D. Trump weakened by the Supreme Court

Link

What are the key takeaways from the market news on february 24, 2026? Sebastian Paris Horvitz provides some insights.

Overview

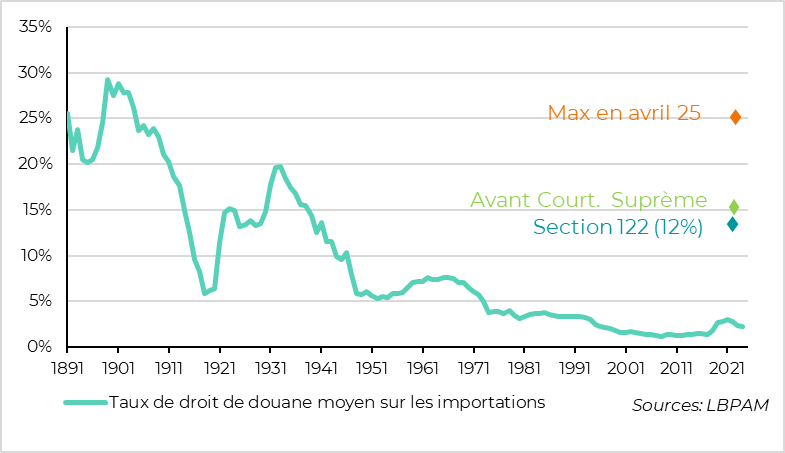

► Ultimately, the U.S. Supreme Court has delivered its verdict: it was illegal to raise tariffs on almost all of the country’s trading partners by invoking the ‘International Emergency Economic Powers Act,’ enacted in October 1977. As a result, the so‑called reciprocal tariffs are now abolished. However, the more specific tariff increases remain in place, as the government had referred to other pieces of legislation for those.

►This decision is, first of all, a defeat for D. Trump, who until now had repeatedly received the support of the Supreme Court and of the Republican‑appointed judges who make up the majority. For the first time, the president sees his powers limited. However, it is difficult to conclude from this that the Court’s judges have undertaken a radical shift in their approach to the president’s controversial actions. Nonetheless, this may prove to be a turning point for certain decisions of the U.S. administration.

► Regarding the economic impact of the decision, it is difficult to clearly determine all the effects. First, there is uncertainty around the reimbursement of the 'illegal' taxes collected by the government so far. The amounts would exceed 150 billion dollars.

On the other hand, the government reacted quickly by using Law 122, which allows the president to raise customs duties by up to 15%. As a result, an increase of this magnitude has been applied to all countries for a period of 150 days (renewable with the Senate's approval).

In its current form, this would slightly change the average tariff rate on imports (lower than before). More importantly, it introduces ambiguity regarding the agreements already concluded with the country's trade partners.

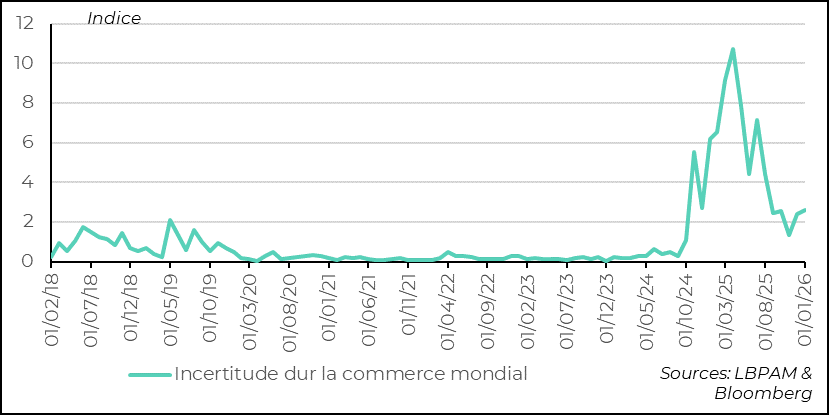

Overall, although the U.S. government could recover a significant share of the expected revenue through this new measure or by using other mechanisms, this move nevertheless reintroduces uncertainty into trade relations and may intensify wait‑and‑see behavior among economic agents, thereby slowing down activity.

► This uncertainty adds to the anxiety that still prevails in the markets regarding the impact of the rise of artificial intelligence (AI) on certain sectors (such as software producers), as well as the uncertainty surrounding the profitability of the massive infrastructure investments currently being made in AI. As a result, U.S. stock indices continue to come under pressure, while safe‑haven assets—such as sovereign bonds and gold—are attracting investors.

