Central banks must keep their cool

Link

What are the key takeaways from the market news on March 13, 2026? Xavier Chapard provides some insights.

Overview

► Between the ongoing escalation on the ground on both sides and signs that the U.S. administration wants to limit the scale and duration of the energy shock, markets are wavering and remain highly volatile. The magnitude of oil and gas price swings during the week has been extreme (nearly 40 dollars per barrel and more than 10 EUR/MWh), and by the end of the week prices were 50% above their levels at the end of February.

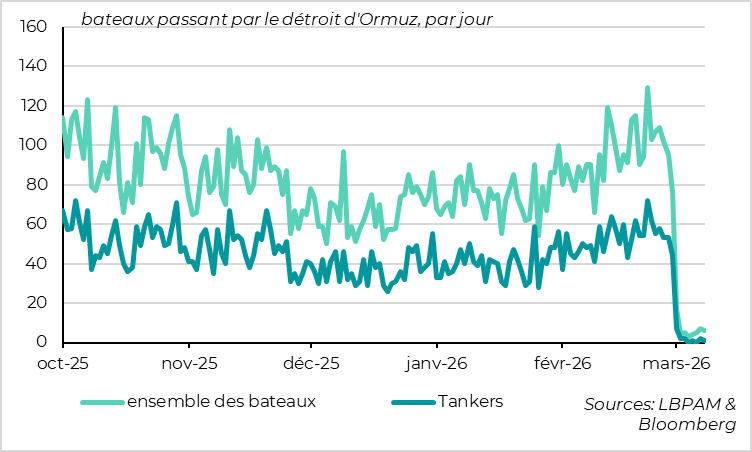

►On the ground, the war has now been going on for 14 days, surpassing the twelve‑day war of last June. Israeli‑American bombardments remain intense and are increasingly hitting civilian infrastructure. For its part, Iran’s strategy of disrupting the energy market is becoming clearer, with the effective closure of the Strait of Hormuz for the past two weeks and attacks on tankers in the Persian Gulf as well as on Omani ports beyond the strait.

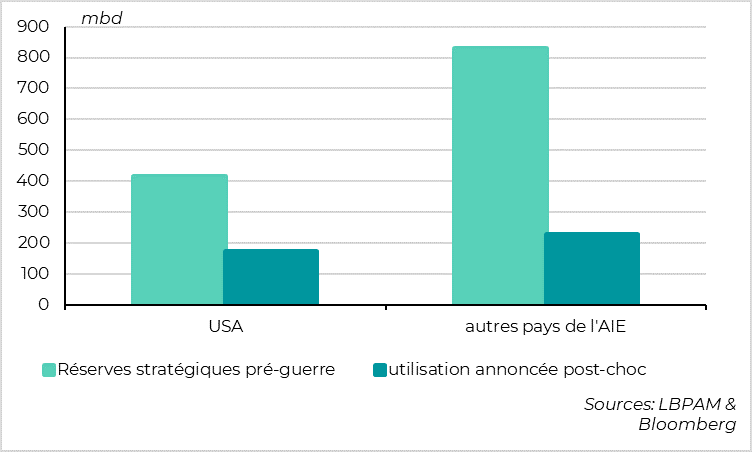

►The International Energy Agency announced that its members will supply 400 million barrels by drawing on their strategic reserves, nearly half of which would be provided by the United States. This is a historic decision that could offset a temporary drop in supply from certain Middle Eastern wells or ports, or a slight reduction in traffic through the Strait of Hormuz. But it is far from sufficient to compensate for a prolonged and significant closure of Hormuz.

►The short‑term risk therefore remains significant. If energy prices were to remain at their current levels for an extended period, this would add 1 percentage point to euro‑area inflation this year and reduce growth by 0.4 percentage point compared with the situation at the end of February. A larger and more persistent shock would jeopardize the economic cycle, even though governments have begun announcing fiscal measures to mitigate the impact.

