After the relief brought by the ceasefire, Hormuz must reopen quickly

Link

What should we take away from market developments on April 24, 2026?

Insights from Xavier Chapard.

Overview

► Despite the extension of the ceasefire in Iran, the absence of new negotiations and, above all, the fact that Hormuz remains blocked by both sides (with Iran keeping the Strait closed and the United States maintaining the blockade) are leaving investors in a wait‑and‑see mode. With oil prices climbing back above $100 a barrel for the first time in two weeks, markets are slightly consolidating this week after their strong post‑ceasefire rebound.

►Our central scenario remains one of de‑escalation and a gradual reopening of Hormuz starting in the coming weeks, as it is in the interest of both sides, which appear to be seeking an acceptable exit strategy. In this case, the energy shock would have a significant impact around mid‑year but would not derail the economic cycle. With the Fed inclined not to react to higher energy‑driven inflation, substantial fiscal stimulus, and corporate earnings that have been fairly solid so far, we remain rather positive on markets over the medium term.

►That said, markets have quickly priced in de‑escalation and adjusted their positioning, which is no longer underweight risky assets. However, economic fundamentals deteriorate a little more each day that Hormuz remains closed, with rising risks of shortages if the situation were to persist for more than a few weeks. We therefore believe that caution is once again warranted in the short term.

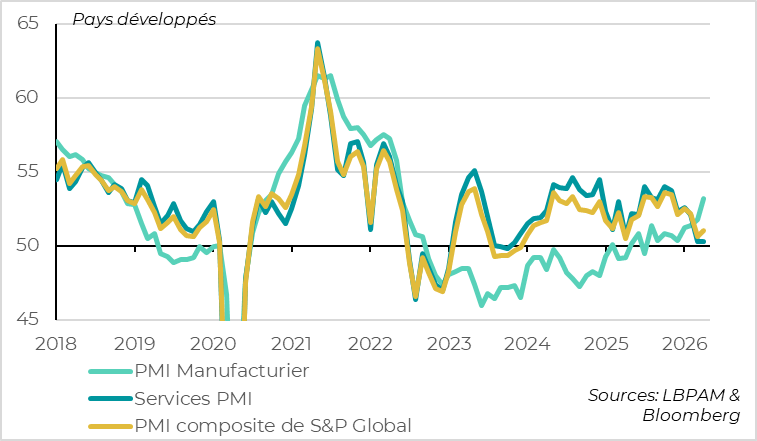

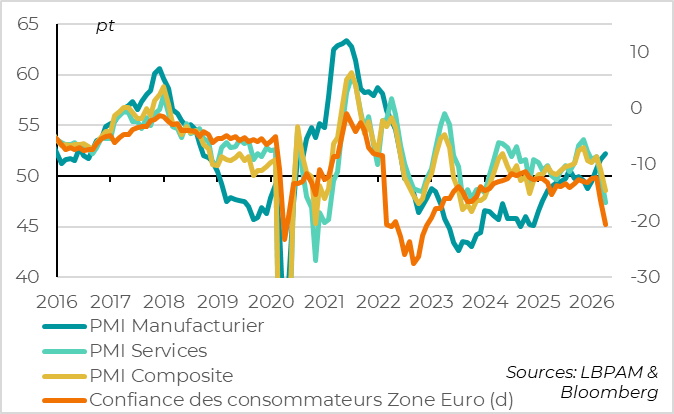

► Preliminary April PMI readings in developed economies have stabilized after their sharp decline in March. As a result, they remain in expansionary territory, but at levels that suggest global growth is running below potential in Q2. At the same time, price indicators are still rising markedly, confirming the stagflationary nature of the shock. However, differences are emerging across regions.

► The Euro Area PMI fell much more than expected in April and moved clearly into contractionary territory, at 48.6. Weakness is confirmed by the sharp decline in consumer confidence and the INSEE indicator in April. Price indicators are rising in the PMI surveys, but more moderately for services selling prices. This suggests that the shock could be more negative for growth than we had anticipated, while the risk of persistent inflation remains quite limited. This reinforces our view that the ECB is likely to raise interest rates at most once this summer.

►In the United States, both PMI surveys and hard data suggest that the slowdown in activity remains limited. By contrast, price pressures are rising more markedly, including in services. Under these conditions, the Fed is likely to wait at least until the end of the year before considering further rate cuts, even though its new chair will face political pressure to lower rates.

