Concerns over Hormuz are resurfacing

Link

What are the key takeaways from the market news on July 10, 2026? Sebastian Paris Horvitz provides some insights.

Overview

►In just a few hours, we find ourselves once again wondering whether the United States and Iran can reach an agreement. Indeed, following the attack on three tankers, which the United States has attributed to Iran, Washington reportedly carried out strikes against Iran. This has created significant uncertainty regarding the viability of the preliminary agreement signed by the two countries just over two weeks ago.

►Indeed, under the 14-point agreement, Iran was expected to guarantee the security conditions necessary for commercial vessels to transit the Strait. At a later stage, it was also supposed to reach an agreement with the Sultanate of Oman on the administration of passage through the Strait of Hormuz. At this point, it is difficult to understand why the Iranian authorities would take the risk of returning to conflict, and why U.S. negotiators have been unable to establish a clear framework governing transit through the Strait.

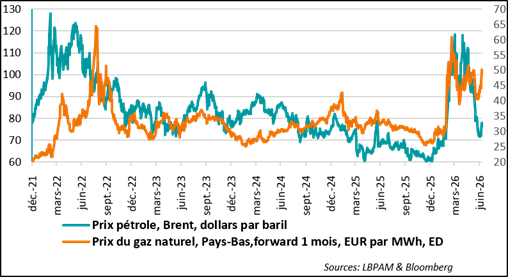

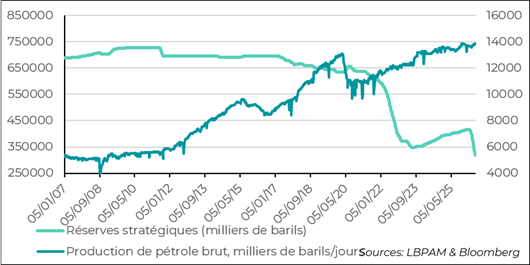

►Nevertheless, one thing remains true: both belligerents have a great deal to lose from a return to war, as would the global economy should the Strait of Hormuz once again be closed for an extended period. In fact, despite the rise in oil prices from their recent lows (+6.5%), the increase remains relatively modest. Like us, the market appears to believe that the current deadlock is not sustainable for either country. It is also worth noting that we had already come close to exhausting our ability to cushion an energy shock through the use of strategic reserves. As a result, natural gas prices have reacted much more strongly to the upside.

►We maintain our reopening scenario, although the probability of a highly adverse outcome has obviously increased. The market has not only refrained from overreacting to the rise in oil prices, but global equity markets have also maintained their upward trend, while sovereign bonds have recovered almost all of the ground lost following the initial announcements of mutual military strikes.

Moreover, discussions between the two countries reportedly remain ongoing.

►Obviously, should the situation deteriorate further, we would need to adapt our investment strategy. For now, however, our stance remains constructive on financial markets over the coming month.

►Furthermore, few economic data releases have been published in recent days that could provide clearer guidance on macroeconomic trends. The only notable development was the release of the minutes from the Fed’s June monetary policy meeting, which merely confirmed the divisions within the Committee. Two distinct camps emerged: one in favor of maintaining the current policy stance, and the other supporting a further increase in policy rates by year-end.

We continue to believe that the Fed is unlikely to overreact to current developments. Nevertheless, it may still deliver one additional rate hike toward the end of the year.

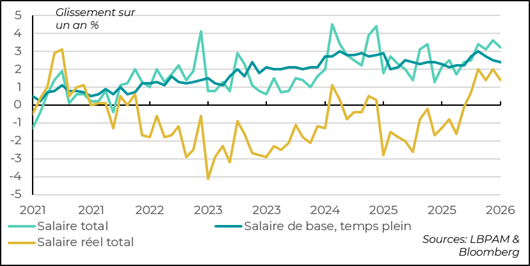

►Turning to monetary policy, Japan’s latest wage data showed that, although wage growth has moderated somewhat, it remains well above inflation. Real wages are still increasing by 1.4% year-on-year. Moreover, the slowdown is largely attributable to calendar effects. This provides an additional argument for the Bank of Japan (BoJ) to take action.