►That said, we still believe that political pressure in the United States (via public opinion and gasoline prices), as well as economic and geopolitical pressure on Iran (via China), should help ease tensions and lead to a normalization of the oil market within a few weeks. If this proves to be the case, the macroeconomic outlook should remain fairly positive for markets over a 3‑ to 6‑month horizon—especially since, historically, markets tend to rebound quickly once geopolitical risks begin to recede.

►In any case, the extreme uncertainty is not making the task any easier for central banks, four of the most important of which are meeting next week (the Fed, ECB, BoE and BoJ). We believe they will remain on hold while signaling that they stand ready to act if necessary.

►For the ECB, the update of the economic projections will not be particularly meaningful, as the assumptions for energy prices were based on February levels, prior to the start of the war. That said, the ECB staff may present scenarios to help assess the impact of various possible shocks. Since the beginning of the conflict, ECB members have been unanimous in stressing the need to remain calm in the short term, even though most have noted that the risk of a rate hike has increased. We believe it is very unlikely that the ECB will change its rates before June, and that although the risk of a rate hike this year has risen, it remains limited.

►For the Fed, the February inflation data confirmed that inflation was on a slightly downward trajectory but remained well above target, prior to the start of the war. Given the additional rise in inflation already locked in for March and April and the uncertainty surrounding the following months, the Fed will likely feel justified in keeping its rates unchanged in the coming months, while remaining open to either rate hikes or cuts from the summer onward, depending on how inflation and employment risks evolve. This is all the more likely as the U.S. administration is not stepping back on tariffs, having launched investigations this week against 16 major trading partners—including China and the European Union—and promising inquiries into 60 additional countries soon. This confirms that the objective is to keep tariffs durably at their pre–Supreme Court ruling levels.

Going further

Oil: Using strategic reserves only marginally reduces risks

Developed countries release one‑third of their oil reserves

The International Energy Agency announced this week that its member countries will release 400 million barrels of oil onto the market by drawing on their strategic reserves. This is a historic decision that underscores the urgency of the situation. Less than two weeks after the start of the war in Iran, developed countries are committing to ‘spend’ more than one‑third of their insurance against an oil shortage.

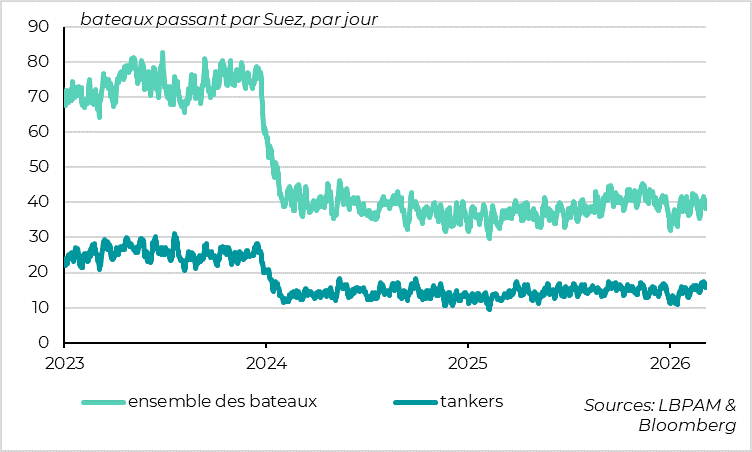

The Strait of Hormuz has effectively been closed for two weeks

This decision is explained by the effective blockage of the Strait of Hormuz. Indeed, only a handful of vessels—and almost no tankers—have passed through the strait since the beginning of the war. This is an unprecedented situation, as Hormuz had never been significantly affected by previous conflicts in the Middle East, not even during the twelve‑day war between Israel/the United States and Iran last June.

The amount of strategic reserves to be released would theoretically be enough to offset the loss of oil supply corresponding to one month of closure of the Strait of Hormuz, which is the duration of the conflict initially anticipated by President Trump at the start of the bombardments.

