. Messages from the new leaders also indicate their intention to continue the war by targeting American interests throughout the region.

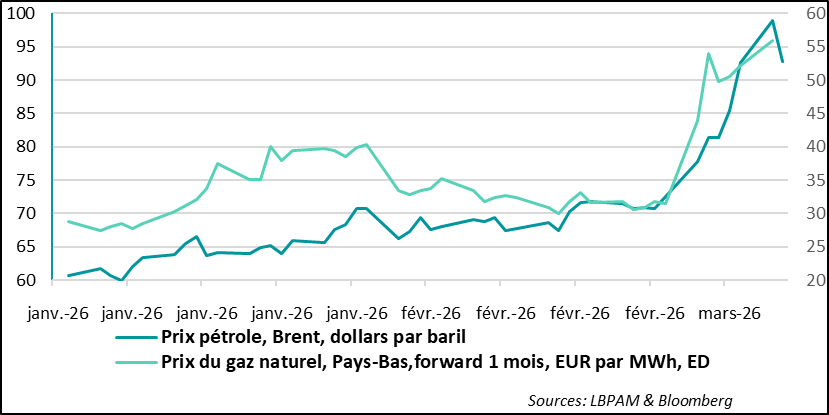

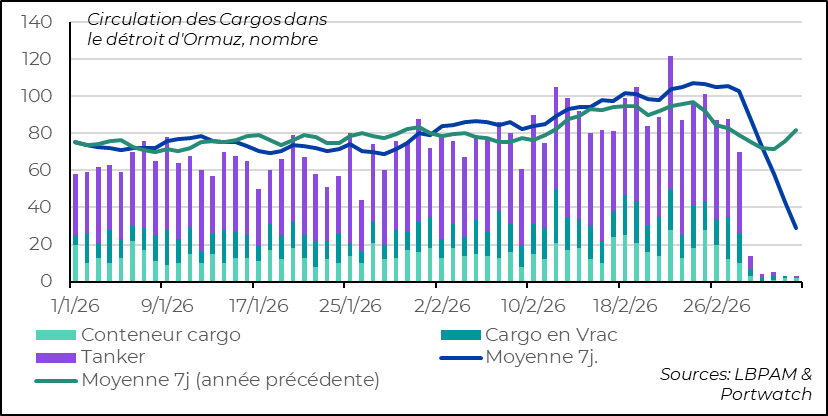

►This situation has already led to a sharp rise in oil prices, which exceeded 100 dollars yesterday morning. This is partly due to the almost total closure of the Strait of Hormuz, where hardly any ships have been circulating for several days. A prolongation of the conflict could further increase pressure on prices.

►Moreover, the U.S. strategy remains unclear, despite President Trump’s rhetorical escalation over the weekend, calling for Iran’s total capitulation. Surprisingly, Donald Trump stated last night that ‘the war was almost over’ and that the U.S. ‘excursion’ would be very brief. According to him, Iran ‘no longer has a navy, no communications, no air force.’ However, shortly after these remarks, the U.S. president clarified during a press conference that the war would end soon, but not this week.

►The initial statements from the U.S. president quickly boosted risk appetite: U.S. stocks rebounded sharply to end the session higher, while long-term interest rates and oil prices both fell, with Brent dropping below 90 dollars per barrel. This movement was also supported by announcements from several major countries seeking to mitigate rising energy prices, either through subsidies or by increasing supply using their strategic reserves.

►Overall, D. Trump’s remarks do not provide any additional short‑term clarity, even though they could signal a limited tolerance from the U.S. president toward a major economic shock. In any case, as long as the conflict persists, the oil market will remain under pressure, leading to a direct negative impact on growth in most countries. Nevertheless, we maintain a central scenario that factors in a limited shock lasting one or two months, without an extreme and lasting increase in oil prices above 100 dollars per barrel.

►However, the possibility of a more adverse scenario leads us to remain cautious. After the sharp rise in long‑term interest rates, both in the United States and in Europe, we have become more constructive on sovereign bonds.

►As already mentioned in previous publications, one of the factors allowing economies to withstand the energy shock lies in the current growth momentum. In this respect, while the U.S. economy appears to remain robust, as shown by the latest ISM surveys—particularly in services—consumer spending has lost some momentum. This was confirmed by slightly disappointing retail sales figures in January, even though they were affected by adverse weather conditions at the end of the month.