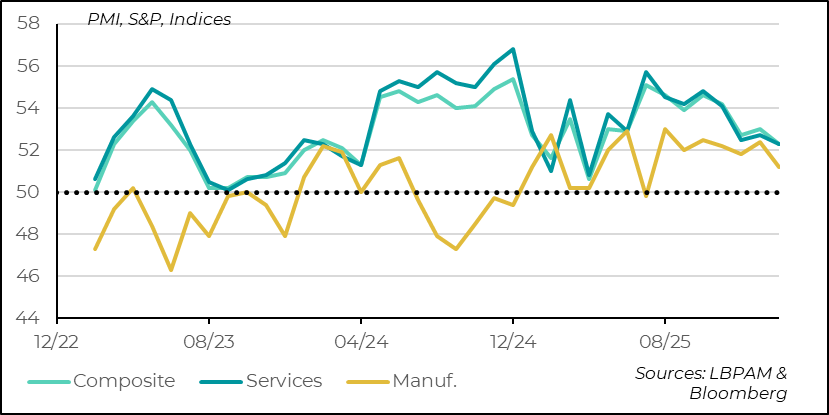

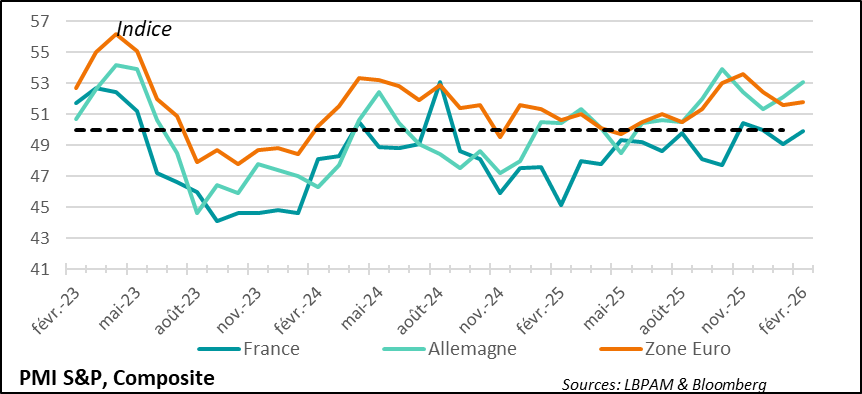

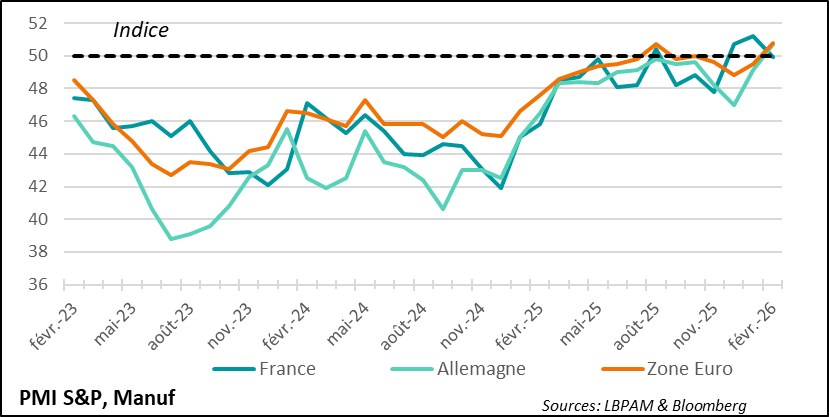

►At the same time, in contrast with the prevailing sense of unease in the markets, S&P’s preliminary PMI surveys for February for the major economies showed that activity remained resilient at the start of the year. This resilience was particularly evident in Asia and Europe. In Japan, the composite index (services and manufacturing) continued to rise, approaching 54. Similarly, in the Eurozone, as well as in the United Kingdom, composite indices edged higher, remaining in expansion territory.