► In this context, K. Warsh’s Senate hearing ahead of his confirmation as the new Fed Chair provided little new information. As expected, he defended the Fed’s independence with respect to monetary policy, while arguing for a more limited role for the Fed in other areas (fiscal matters, supervision, etc.). He reiterated his desire to modify the Fed’s strategy regarding its balance sheet, communication, and monitoring of inflationary pressures, but without providing details or guidance on the future level of interest rates. He also declined to answer highly political questions (regarding legal actions by the administration against the Fed and several governors). At the margin, Warsh appears more focused on the Fed’s inflation‑fighting mandate than on its full‑employment mandate, which is difficult to reconcile with rate cuts in the current environment.

► In the United Kingdom, inflation rose sharply in March, driven by gasoline and transportation prices. However, underlying inflation eased slightly, and the labor market weakened after having started to stabilize. We continue to believe that the BoE will keep interest rates unchanged this year, as inflation is set to remain above target while economic growth is likely to run below potential following the rebound in Q1.

Going Further

Global: PMIs broadly stable in April, with regional differences

PMIs in developed economies stabilize in April after their March decline

Preliminary April PMIs confirm the negative impact on global growth, even though activity is still holding up two months after the start of the war in Iran and the energy shock.

The composite PMI for developed economies stabilized in April, rising by 0.2 points to 50.9 after falling by 1.5 points in March. It remains above the 50 threshold—the boundary between expansion and contraction in private‑sector activity—but is well below its levels of the past two years (excluding April 2025, when reciprocal tariffs were announced). Leading indicators (confidence, new orders, etc.) have also stabilized, albeit at low levels. This is consistent with global growth remaining positive but slowing markedly below its trend rate (around 3%).

From a sector perspective, weakness in activity once again originated in services in April. The services PMI edged lower and is approaching the 50 threshold, pointing to near‑stagnation in services at the start of Q2, despite the sector having been the main engine of growth in 2024 and 2025. Higher energy costs are weighing on household purchasing power and confidence, prompting households to cut back on discretionary spending. The sector may also be suffering in the short term from demand being brought forward toward goods.

By contrast, the manufacturing PMI rose again in April, reaching its highest level since mid‑2022, above 53. This reflects not only an acceleration in production but also an increase in new orders and delivery times. It may seem surprising that industry is holding up, as it is typically more cyclical than services. However, this outcome is not unusual during supply shocks, which tend to encourage precautionary purchasing and inventory accumulation ahead of price increases and potential disruptions to production chains. There is little doubt that the manufacturing PMI would decline sharply in the coming months if the energy shock does not ease rapidly.

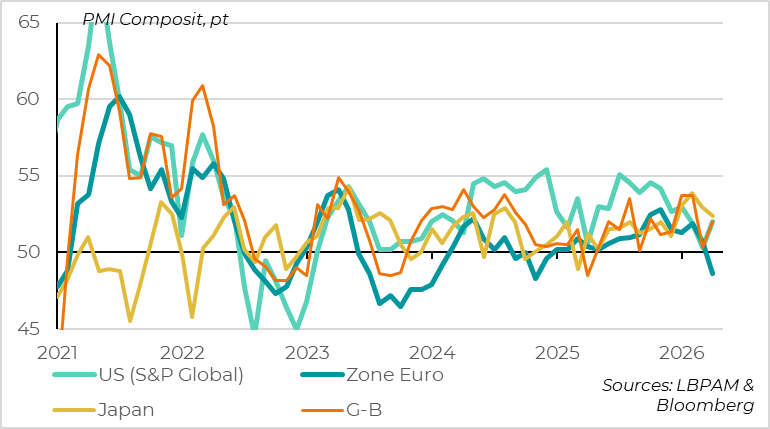

The decline in PMIs is broad‑based, but more pronounced in Europe

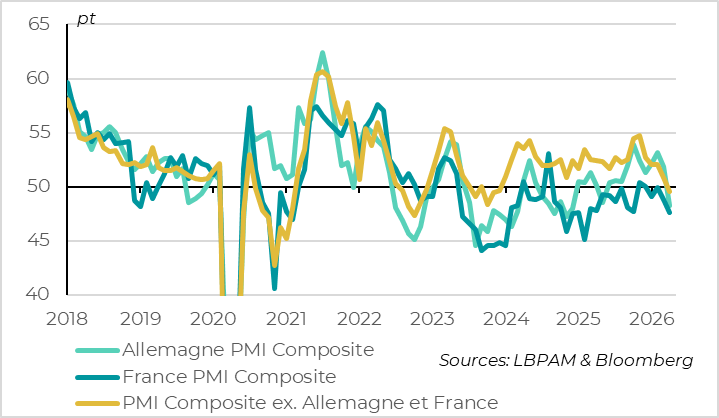

At the country level, PMI developments were fairly dispersed in April following the broad‑based decline in March, with resilience proving stronger than expected outside the Euro Area.