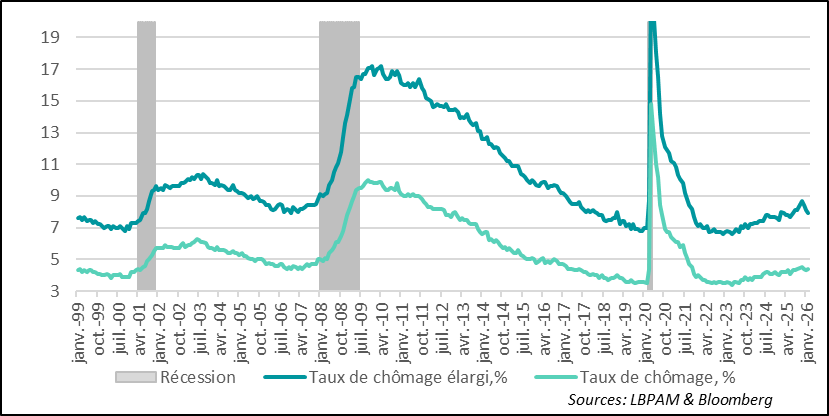

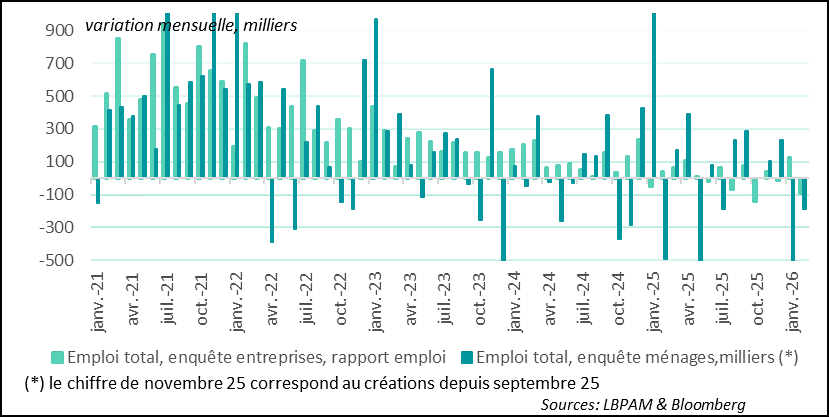

►Moreover, while we had expected the labor market to extend its January rebound, the February employment report delivered a very disappointing message, with 92,000 jobs lost this month. The unemployment rate rose to 4.4%. This shows that companies remain very cautious. A resumption of hiring is essential to support consumption and ensure continued growth. The only positive point is that wages continued to increase, slightly above inflation, thereby improving workers’ purchasing power. But the current energy shock is likely to weigh on household spending in March.

Going Further

War in the Middle East: Rising Tensions

A pause in rising oil and gas prices

The war in the Middle East continues, keeping pressure on oil and gas prices. Nevertheless, last night, President Trump surprised everyone by suggesting that the war in Iran was nearing its end. He notably stressed that the country ‘no longer had a navy, no communications, no air force.’ At the same time, recently mentioned objectives such as regime change or the country’s total capitulation were no longer referenced. Overall, the U.S. president delivered a message that seems to indicate a more limited tolerance for a major economic shock linked to rising energy prices.

From a military standpoint, recent Israeli and American bombings have shifted toward the destruction of the country’s infrastructure beyond strictly military targets. Water production facilities and oil storage tanks have been hit, further weakening the country.

Meanwhile, Iran’s new leadership remains dominated by the regime’s hardest-line positions, notably with the appointment of Ali Khamenei’s son as Supreme Leader. As a result, Iranian drone attacks across the region have continued, even though their intensity appears to have decreased.

The Strait of Hormuz, vital for oil and gas transportation, remains blocked

This situation is keeping the Strait of Hormuz blocked for now. Indeed, statistics compiled by the IMF with the support of Oxford University show that almost no cargo ships are transiting through the area. Naturally, a rapid end to the conflict would allow a fairly quick return to normal conditions. In contrast, the proposal to escort cargo ships with military forces would not realistically restore smooth traffic any time soon.

Meanwhile, proposals aimed at mitigating the energy shock are multiplying around the world, ranging from the deployment of OECD countries’ strategic oil reserves to the introduction of new national support measures for households. On this last point, it is clear that many countries’ fiscal positions have deteriorated so significantly in recent years that room for maneuver remains limited.

We believe that in the short term, uncertainty will remain high before any potential end to the conflict becomes visible. At the same time, D. Trump’s statements yesterday seem to indicate a more limited tolerance for a severe economic shock, contrary to what his very hawkish comments in recent days might have suggested. This aligns with our scenario of a relatively short conflict, lasting no more than one to two months. As a result, the negative shock on global growth would remain contained.