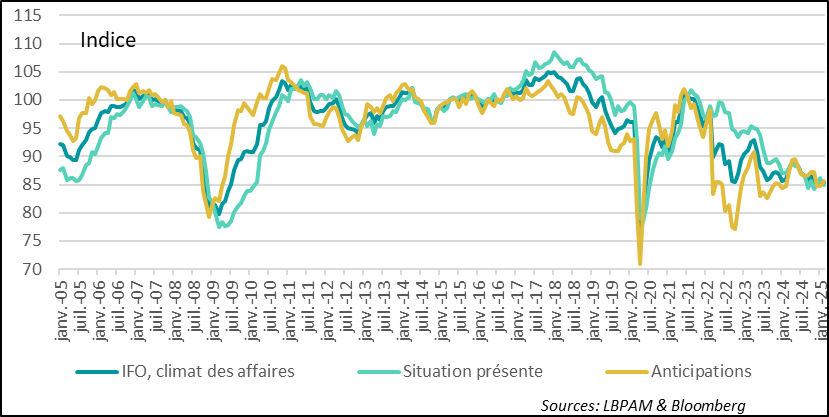

►In the Eurozone, the good news came from Germany, where the composite index rose by one point, but more importantly, the manufacturing index moved back into expansion territory for the first time since 2022. This improvement in German activity was reinforced by the IFO survey, which also presented a more optimistic outlook. This suggests that the effects of the German stimulus plan are beginning to take hold, even though the export sector remains less robust.

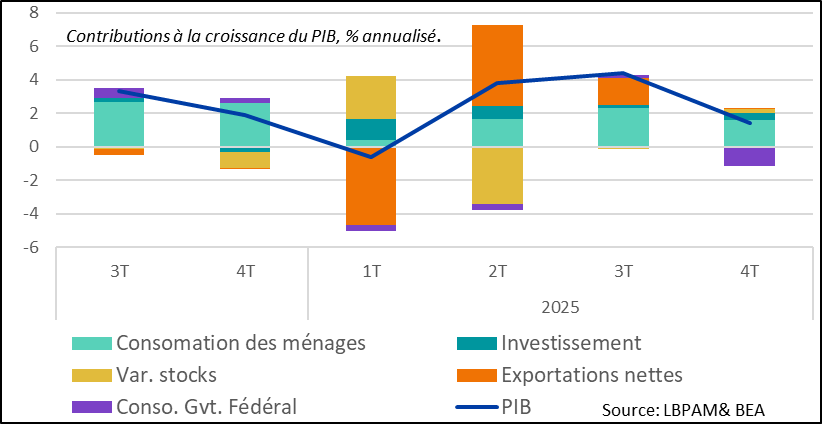

►In the United States, however, the S&P PMI survey was more disappointing, showing a continued slowdown in activity following the slight rebound of the previous month. Nevertheless, activity in both services and manufacturing continues to grow. This deceleration also echoes the much weaker‑than‑expected GDP momentum in Q4 2025, with GDP increasing by only 1.4% at an annualized rate. This was largely due to the strong negative contribution of public spending linked to the shutdown. However, household consumption also lost momentum. We still expect a more virtuous dynamic to take shape during the first half of 2026, particularly with an improvement in labor market conditions.

