Finally an important first sign of de-escalation

Link

What are the key takeaways from the market news on April 10, 2026? Xavier Chapard provides some insights.

Overview

► The United States and Iran announced a two‑week ceasefire on Tuesday evening, during which intense negotiations for a more lasting solution are expected to take place. This will begin as early as this weekend in Islamabad, with the presence of U.S. Vice President Vance.

►This is only a first step toward de-escalating the conflict and normalizing energy flows, and significant risks remain, particularly regarding the reopening of the Strait of Hormuz. But it is still very good news for the global economy, as it reduces the risk of an energy shock far greater than the one already experienced and shows that both sides have an interest in stopping the escalation. And for the markets, it confirms that TACO is still very much at play (the idea that Trump backs down when the cost of his actions becomes too high).

►Overall, the situation seems to be unfolding as we anticipated in our baseline scenario — namely, that de‑escalation would begin during April. If this leads to a relatively quick, though incomplete, decline in energy prices by the summer, the global cycle should be preserved despite the slowdown that will still occur mid‑year.

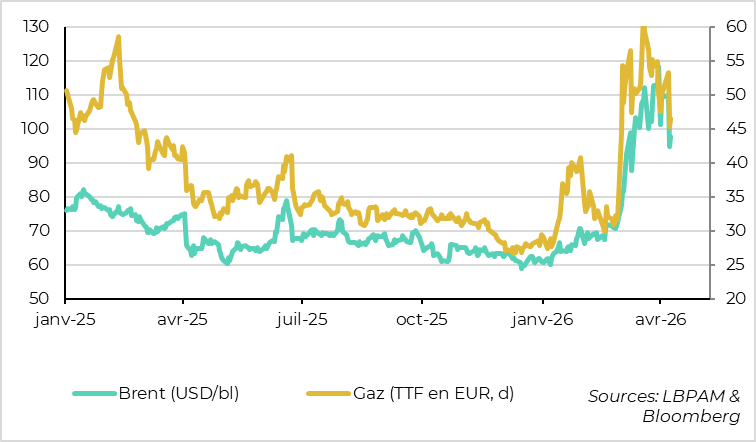

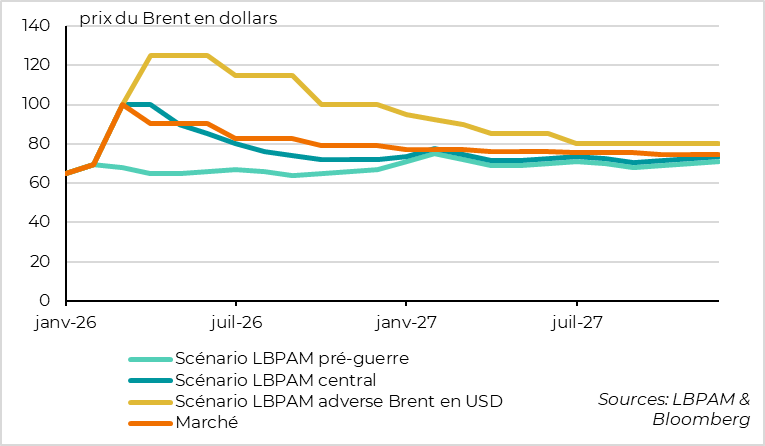

►As expected, markets reacted strongly after the announcement of the ceasefire. Oil prices fell back below 100 dollars per barrel after approaching 120 dollars at the end of March, although they remain well above the pre‑crisis 60–70 dollar range. And the uncertainty indicator known as the VIX (the implied volatility of U.S. equity markets) has returned to its pre‑war level, below 20%. That said, the rebound in assets is only partial, with markets recovering on average about half of March’s decline, particularly for riskier assets outside the United States and for rates.

►Given the markets’ measured reaction, we remain moderately positive on risk assets, even though we believe that the next phase of the market rally will be more gradual and uncertain than this week’s rebound.

