All wars end one day

Link

What are the key takeaways from the market news on march 03, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► This weekend, the United States and Israel unilaterally decided to go to war with Iran. In the very first hours of the conflict, targeted attacks and bombings resulted in the death of Ali Khamenei, the country’s supreme leader and president. Along with him, several other leaders were killed.

►A new leadership is already in place in Iran, which has begun retaliating against the attacks, targeting not only U.S. forces in the region and Israel, but also countries allied with the United States, including Saudi Arabia, the Emirates, Kuwait, and Oman.

►President Trump’s objectives regarding this war do not seem entirely clear. Although the demand to halt Iran’s nuclear program remains a requirement, the American president now appears to be aiming for a regime change.

►Moreover, in his latest statements, President Trump no longer ruled out sending ground troops to ensure that a regime change would indeed take place. Such a decision would go against his campaign promises and further weaken the Republican Party in the upcoming midterm elections this November.

►Despite the military superiority of the United States and Israel, the outcome of this war is very uncertain, as is the path to bringing it to an end. We know that all wars end one day. But their duration and the damage they can cause are key factors in assessing the consequences for the global economy and the markets.

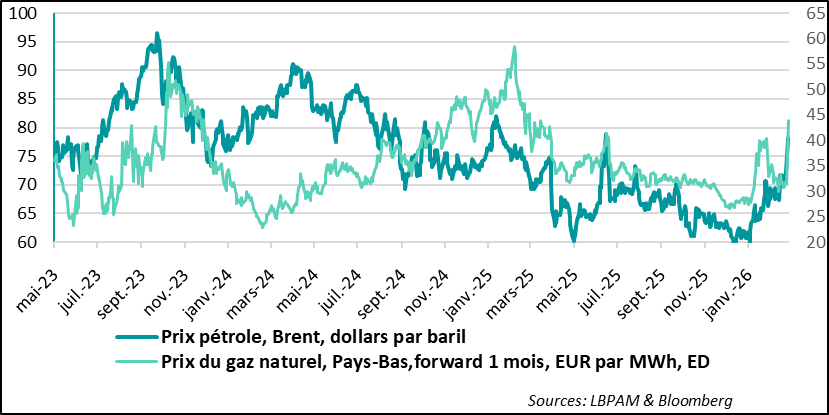

►Obviously, in the present situation, the main focus is the impact of this war on the evolution of oil and gas prices. So far, globally, the price of a barrel of oil (Brent) has risen by less than 10 dollars (to 80 dollars per barrel) since the start of the hostilities, bearing in mind that the market had already priced in a premium of around 5 dollars due to the rising tensions with Iran in recent weeks. Moreover, Qatar’s decision to halt its gas (LNG) exports because of the war has put strong upward pressure on gas prices in Europe.

►Nevertheless, these increases remain relatively moderate and do not seem to reflect extreme risks. The market appears to be anticipating a short conflict, allowing conditions to return to something close to the pre-war period in the coming months.

►At this stage, we favor this scenario with a probability above 50%: a short conflict with no regional escalation. In this case, the price of a barrel of Brent crude could return to 70 dollars or even lower. In this context, the impact on global growth would be limited.

►Alternative scenarios would depend largely on the duration of the conflict and, in particular, on the impact on oil supply. A near‑closure of the Strait of Hormuz — through which around 20% of global production transits (20 million barrels per day) — could push the price of a barrel toward 100 dollars, while a total blockage combined with damage to production infrastructure could trigger a massive oil shock, sending prices above 130 dollars and likely causing a global recession.

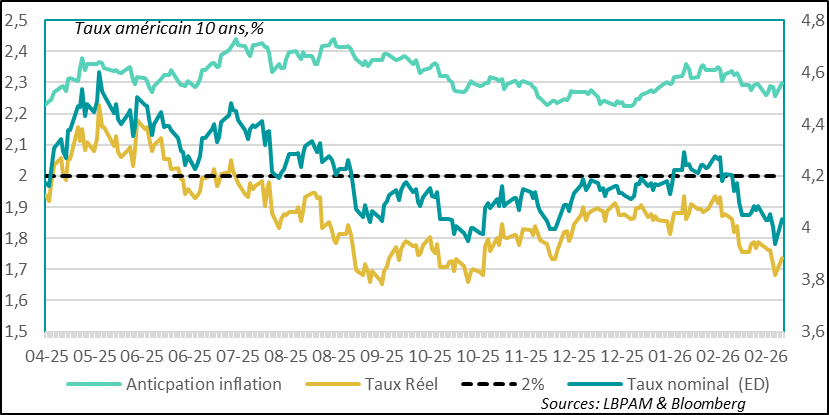

►In the markets, long‑term interest rates have risen, reflecting on the one hand the inflationary impact of higher oil prices and, on the other, investors’ concerns about a possible deterioration in public finances, partly linked to potentially higher military spending. As a result, U.S. long‑term yields have increased by more than 10 basis points. The recession risk associated with an oil shock does not appear to be reflected in prices.