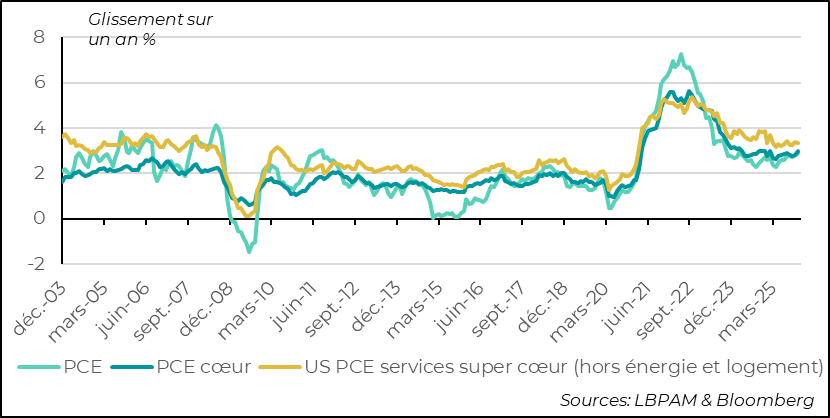

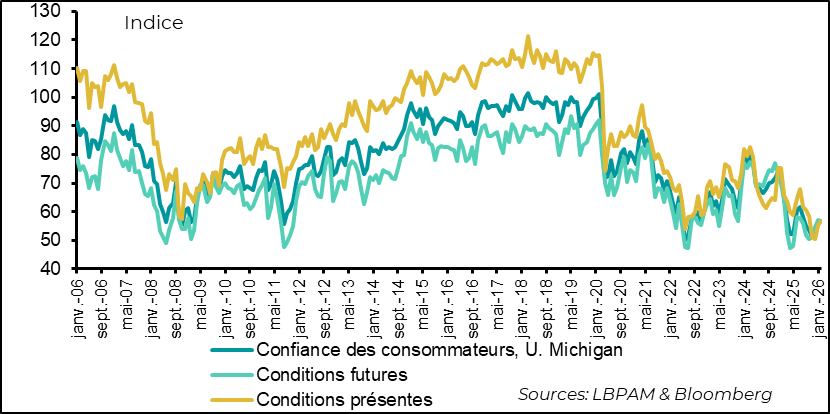

►This improvement in the labor market is necessary to counteract the negative effect of inflation on purchasing power. Indeed, inflation in December, measured by the Personal Consumption Expenditures (PCE) deflator—the Fed’s preferred gauge—accelerated to 2.9% in December, and to 3% year‑on‑year excluding energy and food (core). At the same time, although inflation expectations have eased slightly, household confidence remains rather weak, with a slight dip at the end of February according to the University of Michigan survey. We expect confidence to recover somewhat as labor‑market dynamics strengthen, which should support consumption.

Meanwhile, an economy that remains resilient and inflation that is somewhat elevated are not very compatible with a Fed that would turn more aggressive in cutting policy rates. We still expect only one rate cut in 2026.

Going Further

United States: Tariff Disorder as a Source of Uncertainty

Towards Slightly Lower Tariffs?

The decision by the U.S. Supreme Court to declare the use of the ‘International Emergency Economic Powers Act (IEEPA)’ illegal was expected. But the strong majority (6 to 3) that formed within the institution to support this outcome was less so. Above all, the Court’s reasoning emphasized that the President does not hold all powers—specifically not the authority to determine taxes or customs duties, which is the prerogative of Congress. Thus, for the first time, the Supreme Court is showing that there are limits to presidential power.

As a result, the IEEPA, which was enacted in 1977, can no longer be used by the President as a permanent threat against trade partners. Likewise, the tariffs already imposed under this law are therefore invalid. This should lead to the reimbursement of revenues collected by the federal government, estimated at more than 150 billion dollars. However, such reimbursements may take a long time.

To offset these revenue losses, the government immediately turned to another legal tool, known as ‘Section 122,’ which allows the President to raise tariffs on a country by up to 15% and for a maximum of 150 days (renewable only with Senate approval). Thus, on Sunday, President Trump imposed a unilateral 15% tariff on all countries.

At this stage, there are therefore winners and losers. Brazil (–13 points), China (–7 points), and India (–6 points) would emerge as winners in this situation, whereas the European Union would be marginally worse off (+1 point). Overall, as it stands, the average tariff rate on U.S. imports would fall slightly to 12%, compared with 14% today. Nevertheless, it would remain historically high.

At the same time, it should not be forgotten that other specific tariffs have been imposed under other laws. These tariffs are expected to remain in place. In addition, the U.S. government has indicated that it is prepared to launch investigations into imported goods from each country to impose new duties in order to protect against practices deemed harmful to the U.S. economy. But at this stage, it remains unclear which products could be affected.

A Likely Rise in Global Trade Uncertainty

Many countries that had signed agreements with the United States now find themselves in a state of uncertainty. Several have therefore decided to put these agreements on hold and are waiting for greater clarity on the new tariff rules that will be adopted.

It is clear that new negotiations will have to take place. However, the U.S. administration could be constrained by this new context and may have less latitude to impose arbitrary tariffs.

What is certain is that this situation creates uncertainty for the months ahead. At this stage, the market is expecting the status quo, and the Supreme Court decision has therefore not caused major turbulence. We also believe that the average tariff rate should remain relatively stable in the long run. Nonetheless, it is evident that upcoming negotiations and the potentially erratic nature of future U.S. government decisions—by increasing uncertainty—could undermine confidence and weigh negatively on economic activity. This is therefore a key risk to monitor for short‑term growth prospects.

United States: Growth Has Weakened While Inflation Remains Elevated

GDP growth slowed sharply in Q4 2025

U.S. GDP growth slowed sharply in Q4 2025, to 1.4% from 4.4% in the previous quarter. This was well below expectations. In fact, it now appears clear that forecasts had underestimated the impact of the shutdown on federal government spending. Indeed, federal spending made a negative contribution to GDP growth of more than one percentage point. However, household consumption also slowed sharply over the quarter, as did other components of demand.