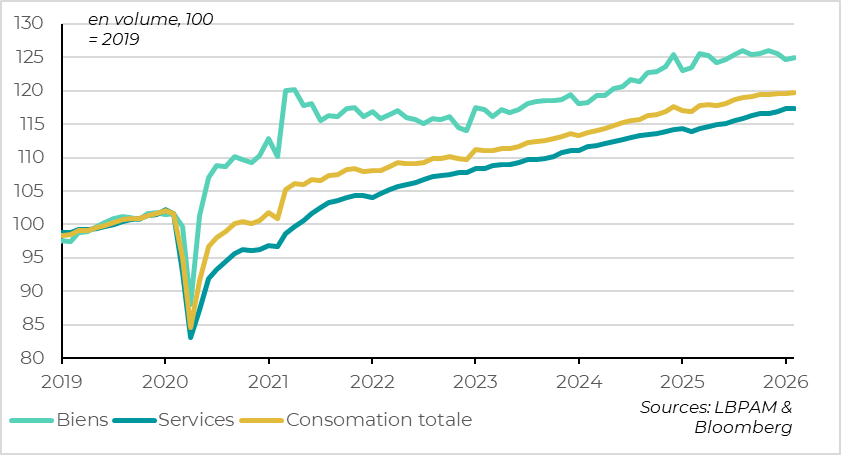

►On the data front, the latest U.S. figures regarding the post‑war situation are reassuring (a rebound in employment in March and a decline in jobless claims, as well as resilient household and business confidence indicators…). But the economic activity data reflecting the pre‑war situation indicate that momentum was weaker than expected before the conflict. This is particularly true for consumption, which slowed to below 2% in Q4 2025 and stalled in January and February. This does not call into question the continuation of growth in early 2025, but it does highlight the importance of a stabilizing labor market and continued normalization in business confidence. These are necessary to support household incomes, especially at a time when households are about to face the energy shock.

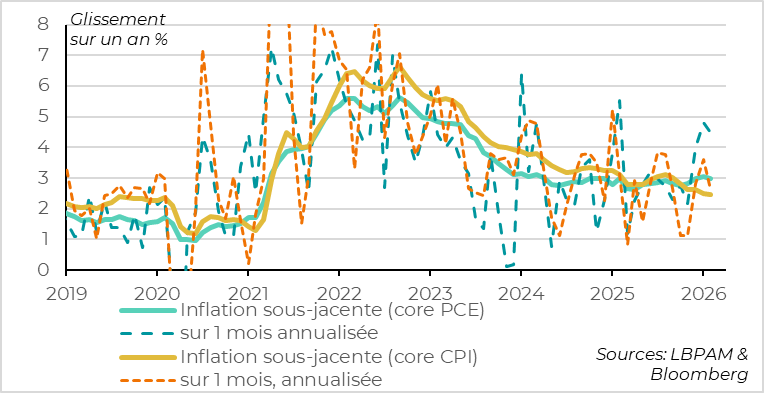

►The Fed’s preferred measure of inflation edged up slightly at the start of 2025 and remained too high, at 3% in February. This is mainly due to rising core goods prices, driven by the lagged impact of tariffs as well as tensions in Tech supply chains. This should reinforce the Fed’s caution before considering further rate cuts, as confirmed by the minutes of its latest meeting. We still believe the Fed will keep rates unchanged this year before cutting them one last time next year, provided inflation resumes its decline toward the target.

Going further

World: A fragile ceasefire that significantly reduces extreme risks

Energy prices are falling quickly but only partially after the announcement

The market’s reaction to the ceasefire was immediate, as one would expect from the first sign of de‑escalation. Oil and gas prices have reversed half of their peak increase since the start of the war.