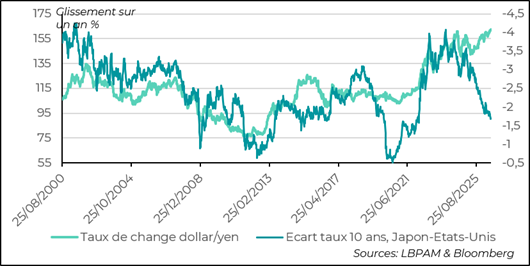

At the same time, the yen has continued to come under downward pressure, with the exchange rate against the U.S. dollar clearly breaking through the ¥160 per dollar threshold. Admittedly, most currencies have recently lost ground against the U.S. dollar. However, the persistent depreciation of the yen is likely to be a growing concern for the BoJ, especially as repeated intervention threats from Japan’s Ministry of Finance do not appear to be doing much to stem the currency’s decline.

Going Further

Hormuz: Is the Reopening at Risk?

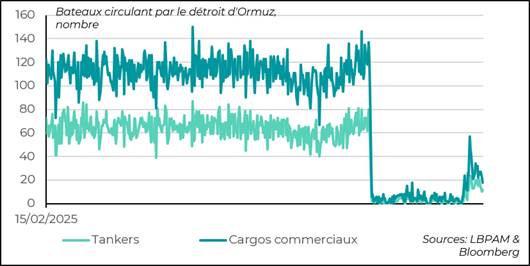

The downward trend in tanker traffic through the Strait of Hormuz is clear

Following the resumption of mutual military attacks between the United States and Iran, tanker traffic through the Strait of Hormuz has, unsurprisingly, declined rapidly. It is difficult to understand why the Iranian authorities are taking the risk of escalating the conflict when the memorandum of understanding had already granted Iran and Oman the prerogative to “control” transit through the Strait. Reigniting tensions can only harm a country that is already economically exhausted and severely weakened.

On the American side, it is somewhat surprising that the ongoing negotiations have not yet succeeded in clarifying the rules of the game and thereby preventing a return to a worst-case scenario.

Be that as it may, both we and the market continue to view the reopening of the Strait as the most likely outcome. Indeed, the costs of a prolonged disruption would be considerable, not only for the two countries involved but also for the global economy as a whole.

Moderate Rebound in Oil Prices, but a Stronger Rise in European Gas Prices

At this stage, markets have reacted relatively moderately, with oil prices rising by around 6.5% from their recent lows. By contrast, European natural gas prices have rebounded by more than 10%.

However, if the current tensions were to persist—or worse, if the Strait of Hormuz were to be closed again—we would likely witness a sharp surge in oil prices. Coming on top of the costs already borne by economies in recent years, such a shock would be highly detrimental to growth while also sustaining inflationary pressures. In particular, such an outcome would likely prove especially damaging for the U.S. President and the Republican Party in the run-up to the midterm elections.

It is also worth noting that we are approaching the limits of the mitigating effect that releases from strategic petroleum reserves have been able to provide in recent years. Many countries, including the United States, have drawn heavily on their oil stockpiles to cushion supply shocks. In the case of the United States, reserve levels are now at historically low levels. As a result, any new oil supply shock would likely have a much greater impact on both energy prices and the global economy.

Japan: Wage Growth Adds to Pressure on the BoJ… Not to Mention the Yen

In Japan, the latest wage data showed that wages continue to grow at a strong pace, well above inflation. On a year-on-year basis, wages rose by 3.2%, marking a slowdown compared with the previous month. However, this moderation is largely explained by calendar effects, as the number of working days was lower during the period. Once adjusted for these effects, the underlying trend still points to robust wage growth.

In fact, real wages—that is, wages adjusted for inflation—continue to increase at a solid pace of 1.4% year-on-year. Despite the recent slowdown, which is likely to be reversed next month, the overall trend remains very strong.

This is yet another factor that should add pressure on the Bank of Japan (BoJ) to continue raising interest rates, or even to accelerate the pace of monetary tightening. Indeed, at this stage, two additional rate hikes before the end of the year cannot be ruled out.

The Yen Continues to Slide

Moreover, the continued slide of the yen can only be a source of concern for the BoJ. Rising long-term bond yields may already be seen as a sign of a growing mismatch between monetary policy—which remains far too accommodative—and both the expected inflation trend and the underlying strength of the economy.

It is possible that the BoJ’s gradual approach to monetary policy normalization has reached its limits. What is clear, however, is that repeated intervention threats from Japan’s Ministry of Finance do not appear to be restoring confidence in the currency or slowing its depreciation.

Sebastian Paris Horvitz

Director of Research