Central banks’ caution in the face of the resolution of the crisis

Link

What are the key takeaways from the market news on June 19, 2026? Sebastian Paris Horvitz provides some insights.

Overview

►The document outlining the preliminary agreement to end the conflict between the United States and Iran was signed yesterday by the authorities of both countries. The key point for markets is the immediate reopening of the Strait of Hormuz. This has resulted in a continued decline in oil and gas prices. The price of a barrel remains close to 80 dollars.

►At the same time, discussions will continue for 60 days to confirm the other elements of the agreement, particularly regarding the Iranian nuclear program. Nevertheless, despite concerns about the durability of this agreement, it seems to us that there is a very strong willingness on both sides to return to a stable framework. Overall, we take as a key point the statement made yesterday by President Trump: “I wanted to avoid an economic catastrophe if [this conflict] had continued.”

►The very rapid declines in oil and gas prices are expected to stabilize. In our view, these decreases will feed through, more or less quickly, into consumer prices across all economies. If energy prices were to remain at current levels, inflation could quickly be reduced by 0.5 percentage points. Moreover, the pass-through effects of the energy shock on inflation would be significantly limited.

►Obviously, at this stage, central banks are likely to remain generally cautious. It is difficult to be definitive about the transmission of the energy shock, particularly regarding potential second-round effects that could keep inflation higher for longer and, above all, alter expectations.

►On Wednesday, the Fed decided to keep its key interest rates unchanged. Although K. Warsh, the new Chair of the Fed, did not provide a very clear view of his assessment of the adequacy of monetary policy in the current context, his emphasis on the need to bring inflation back to its 2% target was seen by the market as a call for discipline.

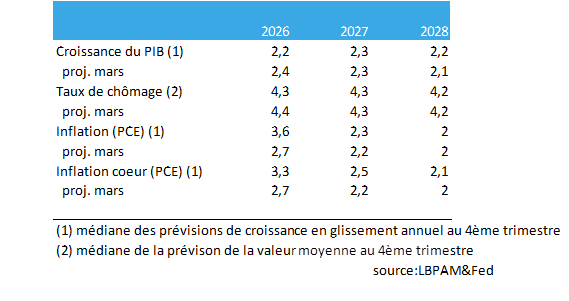

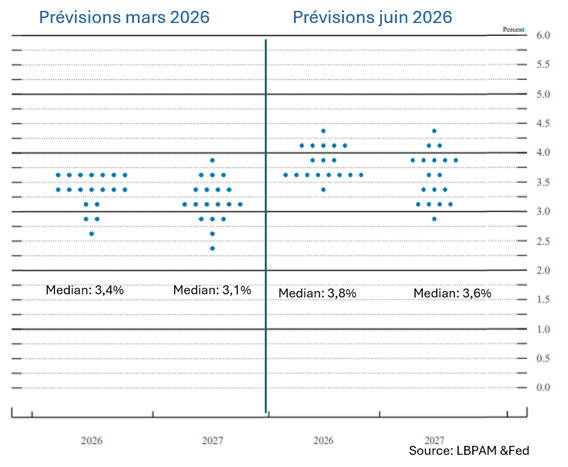

►This view was reinforced by the projections of several members (8 out of 16) of the monetary policy committee, who anticipate at least one rate hike in 2026 (the median policy rate rising to 3.8% by the end of 2026, compared with 3.4% in the March projections).

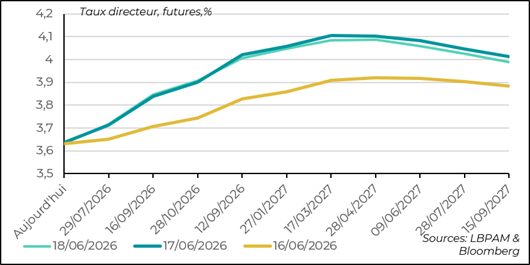

►This surprised the market and led to upward revisions in expectations for policy rates, pushing short-term sovereign yields sharply higher (+17 basis points on the 2-year, before easing somewhat).

►We maintain our view that the Fed should not overreact, especially given the current pace of the decline in energy prices. However, given the resilience of the U.S. economy, upward pressure on prices could persist, increasing the risk of a rate hike by the end of the year. As a result, we now consider it reasonable to expect a single rate hike in the fall.

►Regarding the strength of the U.S. economy, retail sales data showed that consumption remains resilient. Indeed, the statistic used as an initial estimate of consumption in GDP, known as the control group, recorded growth of 0.7% in current dollars in May. This shows that, despite the shock to purchasing power, the consumer remains a key driver of growth.

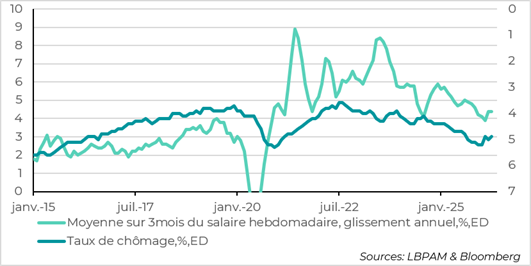

►In the United Kingdom, the BoE also decided to keep its policy rate unchanged. As at the previous meeting, seven members of the monetary policy committee voted for the status quo, while two continued to advocate for a tightening of the bank’s stance.

►At the same time, inflation data for May came in below expectations, remaining stable at 2.8% year-on-year for headline inflation and rising only slightly to 2.6% for core inflation. This likely helped reassure central bankers. Similarly, wage growth in April, although still somewhat elevated, remained unchanged year-on-year at 4.4% compared with the previous month, indicating no building wage pressures. As a result, the unemployment rate remains relatively high at 4.9% (its highest level since February 2021).