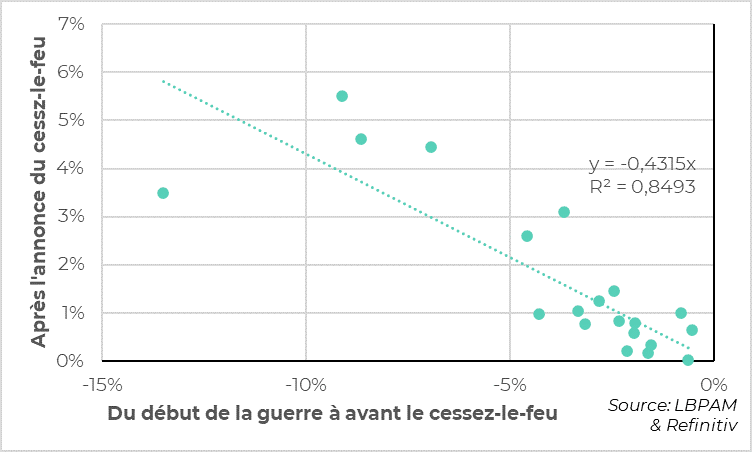

Assets have generally recovered half of their March decline

Similarly, financial assets have generally recovered half of their March decline. However, this rebound is uneven, with a more complete recovery in U.S. risk assets compared with European and Asian assets, and only a very partial pullback in interest rates relative to their pre‑war levels.

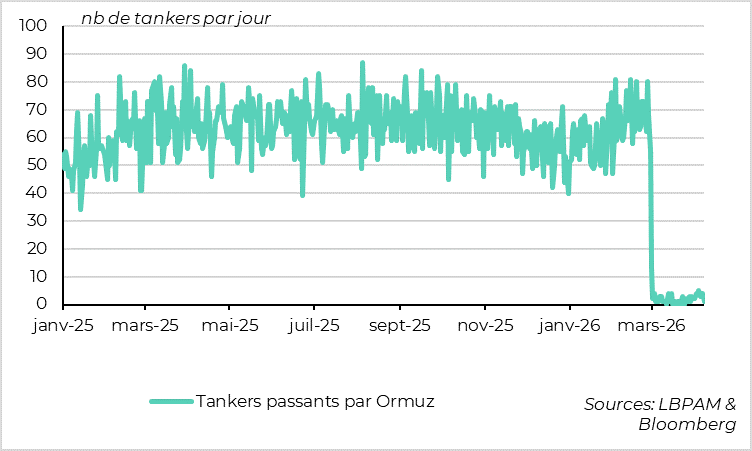

The scale and speed of the reopening of Hormuz remain the key issue

A great deal of uncertainty and risk remains.

The ceasefire is fragile and could be called into question before the end of the two‑week period. Indeed, strikes have continued to be reported on both sides since the announcement. Moreover, it is unclear whether Lebanon is included in the ceasefire. Most importantly, the ceasefire includes the reopening of the Strait of Hormuz, which in practice remains closed two days after the agreement.

Next, the ceasefire is meant to allow for intense negotiations toward a more lasting solution. But these negotiations are likely to be extremely challenging, as the positions of the two sides differ considerably — particularly regarding Iran’s nuclear program, Iran’s support for its proxies, and long‑term control of the Strait of Hormuz.

Finally, much uncertainty remains about the scale and speed at which Middle Eastern energy supply (oil and gas) will normalize. This will depend, of course, on the conditions under which the Strait of Hormuz reopens as well as on the extent of damage to energy and port infrastructure.

The market scenario is realigning with our baseline scenario

That said, this ceasefire — even if fragile — and the start of negotiations — even if extremely difficult — are nevertheless very good news for the economy and for markets.

It shows that both sides have an interest in stopping the escalation, which reduces the risk of a very negative scenario for the global economy. We also learn that several countries are involved beyond the belligerents, notably China (in addition to Pakistan, Turkey, and Egypt). This makes the process more credible. And it significantly reinforces TACO, meaning markets should now be somewhat less sensitive to belligerent statements from the U.S. administration. This is positive in itself, as it reduces the risk of an abrupt tightening in financial conditions, which would amplify the economic impact of the energy shock.