Despite this slowdown in Q4 2025, carry‑over growth for Q1 2026 remains positive, while the effects of last year’s shutdown will fade at the beginning of the year.

PMIs Weaken in February

At the same time, the February PMI surveys delivered a mixed message regarding the evolution of activity across the Atlantic. The preliminary composite index (services and manufacturing) from the S&P PMI survey erased the rebound seen the previous month and returned to a downward trend, although it still remains in expansion territory. This slowdown in the pace of growth affected both services and manufacturing, notably due to weaker momentum in new orders.

At the same time, according to the survey, business confidence about the outlook remains high, with firms still counting on the positive effects of the fiscal support measures being implemented at the start of the year.

Inflation (PCE) Remains Elevated

Part of the weaker demand growth can be explained by inflation remaining elevated. Indeed, inflation measured by the Personal Consumption Expenditures (PCE) deflator—the Fed’s preferred gauge—rose more than expected last December, reaching 2.9% year‑on‑year for headline inflation and 3% for core inflation. This could become a constraint on consumption if real wages were to slow further.

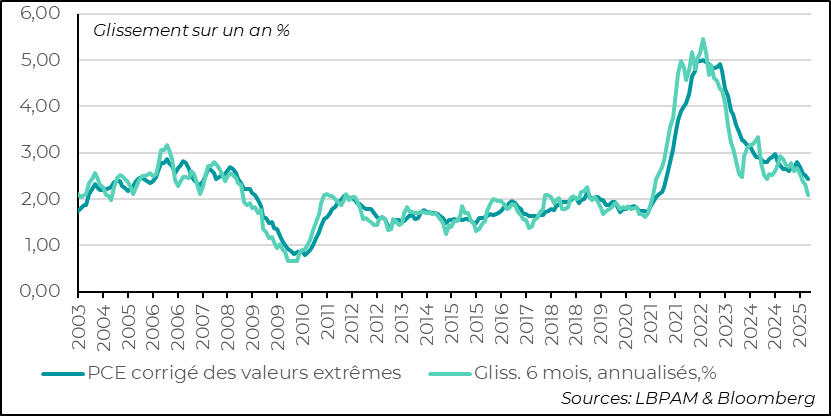

Trend Measures of Inflation Are Slightly More Reassuring

At the same time, some trend indicators—such as the Atlanta Fed’s measure, which excludes extreme price variations—point to a more reassuring pattern, showing a deceleration.

However, it is important to continue highlighting that inflation statistics still appear to be affected by information gaps linked to the shutdown period. In our view, it will take a few more months before they return to normal.

Nevertheless, given our growth forecasts, including an expected improvement in labor‑market conditions, we continue to believe that inflation will only slow gradually over the course of 2026, which would prevent the Fed from adopting an overly aggressive pace of rate cuts in 2026.

Household confidence remains weak

Another area that remains a concern is U.S. consumer confidence. It resumed its downward trend at the end of February and remains historically low. Although the relationship between this measure and consumption has been weak over the past year, an improvement in confidence would be welcome to help support growth.

Eurozone: PMI Surveys Remain Reassuring

The composite PMI index in February remains in expansion territory, driven by Germany

S&P’s preliminary PMI survey for February showed that activity in the Eurozone remains in expansion territory, with even a slight improvement. The composite index (services and manufacturing) continued to gain ground, reaching 51.9. Germany contributed significantly to this increase, with its composite index moving higher again. However, despite this rebound, activity there still remains in contraction territory.

PMI data indicate that industrial activity in Germany is rebounding sharply

The most notable aspect of the survey is the rebound in manufacturing activity in Germany. Indeed, the PMI for the manufacturing sector has reached its highest level since 2022 and has finally returned to expansion territory. This appears to reflect the beneficial effects of the German stimulus plan, which are now starting to bear fruit, even though the survey indicates that the export sector remains fragile.

The IFO survey confirms the improvement in Germany

The positive news from the PMI survey is corroborated by the IFO survey, which showed a rebound in the IFO index in February—both in current conditions and in expectations. We continue to expect German growth to gain momentum in the first half of 2026 and to support, at least partially, the rest of the Eurozone.

Sebastian Paris Horvitz

Director of Research