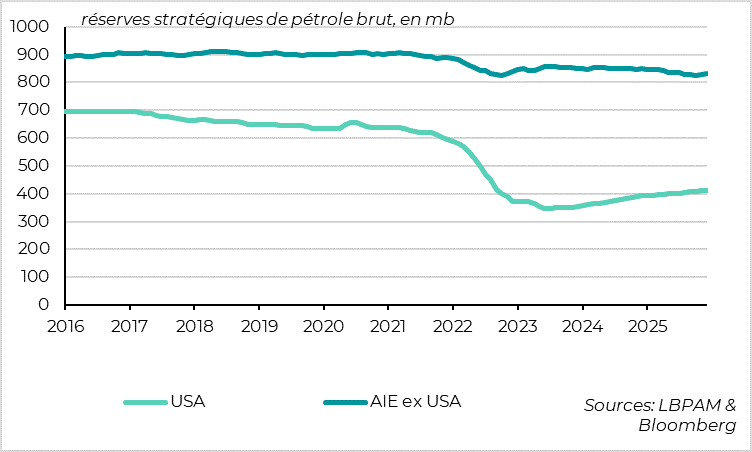

The United States wants to release its oil reserves faster than in 2022

But releasing these reserves quickly onto the market is not that simple.

The United States announced that it would contribute 172 million barrels to the IEA operation, and that these barrels would be released onto the market within 120 days. This implies nearly 1.4 mb per day. This is likely the maximum speed at which the United States can draw on its reserves. Indeed, at the start of the war in Ukraine in 2022, the United States ‘spent’ 200 million barrels but never sustainably exceeded one million barrels per day (a level reached during the summer of 2022).

China: Authorities slightly lower the growth target for 2026

The ability of other governments to draw on their reserves has not been tested

If other countries were to draw on their reserves at the same pace as the United States, this would amount to 3.3 mb/d of supply over the next four months. But this seems like an optimistic estimate, given that these countries have not tapped their reserves in meaningful quantities for decades—not even in 2022.

And even in the most positive scenario, this remains far below the 15–20 million barrels per day that normally transit through the Strait of Hormuz. Adding to this, once these 400 million barrels are released, strategic reserves in developed countries will fall to their lowest levels since the 1980s, which influences market expectations and therefore prices.

Red Sea traffic has still not returned to normal after two years

Overall, the IEA’s announcement provides some reassurance and can offset limited and temporary disruptions to oil supply from the Middle East, but it is no substitute for an almost complete reopening of the Strait of Hormuz. This is essential to avoid an energy shock far larger than the one we are currently experiencing.

Our central scenario is that the war and the blockage of the Strait of Hormuz will come to an end in the coming weeks, because political pressure in the United States is rising rapidly (through public opinion and gasoline prices, with midterm elections approaching) and because both Iran and China need oil to flow through the strait. In that case, oil and gas prices should fall rapidly during the spring and be almost normalized by the summer, allowing the global expansion to continue.

But the risk of a larger and longer‑lasting shock remains significant in the short term. And although the situation is not comparable, the example of disruptions to trade in the Red Sea is not reassuring. Indeed, the actions of an Iranian‑aligned proxy with very limited power have cut commercial traffic by half over the past two years despite the engagement of the international community.

United States: The latest inflation figures support the Fed’s wait‑and‑see stance