►Nevertheless, we maintain our view that a rate hike by the BoE by the fall appears reasonable in order to accelerate inflation’s convergence toward the 2% target without significantly affecting growth. The market remains more aggressive.

►From a political standpoint, A. Burnham, the Mayor of Greater Manchester, won the by-election he had sought in order to become a member of the House of Commons. This paves the way for him to run for Prime Minister against K. Starmer. He has a strong chance of succeeding. For markets, the concern surrounding the pressure on K. Starmer to step down from within the Labour Party was that an overly populist candidate might replace him, raising the risk of a deterioration in public finances. So far, A. Burnham has sought to reassure investors by stating that he is committed to maintaining sound public finances.

Going Further

United States: Fed holds rates steady

Outlook: solid growth and inflation converging to 2% by 2028

Unsurprisingly, the Fed’s monetary policy meeting on Wednesday concluded with the current policy being maintained, with interest rates left unchanged. However, this first meeting led by K. Warsh, the new Chair of the Fed, triggered a strong market reaction, with investors anticipating a tightening of monetary policy ahead.

First, K. Warsh strongly emphasized the Fed’s commitment to bringing inflation back to its 2% target. This was seen by the market as confirmation that he is firmly defending the institution’s independence and its mandate, and that pressure from President Trump would not influence policy decisions.

Moreover, as will be discussed below, the projections from members of the monetary policy committee regarding the path of policy rates proved significantly more restrictive than expected.

These views were reinforced by economic forecasts pointing to resilient growth in the years ahead, alongside a labor market that remains close to what is considered full employment, with an unemployment rate ranging between 4.2% and 4.3%.

At the same time, somewhat paradoxically, K. Warsh did not clearly commit to a specific stance, remaining vague in his characterization of the monetary policy setting (restrictive, accommodative, or neutral).

Instead, he focused his communication on five initiatives he has launched, related to the Fed’s communication strategy, quantitative policy (balance sheet management), the economic data used in decision-making, the impact of technological changes on productivity and employment, and the drivers of inflation.

It remains unclear what specific objectives he aims to achieve, aside from the fact that he has been highly critical of the Fed’s practices in recent years, despite having previously served on the Board.

It should also be noted that, in response to the numerous shocks of recent decades, the Fed has already conducted several reviews of its policy framework to improve both communication and implementation.

More restrictive projections for policy interest rates

In any case, the announcement of these initiatives had little impact on investor sentiment. By contrast, the projections submitted by the committee members had a strong effect on the market.

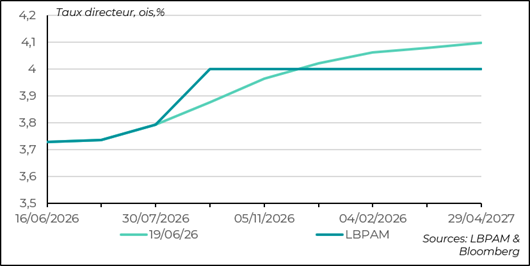

Indeed, compared with the March forecasts, committee members’ expectations regarding the appropriate level of policy rates have clearly shifted upward. As a result, half of the members now expect at least one rate hike by the end of 2026. However, these increases would be partly reversed in 2027.

It is worth noting that K. Warsh deliberately chose not to participate in this exercise and did not submit any projections.

Market expectations are shifting upward

This shift in views within the monetary policy committee has therefore led to a rise in expectations regarding interest rate levels. The market now anticipates two rate hikes by early 2027.

We had maintained the view that the Fed should keep policy rates unchanged. However, even though the sharp decline in energy prices we are observing will alter the inflation dynamic, its slowdown may prove gradual—especially given the continued strength of the U.S. economy. This could justify a rate hike in order to firmly anchor inflation expectations. Importantly, this view now appears to be gaining support among members of the monetary policy committee.

United Kingdom: prices and wages support the BoE in maintaining an unchanged policy stance

Inflation came in lower than expected in May

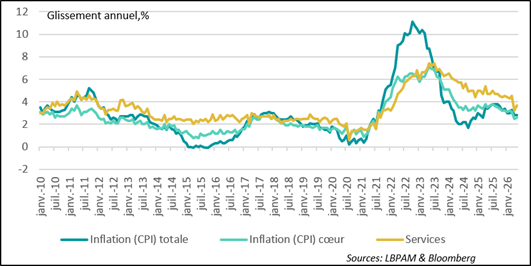

In May, inflation in the United Kingdom came in well below expectations, which is a positive surprise. Headline inflation remained unchanged at 2.8% year-on-year. Notably, the monthly increase was only 0.2%, compared with 0.4% expected. Core inflation also edged up only slightly to 2.6%.

Of course, caution is warranted, as a single data point does not establish a trend. However, with the expected decline in energy costs, we can be somewhat more optimistic about the outlook for prices in the coming months.

This development was likely well received by the BoE, although it will continue to monitor price dynamics in the services sector, where the energy shock may still be feeding through via indexation effects, continuing to put upward pressure on prices.

Policy rates at their highest level in over 30 years

In addition, labor market and wage data were reassuring, with the unemployment rate declining slightly but remaining relatively high, and wage growth, although edging up, not pointing to significant inflationary pressures.

A rate hike in the fall appears reasonable

In light of these data, the monetary policy committee once again decided to leave its policy unchanged by a very large majority (7–2).

Nevertheless, it seems to us that, in order to achieve its objective of bringing inflation back to 2% and to keep expectations well anchored, the BoE will need to adopt a somewhat more proactive stance. We therefore maintain our projection of a rate hike by the fall. This should allow for a faster convergence of inflation toward the target, without undermining growth. The more aggressive market pricing appears to us to be excessive.

Sebastian Paris Horvitz

Director of Research