Amid the confusion, D. Trump seems to want to end the war

Link

What are the key takeaways from the market news on March 24, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► Over the weekend, in just a few hours, D. Trump first announced that his objectives in the war with Iran were close to being achieved, suggesting that the end of hostilities was near. Then came a very belligerent message issuing an ultimatum to the Iranian authorities to open the Strait of Hormuz within 48 hours, failing which the U.S. military would annihilate Iran’s energy production capabilities. This message became void yesterday morning, with a new statement from the U.S. president declaring that the ultimatum was suspended, as discussions with Iranian authorities were moving toward a resolution of the conflict.

►Despite the confusion created by these successive contradictory messages, the market interpreted the latest announcements as a genuine path toward possible easing. This surge of optimism occurred while Israel was continuing its attacks on Iran, and while President Trump’s comments remained rather vague regarding the Iranian interlocutors with whom U.S. negotiators were engaged in discussions.

►Thus, amid such confusion, the market’s rather positive reaction — with the Brent crude oil price ending the day sharply lower, below 100 dollars, along with a strong rebound in stock indices in Europe and the United States and a decline in long‑term interest rates — could be described as overly complacent. But in our view, President Trump’s hesitations seem to indicate that he is indeed seeking a way out of this conflict, which, in the short and medium term, could cost him not only economically but, more critically, politically.

►At the same time, we still cannot ignore the risks of a stalemate, or at least the possibility of a more prolonged conflict than we initially expected. Indeed, instability remains high and tensions in the region are still very intense. However, at this stage, we maintain the assumption that a strategic withdrawal by the United States should bring calm relatively quickly.

►Nevertheless, even if a return to normal in energy prices could occur fairly quickly with the reopening of the Strait of Hormuz, which remains blocked today, it must be acknowledged that there is now greater uncertainty surrounding production capacities in the region, following the damage already inflicted.

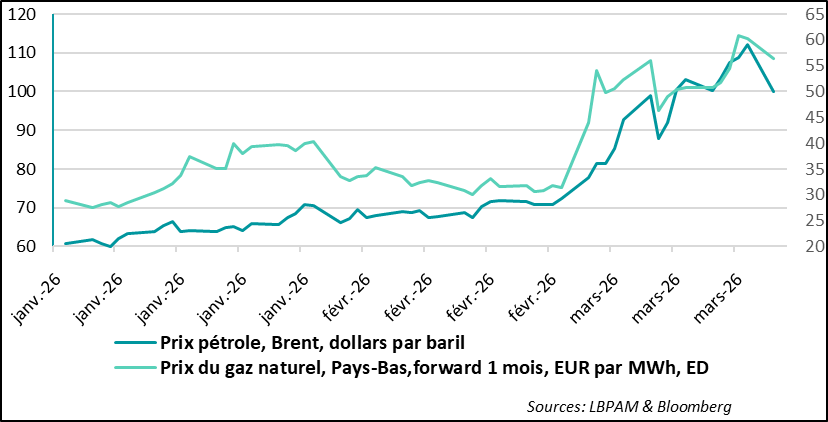

►Already, everything suggests that the price of oil could remain higher than we had anticipated. Indeed, the average price of a barrel of oil has now approached 100 dollars since the start of the war, and the price of gas in Europe remains above 50 euros per MWh. Even assuming a convergence over the summer toward pre‑war levels, the negative impact on growth and inflation could prove stronger, particularly in Europe.

►The market appears to be strongly focused on the impact on inflation. While the rise in energy prices will have a mechanical effect on consumer price developments, despite possible mitigation measures that governments in various countries might adopt, it seems to us, at this stage, that in the long run this shock will primarily have a negative impact on growth. Nevertheless, markets believe that central banks will act by raising interest rates in order to prevent any slippage in inflation expectations.

►This view, admittedly, is also fueled by statements from numerous central bankers in Europe, whether in the United Kingdom or in the euro area. It appears that the ‘trauma’ of the Covid period remains very vivid, as central banks were slow to act in the face of multiple supply and demand shocks. Nevertheless, it remains difficult today to identify which demand shock could trigger second‑round effects in price setting.