Overall, the energy market has returned to a scenario close to our baseline, whereas it was moving toward our adverse scenario before the ceasefire announcement.

In this context, the market rebound seems reasonable to us, especially since it has been supported by increasingly defensive investor positioning. We remain broadly positive on risk assets in the medium term, even though the upward trend is likely to be more gradual and uncertain than this week’s rebound. As for interest rates, markets have only priced out one rate hike from the ECB and the BoE, meaning they continue to expect more rate increases than we do. We therefore remain positive on sovereign bonds, particularly at the short end of the curve.

United States: Consumption slowed more than expected before the energy shock

Consumption slowed at the turn of the year

While the latest U.S. data on the post‑war situation are reassuring (a rebound in employment in March and a decline in jobless claims, as well as resilient household and business confidence indicators…), the activity data reflecting the pre‑war economic situation indicate that momentum was weaker than expected before the conflict.

GDP growth for Q4 2025 was revised down once again, from 0.7% to 0.5%. This figure overstates the weakness of the economy, as it includes a 1‑percentage‑point negative contribution from public demand linked to the October/November shutdown. But it does appear that underlying growth slipped below 2% at the end of 2025, mainly because of a slowdown in household spending. Consumption indeed slowed from 3.5% to 1.9% in Q4, and residential investment continued to decline at the end of 2025.

Consumption also remained weak in January and February. It rose by only 0.1% in February after stagnating in January. While goods consumption has stabilized after two months of declines around the turn of the year, services consumption is now slowing, whereas it had been holding up well until then.

ore inflation was therefore normalized before the energy shoReal household incomes have been stagnating since late 2025

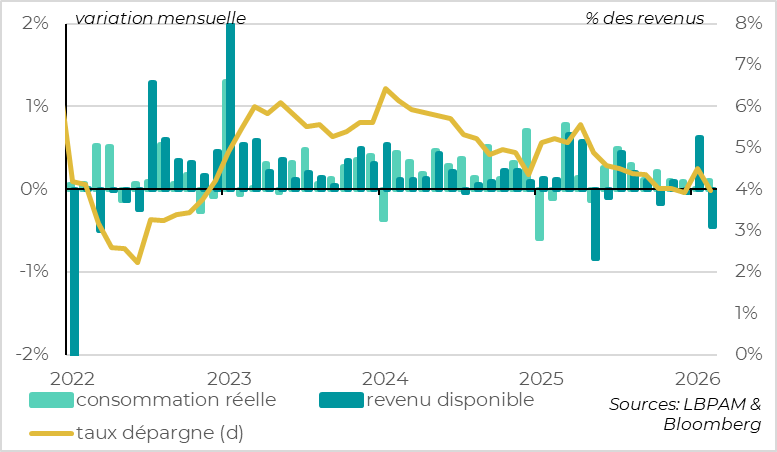

The weakening of consumption is mainly explained by the stagnation in household incomes since the fourth quarter, while the savings rate is already low, as households smoothed last year’s tariff shock. Indeed, incomes reversed their January rebound in February and, despite limited consumption, the savings rate fell back to 4%, its lowest level since 2022.

These data do not, at this stage, call into question our expectation of a slight rebound in growth in Q1, driven by the normalization of public spending after the end of the shutdown, followed by resilient growth in subsequent quarters supported by tax cuts and strong investment dynamics in the Tech sector. But they do show that the U.S. economy was somewhat more fragile than anticipated at the turn of the year, just as households are set to face a decline in purchasing power in Q2 due to the energy shock. This reinforces the importance of a stabilizing labor market and resilient business and household confidence to prevent a more pronounced slowdown in the middle of the year.