In equities, in Europe, the sharp rise in energy prices — particularly gas — which has contributed to higher long‑term rates, has led to a significant drop in stock markets. In the United States, indices have held up better, supported by gains in energy and defense stocks.

►Caution appears warranted in the short term when it comes to asset allocation, given the high level of uncertainty caused by this war. Nevertheless, in the scenario we consider most likely — a relatively short conflict and therefore a global economic growth that holds up — markets should stabilize and recover.

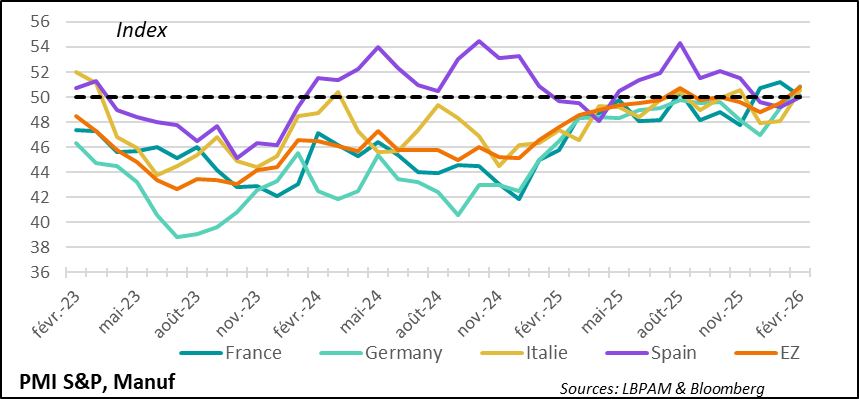

►The magnitude of the impact from the shock also depends on the current momentum of the economies. In this regard, the final activity statistics from S&P’s PMI surveys for February have maintained a rather positive tone, allowing for the absorption of a moderate and short‑lived oil shock. In particular, for the Eurozone, industrial activity appears to be holding up in the region’s main countries, with all of them in expansion territory.

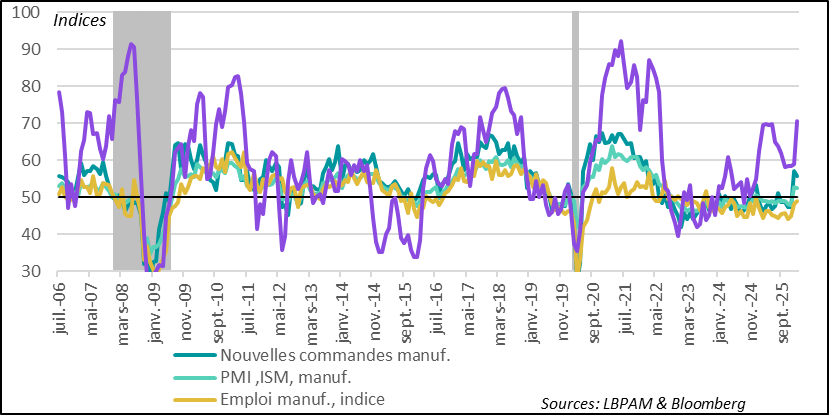

►In the United States, the ISM indicator for the manufacturing sector remained relatively solid in February, although it edged down slightly compared with the previous month. Activity continues to be supported by strong demand, with new orders remaining high. However, despite a slight improvement, hiring is still lagging, while input costs rose sharply over the month.

Going Further

War in the Middle East: significant short‑term uncertainty

Towards slightly lower rates?

The unilateral war against Iran launched by the United States and Israel has plunged the global economy into an atmosphere of considerable uncertainty. Based on available information, the weakening of the regime was viewed by U.S. and Israeli authorities as an opportunity to strike the Islamist state. As a result, the negotiations that had been underway between Iran and the United States were abruptly interrupted, and a war was triggered.

The objectives of the war appear to go beyond the demands related to Iran’s nuclear program and, according to President Trump, now aim for regime change. Indeed, in an extraordinary development, from the very first large-scale U.S. and Israeli strikes, the Iranian leadership was “decapitated,” with the death of Ali Khamenei, the country’s supreme leader and president, along with a significant number of senior officials.