►Nevertheless, it is clear that market participants now expect a significant number of policy rate hikes in Europe.

►Given the rhetoric of central bankers in Europe, it is likely that preventive policy rate hikes will take place in the coming months. However, we anticipate only a very limited number of them. In our view, an overreaction by central banks would have a fairly negative impact on growth. In the United States, market expectations seem more reasonable, with a status quo in monetary policy in 2026.

►Given the significant short‑term uncertainties, we are maintaining a cautious stance in our asset allocations. Nevertheless, our central scenario remains that of a resolution of the conflict in the Middle East within the coming month, allowing risk‑taking to resume in an environment that should remain supportive thanks to public measures sustaining growth.

Going Further

War in the Middle East: Uncertainty remains high even though the United States appears to be seeking a way out of the crisis

Energy prices fluctuate according to the messages sent by the U.S. authorities

D. Trump’s contradictory comments over the weekend and at the start of the week, alternating between escalation and de‑escalation, continue to generate significant volatility in the markets, particularly in energy prices. Indeed, after stating at the end of last week that U.S. objectives in the war with Iran were nearly achieved and that the end of the conflict was near, the U.S. president changed his stance within a few hours and threatened Iran with an ultimatum to annihilate its energy infrastructure if the Strait of Hormuz was not reopened within 48 hours. Then, yesterday, President Trump’s message became much more moderate again, indicating that talks with Iranian officials were progressing well toward resolving the conflict.

It is difficult to see things clearly, all the more so as Israel has continued bombing Iran in the meantime, and Iran has retaliated by targeting energy infrastructure in the region.

In any case, despite the fact that the price of a barrel of Brent crude has already risen back above 100 dollars, it seems to us that D. Trump is genuinely trying to extricate the United States from this conflict. He can only observe that the economic—and especially political—costs of this war risk becoming too high as the midterm elections at the end of the year draw nearer.

In this sense, we still consider the most likely scenario to be a relatively rapid end to hostilities rather than a protracted conflict.

At the same time, we also note that the effects of the conflict are proving more negative than we anticipated, including on energy prices. While we expected significant spikes in energy prices during the conflict, we now find ourselves well above the average levels we had projected for the period.

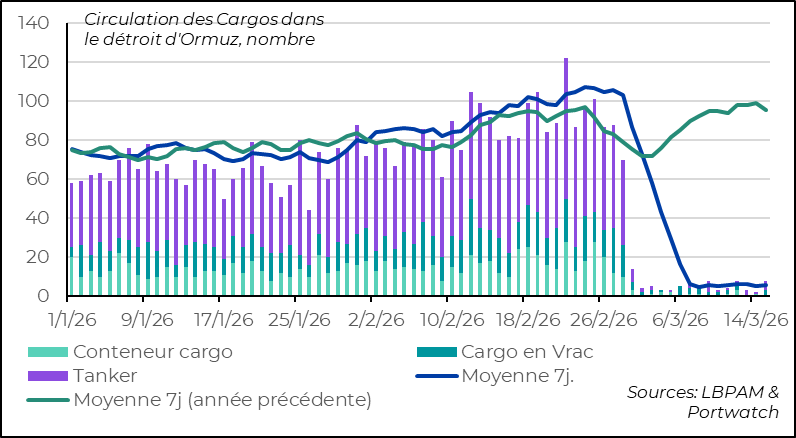

The Strait of Hormuz remains closed

One of the major reasons for these higher energy price levels is the continued near‑total closure of the Strait of Hormuz. Moreover, while it was initially assumed that the region’s energy infrastructure (oil and gas) would be preserved, it has become clear that this is not the case. As a result, the risks of more lasting price disruptions, at least in the short term, have increased.

In this regard, we believe that, in the short term, the risks to inflation and growth will be greater than expected, particularly in Europe. A loss of at least 0.1 percentage point of additional growth in 2026 now appears very likely to us.

At the same time, we continue to believe that a gradual return to normal by the end of Q2 2026 should allow European economies and the global economy to regain a more supportive momentum.