United States: The Fed is likely to remain on hold even as energy prices retreat

The Fed’s preferred measure of inflation remained too high before the war

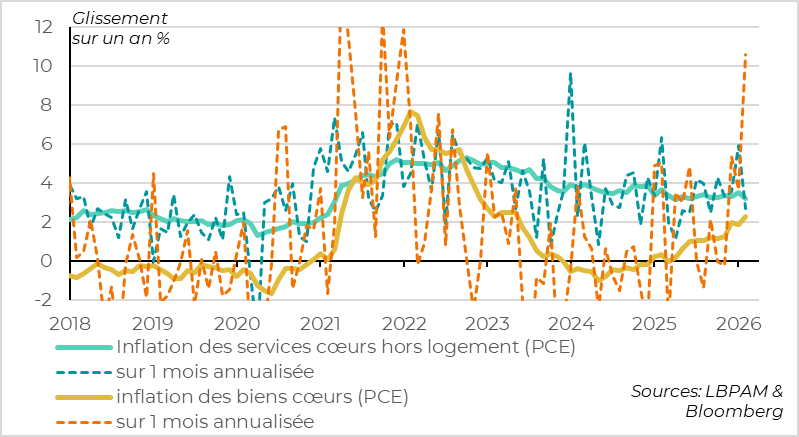

The Fed’s preferred measure of inflation, the personal consumption expenditures price index excluding energy and food (core PCE), is still not slowing toward the target, unlike underlying inflation (core CPI). Indeed, prices rose by 0.4% in February, the same as in January, according to this measure. Year‑on‑year, core PCE slowed only marginally, from 3.1% to 3.0%.

This is a problem for the Fed because core PCE inflation remains well above the target, at 3%, and, more importantly, it has not been slowing for the past two years. It has even reaccelerated in sequential terms since the end of last year, which should prompt the Fed to remain cautious if it wants to preserve its credibility regarding its 2% target.

Inflation expectations continue to rise

The strong increase in prices in February in core PCE came from manufactured goods, whose prices rose by 0.8% over the month and by 2.3% year‑on‑year — their fastest increase since 2022. This sharp rise reflects the pass‑through of last year’s tariff hikes as well as higher prices for Tech‑related products due to tensions in supply chains. That said, we expect core goods prices to begin easing from the summer onward, once the impact of tariff increases starts to fade.

By contrast, core services inflation slowed in February after the sharp upward adjustments in January, which is reassuring. Housing inflation has returned to its pre‑Covid level (3.1%), and non‑housing services inflation slowed from 3.5% to 3.2%. It remains somewhat too high but should continue to ease as wage pressures have normalized.

Overall, the inflation measure targeted by the Fed is likely to remain persistently around 3% until the summer. We expect it to slowly drift back toward the target in the following years, but the risk of inflation remaining durably above target persists, especially if supply shocks continue to multiply.

This is why the Fed has become more cautious regarding rate cuts since late 2025 and is likely to maintain that stance even if energy prices fall quickly. In fact, since second‑round effects from energy on underlying inflation are limited in the United States, and since lower energy prices reduce risks to employment, one could even imagine the Fed being more patient if the energy shock turns out to be smaller than expected.

The minutes from the Fed’s mid‑March meeting indicate that ‘almost all participants’ believe the current policy rate leaves the Fed ‘well positioned’ for upcoming rate decisions. This suggests a prolonged pause.

Beyond that, the Fed retains a slight easing bias. ‘Most participants expressed concern that a prolonged conflict in the Middle East could lead to further weakening in the labor market, which could justify additional rate cuts.’

But this dovish bias is narrowing. ‘Many participants highlighted the risk that inflation could remain elevated for longer than expected in a context of persistently rising oil prices, which might require a rate hike.’ Importantly, ‘some participants’ even wanted the post‑meeting statement to indicate that the next rate move could be either up or down, to reflect the possibility that rate increases might be appropriate if inflation were to remain above target.

Overall, we continue to expect the Fed to keep rates unchanged this year at 3.5–3.75%, before considering a rate cut early next year if underlying inflation shows clearer convergence toward the target.

Xavier Chapard

Strategist