The PMI fell sharply again in the Euro Area, moving clearly into contractionary territory at 48.6. It also declined in Japan, but remained relatively elevated at 52.4. It is somewhat surprising that the Japanese PMI is the highest among major developed economies, given that Asia is the region most exposed to the Middle East energy shock. This likely reflects (1) the strong recovery momentum Japan had prior to the outbreak of the war and (2) support from the AI‑related investment cycle in East Asia.

The slight rebound in the U.S. PMI in April, to 52, is less surprising given that the decline in March had been unusually sharp (and was not confirmed by other indicators such as the ISM or retail sales), while the U.S. economy is somewhat less exposed to the current shock. That said, the U.S. PMI still stands well below its levels of the past two years.

The positive surprise came from the rebound in the UK PMI, which, like its U.S. counterpart, rose from 50.3 to 52 in April. This is noteworthy given that the UK economy is typically among the European economies most exposed to energy shocks. However, we refrain from drawing strong conclusions based on a single data point, especially as domestic surveys were much more negative in April—both for households (consumer confidence at its lowest since 2023) and for industry (business optimism at its weakest since the Covid period).

U.S. indicators are still holding up in April

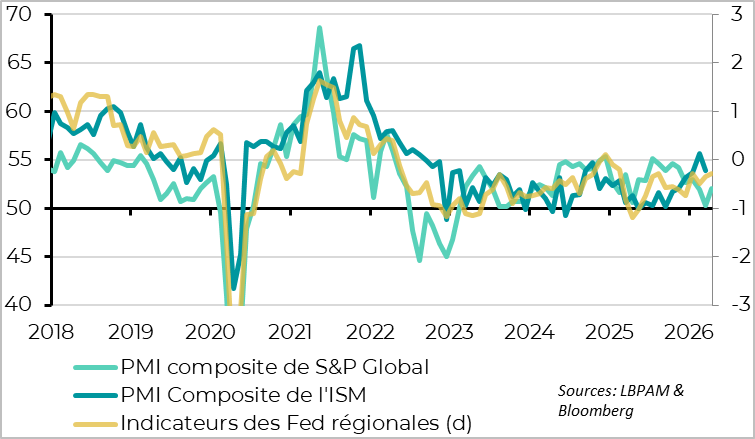

U.S. regional Fed surveys for April are broadly stable after having improved in March, and remain slightly more supportive than the PMI published by S&P Global, although the gap is narrowing. That said, indicators for services—which account for around 80% of U.S. GDP—are at relatively low levels, consistent with growth close to 1%. The resilience of U.S. activity, confirmed by hard data such as retail sales and initial jobless claims, suggests that the recessionary impact of the energy shock is less severe in the United States than in Europe or Asia. However, it is not absent, and consumption is still likely to slow again around mid‑year.

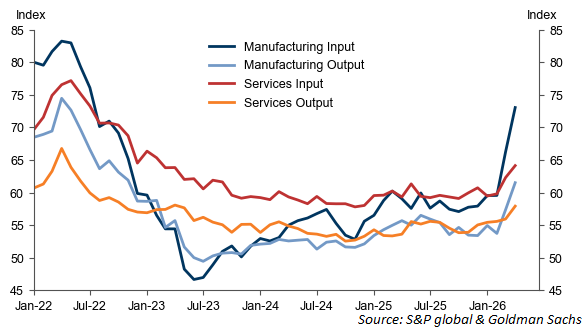

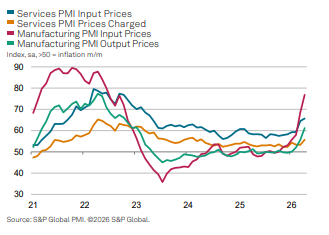

The price shock is broad‑based

Moreover, the price shock is broad‑based across all developed economies and sectors, although it is more pronounced in the United States and the United Kingdom, and more acute in manufacturing than in services. This argues for continued caution from the BoE and, even more so, from the Fed before considering rate cuts—particularly in the United States, where risks to growth and employment remain more limited.