Thus, in the short term, we remain fairly cautious in our asset allocations, yet we stay constructive for the full year, with markets likely to be supported by a more favorable economic dynamic, bolstered by public‑sector stimulus measures.

Central banks: heading toward an overreaction?

Strong expectations of policy rate hikes to counter rising energy prices

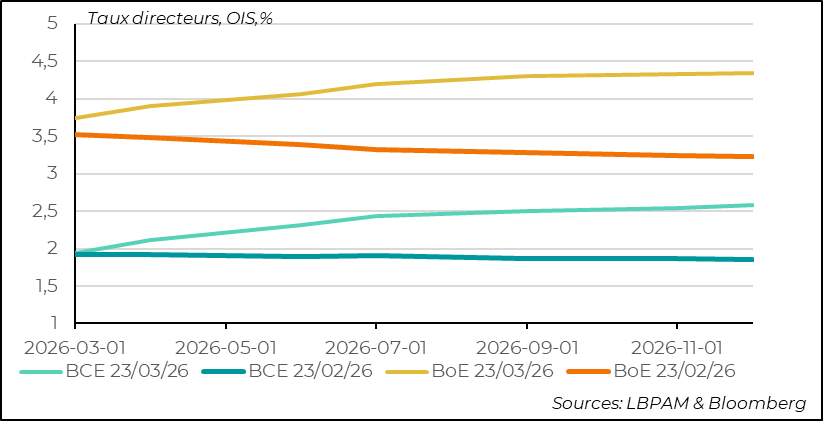

Faced with an energy shock that is proving more significant than expected, concerns have risen about its potentially lasting impact on inflation. This concern is particularly strong in Europe. As a result, expectations of interest rate hikes have increased sharply in recent weeks, both for the ECB and— even more notably— for the Bank of England (BoE).

This movement has been driven in part by comments from several central bankers suggesting that rising energy prices could trigger second‑round effects and ‘de‑anchor’ inflation expectations.

While such effects are possible, we believe that, at this stage, the supply shock reflected in energy prices should be viewed as such, and that it would be misguided to use monetary policy to counter it— especially given that its very nature tends to depress demand.

Nonetheless, the ‘trauma’ left by the Covid crisis still appears to be very present, as central banks acted too late at the time to counter a succession of supply and demand shocks. However, we consider that this shock has little in common with the Covid period.

In any case, given recent central bank comments, it seems reasonable to expect rate hikes. However, we do not believe central banks will be able to go very far in tightening monetary policy, especially if energy prices normalize quickly. Thus, for the ECB in particular, we believe that at most one rate hike could occur by the summer, mainly to satisfy the institution’s most orthodox governors.

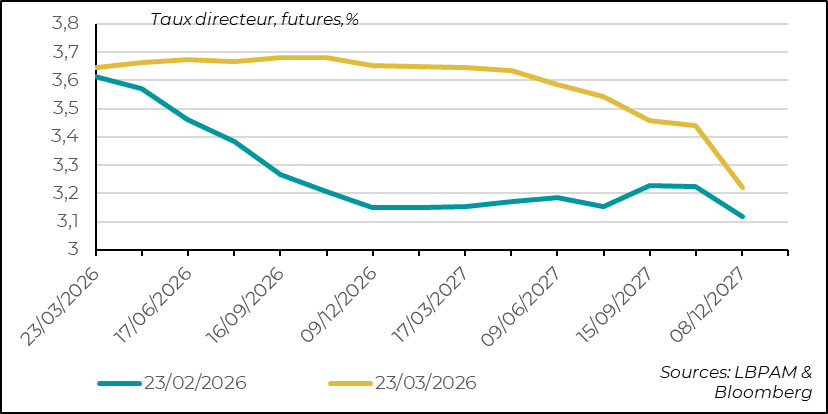

Expectations regarding the Fed appear more reasonable

For the Fed, expectations regarding the path of policy rates have also shifted completely. They now stand very close to our own projections. We no longer expect any rate cuts this year.

Overall, we believe that the risk of an overreaction by central banks—approaching a policy mistake—has increased. However, we continue to assume a more reasonable scenario, one that should help preserve growth rather than undermine it.

Sebastian Paris Horvitz

Director of Research