While new authorities have taken power, they quickly launched a counterattack targeting U.S. forces, Israel, and also regional countries allied with the United States, including Saudi Arabia, the Emirates, Kuwait, and Oman. Cyprus was also struck, as the Iranians targeted a British military base in retaliation for the United Kingdom’s support to the United States.

At the time of writing, U.S. strikes on Iran continue, as do Iranian counterattacks, including an assault on the U.S. Embassy in Riyadh. President Trump has stated that the war could last for some time and has even raised the possibility of sending ground troops to achieve the objectives he has set. Such a decision would run counter to his campaign promises and could further weaken the Republican Party in the upcoming midterm elections in November.

Naturally, for the global economy, the primary concern is the impact of the conflict on oil prices. So far, prices have increased only moderately, extending the rise that began as tensions between the United States and Iran escalated during the recent negotiations. Brent crude has already reached 80 dollars per barrel.

This increase reflects fears that oil supply could be significantly disrupted, either through damage to production infrastructure or major restrictions — even the impossibility — of shipping oil through the Strait of Hormuz, knowing that nearly 20% of global oil production transits through this narrow passage, roughly 20 million barrels per day.

At this stage, although tanker traffic appears restricted, it continues, and there has been no major destruction of production or distribution facilities. However, Qatar has announced the suspension of its LNG production, which has led to a sharp surge in European gas prices, surpassing 40 euros per MWh — the highest level since the start of the war in Ukraine.

It is certainly very difficult to build economic scenarios with confidence. Nevertheless, at this stage we assign a relatively high probability (60%) to a fairly short conflict, lasting no more than a few weeks. This would likely result in temporary spikes in energy prices, but the impact on growth would be relatively limited, as the short-term negative shock would be offset by a subsequent rebound.

In macroeconomic models, a sustained 10% increase in oil prices in developed countries typically results in a 0.1% decline in GDP and a similar rise in inflation. In Europe, which is more energy‑dependent, the effects are somewhat stronger.

In the case of a much larger shock — say a 40% rise in oil prices, pushing them toward 100 dollars per barrel — the impact on growth would be substantial. Beyond that level, for the Eurozone, a recession would be more than likely.

Such a shock could, however, be softened by economic policy. In particular, central banks would counter the recessionary impact with significant rate cuts. Fiscal policy would be more complex, especially given that many countries have limited room for maneuver.

For now, risk appetite on the markets has decreased reasonably, though some indices have experienced significant declines. Still, markets are far from pricing in a worst‑case scenario. In the United States, stock indices even ended in positive territory yesterday, supported by energy and defense‑related sectors.

The bond market appears to be concerned about the inflationary impact and the pressure on public finance

Moreover, in the bond markets, the recession risk linked to the conflict does not appear to be the dominant scenario. Instead, investors seem more concerned about the risk of rising inflation and the increasing need for public financing, including defense spending.

In our view, caution should prevail in the short term, given volatility that is likely to remain elevated. Nevertheless, this war will come to an end — as is always the case. We are opting for a scenario that may of course prove optimistic: namely, an end to the conflict within a few weeks, avoiding in particular a major escalation across the Middle East. Under such conditions, the return to calm should pave the way for a rebound in risk appetite.

Industrial activity: growth remains resilient at the start of the year

Industrial activity held up at the beginning of 2026

S&P’s final PMIs for February confirmed that manufacturing activity held up well at the start of the year. In fact, one of the positive surprises came from the Eurozone, where all major countries in the region saw their industrial activity return to expansion territory. In particular, Germany appears to be showing clear signs of recovery linked to the fiscal stimulus plan.

U.S. manufacturing PMI remains solid

In the United States, the ISM survey for the manufacturing sector in February showed that activity remained dynamic after last month’s rebound. Although there was a slight softening, new orders in particular remain very strong. This clearly reflects business optimism, supported by substantial fiscal incentives, especially those designed to boost investment. At the same time, firms continue to exercise caution, with hiring not contributing meaningfully to the improvement in activity. Moreover, it is important to note the cost pressures, with a sharp increase in the prices paid by companies.

The ongoing war in the Middle East risks creating additional uncertainty, raising energy bills and therefore slowing the pace of recovery. But if the conflict remains short‑lived, from an economic perspective—given the stimulus measures being implemented—activity should continue to hold up.

Sebastian Paris Horvitz

Director of Research