Euro Area: a stagflationary shock, but more recessionary than inflationary

Activity contracts sharply in April, driven by services

The Euro Area PMI fell again in April, from 50.7 to 48.6, suggesting that activity is contracting for the first time since 2024 (around ‑0.1% quarter‑on‑quarter according to our models). Once again, the decline is driven by services, whose PMI, at 47.4, is at its lowest level since the lockdowns of early 2021. By contrast, the manufacturing PMI rose again, as elsewhere. At 52.2, it is even at its highest level since mid‑2022 and the previous energy shock. However, this apparent resilience in industry mainly reflects precautionary purchasing ahead of price increases and potential disruptions to supply chains. Indeed, outlook indicators are deteriorating sharply in both sectors, with industrial new orders at their lowest level in a year and a half and business confidence at its weakest since the start of the war in Ukraine.

Confidence is also weakening among consumers. The European Commission’s consumer confidence indicator fell sharply again in April, reaching ‑20.6, its lowest level since 2022. Overall, the decline in consumer confidence over the first two months of the war in Iran already represents around two‑thirds of the drop observed during the first two months of the war in Ukraine. This is striking given that the rise in gas and electricity prices bears little resemblance to the 2022 shock, and it suggests that the growth impact could be larger than we currently anticipate.

The decline in activity is broad‑based and also affects the southern part of the euro area

At the country level, the decline in PMIs across the euro area is broad‑based. The German PMI fell sharply for the second consecutive month and moved back into contractionary territory for the first time in a year, after having been elevated prior to the war thanks to the public spending momentum initiated late last year. The French PMI declined less sharply, but from an already very depressed level, leaving it below those of other euro‑area countries. Finally, and most importantly, the PMI for the rest of the euro area also fell and entered contractionary territory for the first time since 2023. This suggests that Italy—highly exposed to the energy shock—and, to a lesser extent, Spain, which is less exposed, are nevertheless feeling the strain despite the fiscal support measures implemented by their governments to limit the impact of higher gasoline prices.

Input costs are accelerating sharply, while selling prices are rising more moderately

Alongside the sharp negative shock to activity, April PMI surveys confirm the strong rise in price pressures since the onset of the energy shock, which is unlikely to reassure the ECB. Input costs for companies (including energy) are rising rapidly, both in manufacturing and services, reaching their highest level since late 2022. This is pushing firms to raise their selling prices, which are increasing at their fastest pace since early 2023.

However, the increase in selling prices is significantly more limited than the rise in companies’ costs, particularly in the services sector, which better reflects firms’ domestic pricing power. This suggests that companies are absorbing a larger share of higher costs through their margins in order not to discourage demand, thereby reducing the risk of second‑round effects and persistent inflation following the energy shock. This is consistent with our view that the current environment is less conducive to sustained inflation than in 2022 for the euro area, and that the ECB should therefore not raise rates aggressively.

In our scenario, in which energy prices decline over the course of Q2, we expect the ECB to leave rates unchanged next week and to deliver at most one ‘insurance’ rate hike this summer. The market is once again pricing in more than two…

United Kingdom: March data do not argue for rate hikes

Inflation accelerated sharply in March, while underlying inflation slowed

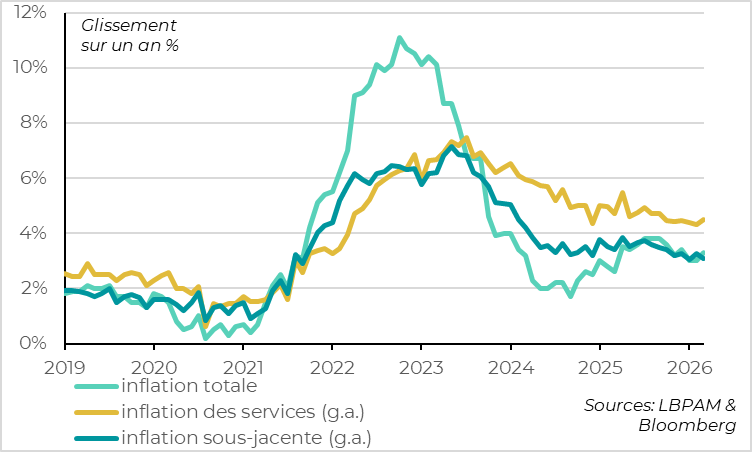

As expected, UK inflation accelerated from 3.0% to 3.3% in March, driven by a 9% month‑on‑month increase in gasoline prices and a stronger‑than‑anticipated acceleration in food prices. Inflation is set to rise even more sharply in Q3, when household gas and electricity prices are adjusted. This puts pressure on the BoE, at a time when inflation had been expected, prior to the war, to return to the 2% target from Q2 onward.