However, at this stage, it is still too early to completely rule out the most adverse scenarios. This is why we remain cautious in the very short term. In the meantime, given the very sharp recent rise in long‑term interest rates, we have become somewhat more constructive on sovereign bonds on both sides of the Atlantic.

United States: Employment remains weak and could weigh on consumption

The unemployment rate rises again in February

As we have emphasized in previous publications, the ability of economies to withstand the energy shock—even if it proves short‑lived—will also depend on the current economic momentum. In this regard, the PMI surveys at the beginning of the year were reassuring and pointed to resilient activity. In the United States in particular, the latest ISM services survey sent a very positive signal.

At the same time, this positive message from businesses continues to contrast with the situation in the U.S. labor market. Indeed, the February employment report was very disappointing, with significant job losses and, above all, another increase in the unemployment rate, which has risen to 4.4%. In contrast, the underemployment rate, or broad unemployment measure, continued to decline, which may be explained by a decrease in the participation rate and a sharp drop in temporary jobs.

Sharp job losses in February

The job losses (–92,000) affected almost all sectors, including healthcare, which had until now been the most dynamic. However, in this sector, the figures were heavily distorted by strikes that have now ended. Moreover, adverse weather conditions likely amplified the weakness of these results. The decline in employment is also visible in both surveys—household and establishment—confirming the breadth of the downturn.

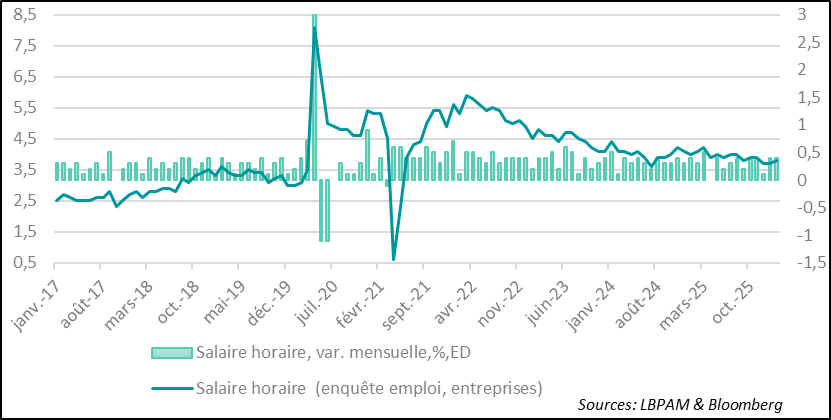

Wages remain resilient

The only positive point in the employment report was the trend in wages. Indeed, pay continued to increase in February at a pace exceeding inflation, which is supportive of purchasing power. However, it will be necessary to wait for the next wage statistics to confirm this trend. If this signal is confirmed, it would represent a positive factor for consumption.

Nevertheless, for the U.S. economy to remain resilient, it is essential for the labor market to recover, which would help improve confidence among both households and businesses.

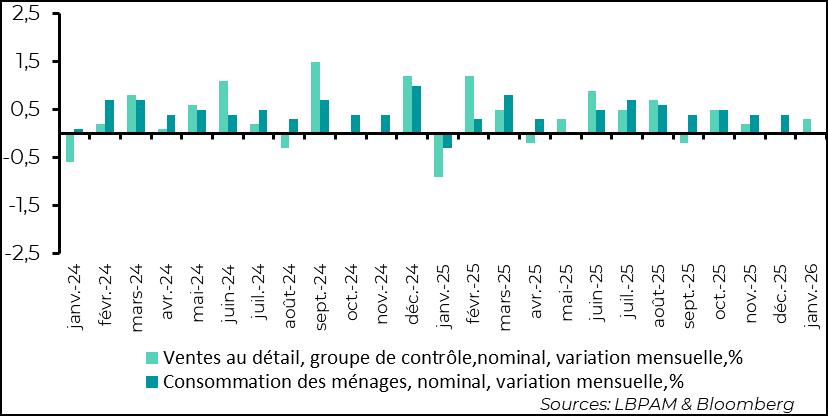

Consumption has lost some of its strength

An improvement in labor market dynamics is essential to support consumption and growth. In this respect, the January retail sales figures showed that consumer appetite remained less robust than in the middle of last year. The expected energy shock in March is unlikely to improve the situation. As a result, growth at the beginning of this year is likely to be slightly weaker than previously anticipated, without, at this stage, fully calling into question the positive outlook for the rest of the year—assuming a normalization of the geopolitical situation and energy prices.

Sebastian Paris Horvitz

Director of Research