Global activity shows signs of improvement

Link

What are the key takeaways from the market news on July 7, 2026? Sebastian Paris Horvitz provides some insights.

Overview

►While the situation in the Strait of Hormuz appears to be improving very gradually, with the number of vessels able to transit remaining low, markets continue to anticipate a normalization of oil flows, potentially resulting in an oversupply in the coming months. As a result, the price of Brent crude oil remains relatively low, averaging around $73 per barrel. Although we believe prices could converge toward a somewhat higher level, the easing of the energy shock should help consolidate the recovery in global economic activity.

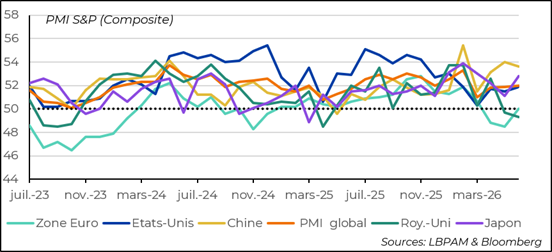

►In this context, the release of S&P’s June PMI surveys for the world’s major economies sends a positive signal for the outlook, with a slight improvement, although activity levels remain below their historical average.

►As a result, the global composite PMI (manufacturing and services), compiled by JPMorgan based on S&P PMI surveys, improved in June. However, it remains below the level that prevailed before the outbreak of the war in Iran.

►It is important to emphasize that this renewed momentum was driven primarily by the services sector, in contrast to previous months, when manufacturing had shown greater strength. More importantly, this rebound suggests that businesses, overall, are once again seeing an improvement in the outlook, although optimism remains moderate. To some extent, this is clearly the result of the announcements regarding the reopening of the Strait of Hormuz that companies had received at the time of the survey. It is reasonable to expect even more encouraging signs to emerge as early as next month.

►At the regional level, emerging economies, particularly in Asia, continue to experience the strongest expansionary momentum, although India, which has been affected by the energy crisis, is seeing a slowdown in services activity. This favorable momentum in Asia is also benefiting Japan. By contrast, Europe remains at the bottom of the global ranking, even though the situation is improving.

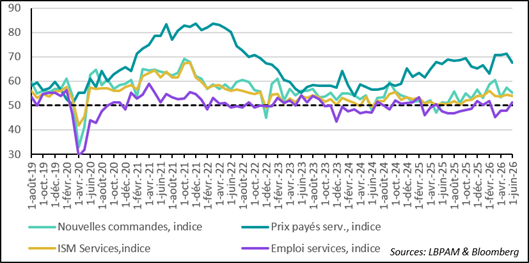

►In the United States, S&P’s services survey showed a slight improvement in activity, which has reached its highest level since the start of the conflict with Iran, although it remains well below the average recorded over the past year. The ISM services survey, by contrast, showed a slight decline. However, both surveys continue to point to a services sector that is displaying limited momentum. The good news, unsurprisingly and as in the manufacturing sector, is the decline in cost indicators, in line with the easing of energy prices.

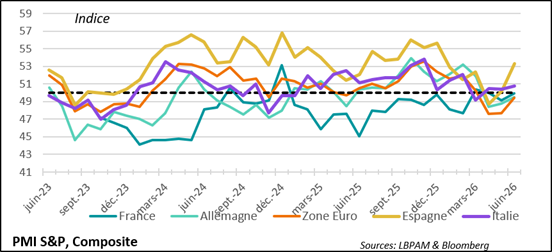

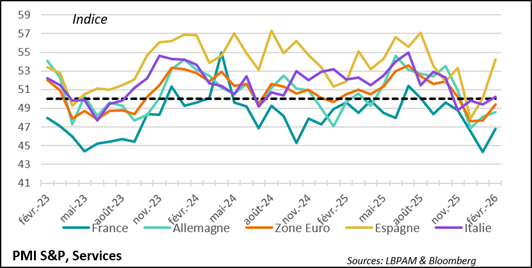

►In the Eurozone, the composite PMI edged up in June, allowing the region to emerge from contraction territory and stabilize. This improvement was driven by stronger activity in the services sector, which helped support the overall rebound, albeit a modest one. Most importantly, nearly all Eurozone countries saw conditions improve in this sector, which has suffered significantly since the outbreak of the war.

As elsewhere, price pressures are easing, with the first signs of declining energy prices beginning to emerge. This improvement remains consistent with our scenario of a gradual recovery, with a more pronounced acceleration expected in the autumn.

Going Further

Global Activity: A Modest Rebound Driven by Services

Global Activity Improves Slightly in June, According to PMI Surveys

S&P’s final PMI survey for June, covering all sectors and major economies, showed an improvement in global activity. Indeed, the global PMI index compiled by JPMorgan from S&P surveys edged higher, although it remains below the average level that prevailed before the war in Iran.

This increase was driven primarily by the services sector, which is beginning to recover after having been the segment most affected by the energy shock. This contrasts with previous months, when manufacturing was the main driver of global growth.

At the regional level, emerging economies, particularly in Asia, continue to display stronger momentum than the rest of the world. Nevertheless, in India, which remains the major economy showing the strongest growth momentum, services activity continued to slow, although it remains firmly in expansion territory as a result of the energy shock.

Elsewhere in Asia, Japan has also benefited from strong support to activity, driven by a weak currency and government measures supporting consumption, including the capping of energy prices.

As elsewhere, the easing of the energy shock caused by the war should help support a rebound in global economic activity.

Eurozone: Activity Stabilizes After Two Months of Contraction

In the Eurozone, S&P’s PMI survey showed a recovery in services activity, which allowed the composite index (manufacturing and services) to rebound and move out of contraction territory, where it had remained for the previous two months. This rebound has been broad-based, affecting all of the major economies in the region.

Eurozone: Services PMI Rebounds

The rebound in services activity was quite remarkable across the Eurozone, with Spain in particular showing a strong resurgence in momentum.

This is good news for the region, which has been one of the areas most affected by the energy shock. With energy prices expected to continue declining significantly, we can expect a further improvement in sentiment and, above all, a reversal of the negative impact on purchasing power that characterized previous months.

A recovery in consumer spending, together with the continued implementation of Germany’s stimulus plan, should help the Eurozone regain momentum in the months ahead.

Furthermore, we continue to believe that the ECB will not need to tighten monetary policy any further, thanks to a disinflation trend that should provide reassurance. This should also act as a supportive factor for future economic activity.

United States: Services ISM Eases Slightly

In the United States, the ISM survey showed a slight softening, delivering a more moderate signal than the S&P survey. Nevertheless, both surveys indicate that economic activity continues to expand, albeit at a modest pace.

As expected, the survey also confirms a slowdown in price pressures, with the first declines in energy prices beginning to feed through.

We continue to believe that, after proving resilient in the face of the energy shock, the US economy is likely to show greater moderation over the summer, with consumer spending becoming somewhat less robust. Nevertheless, as elsewhere, we expect activity to accelerate somewhat from the autumn onward, still supported by investment, particularly in the development of AI.

A potential headwind to growth could come from monetary policy. However, we believe that the Federal Reserve will not go beyond one additional increase in its policy rates toward the end of the year in order to accelerate the convergence of inflation toward its 2% target.

Sebastian Paris Horvitz

Director of Research