That said, underlying inflation eased slightly in March, from 3.2% to 3.1%, which was unexpected and marks its lowest level since 2021. Services prices increased due to higher airfares, but inflation in other services remained stable, while manufactured goods inflation slowed markedly, from 1.3% to 0.8%.

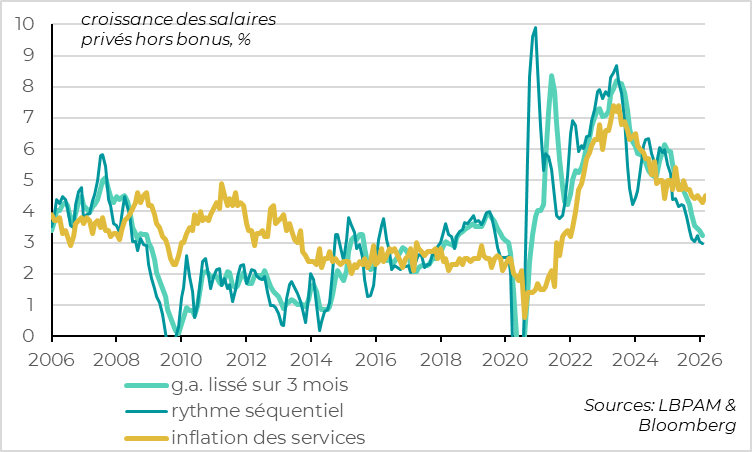

Wage dynamics are consistent with a return to target inflation over the medium term

Wage growth continued to slow in early 2026 following the deterioration in employment in the second half of last year. At 3.2% year‑on‑year and around 3% on a sequential basis prior to the outbreak of the war in Iran, wage growth had returned to a level that the BoE considers consistent with inflation converging back to its 2% target over the medium term.

Overall, inflationary pressures were continuing to ease before the energy shock and were consistent with a gradual return of inflation toward the target.

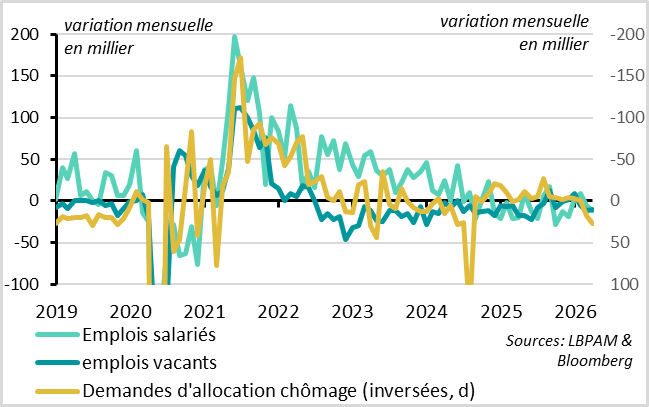

Employment deteriorates again in March after stabilizing at the start of the year

Employment had started to stabilize at the beginning of the year alongside the recovery in activity, even though the decline in the unemployment rate from 5.2% to 4.9% in February was overstated by a drop in the participation rate. However, labor market conditions deteriorated sharply in March, suggesting that companies have once again become very cautious in the face of the new energy shock. Indeed, payroll employment declined by 11,000 after three months of stabilization, jobless claims increased more markedly, and the number of job vacancies fell to its lowest level since 2021.

Overall, the highly stagflationary environment in the United Kingdom makes the BoE’s task particularly challenging. It is difficult to cut rates while inflation is set to remain well above target this year. At the same time, the weakness in the labor market does not argue for a more restrictive stance, especially as fiscal policy is already restrictive. Against this backdrop, we expect the BoE to keep rates unchanged at its meeting next week and through the rest of the year, although the risk of an ‘insurance’ hike cannot be ruled out should the energy shock prove larger or more prolonged than we currently anticipate.

Xavier Chapard

Strategist