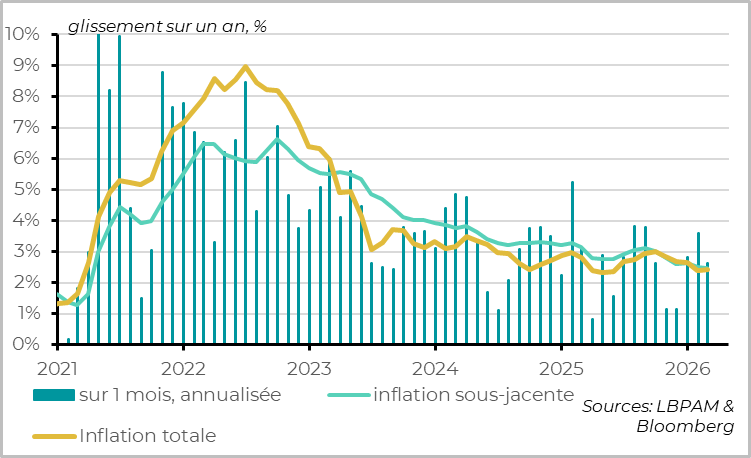

U.S. inflation stabilized just below 3% in February

U.S. inflation, which had been at the center of market concerns in recent years, went almost unnoticed this week. This is understandable, as we know it will rise sharply in March and April due to the oil shock, and that the trajectory in the following months depends almost entirely on developments in the Middle East. Moreover, uncertainty should push the Fed to extend its pause on rate changes at least until the summer.

That said, if the situation normalizes in the coming weeks and the oil shock remains short‑lived, as we assume in our central scenario, the market’s focus will quickly return to the inflation trend and its implications for Fed decisions.

From this perspective, the February inflation figures did not bring much surprise: they confirmed that the inflation trend is very slightly downward, but remains clearly above target, close to 3%.

Indeed, headline and core inflation remained stable in February at 2.4% and 2.5%, respectively. The month‑over‑month increase in core prices slowed slightly in February compared with January (0.2% after 0.3%). But this is still a pace more consistent with inflation remaining between 2.5% and 3% than with inflation in the 2.0% to 2.5% range the Fed would prefer. Especially since the Fed’s preferred measure—the core personal consumption expenditures deflator—is currently above this core inflation gauge (just over 3%).

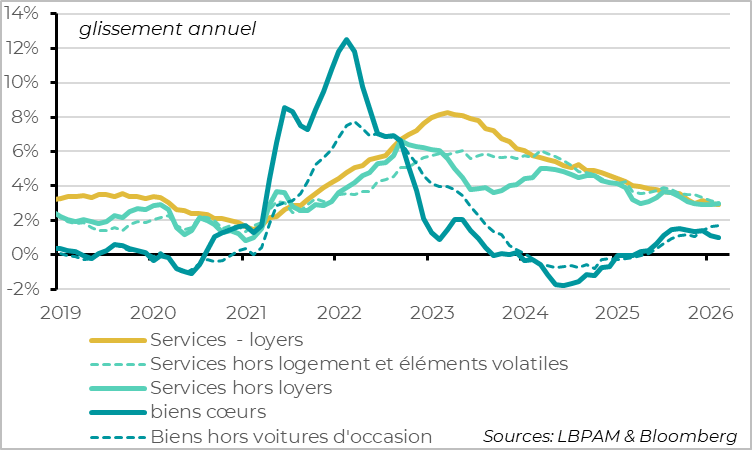

Goods prices are rising slightly, while services prices remain somewhat elevated

The breakdown by component is once again mixed.

Goods price inflation remains contained (+0.1% on the month and 1.0% year‑on‑year), but once again this is due to the decline in used‑car prices. Prices for other goods are rising more noticeably (+0.2% on the month and +1.7% year‑on‑year), which is consistent with the pass‑through from higher tariffs, a process that should continue through the second quarter.

Rents continue to decelerate gradually, falling back below 3% year‑on‑year for the first time since mid‑2021. This is consistent with the slowdown in new rents, although rent inflation is still likely distorted by the impact of the shutdown through April.

Finally, services prices excluding rents—those that best reflect domestic inflationary pressures—remain too dynamic, even if they are rising more slowly than in previous years. Excluding volatile items (such as airfares), prices are still increasing by 3% year‑on‑year and have actually edged up slightly at the start of 2026.

Overall, the pre‑Iran‑war inflation trend was pushing the Fed to keep rates unchanged in the coming months, waiting for inflation to slow more clearly toward target. After the shock, and given the uncertainty surrounding its magnitude and duration, we believe the Fed will maintain this stance of stability at next week’s meeting, signaling that it is prepared to raise or cut rates in the future depending on how risks evolve between inflation and employment.

Xavier Chapard

Strategist