In Search of a Way Out of the Crisis in Iran

Link

What are the key takeaways from the market news on April 14, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► Following the failure of negotiations between the United States and Iran, dialogue remains at a deadlock. Instead, in response to the Iranian authorities’ refusal to allow free maritime passage through the Strait of Hormuz, Donald Trump ordered a military blockade of the strait, with the aim of curtailing, in particular, Iran’s oil exports and thereby cutting off a vital source of revenue for the country.

►This strategy of attrition, even if it could be implemented in practice, does not appear truly viable in the medium term, given the potentially very high costs it would entail. Indeed, we believe—like the market—that a resolution of this crisis, involving concessions on both the Iranian and American sides, remains the most likely scenario. Thus, even though oil prices remain very high, they have fallen back below $100 per barrel (Brent) after having surged sharply following the announcement of the U.S. blockade. Obviously, any further escalation of tensions would once again increase the likelihood of the most negative scenarios for the global economy and financial markets.

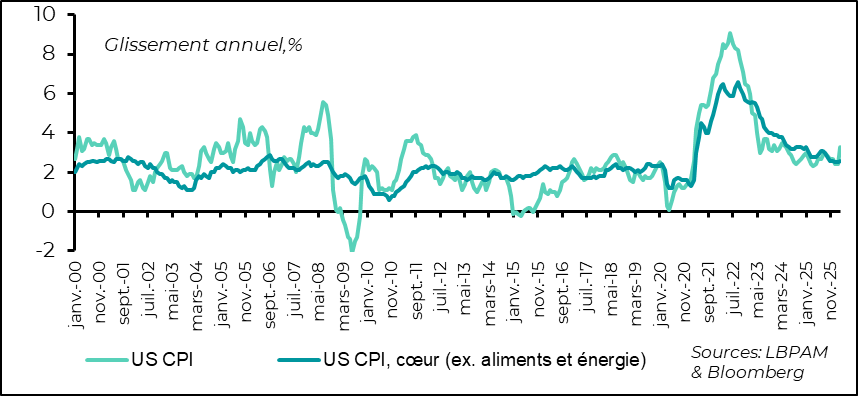

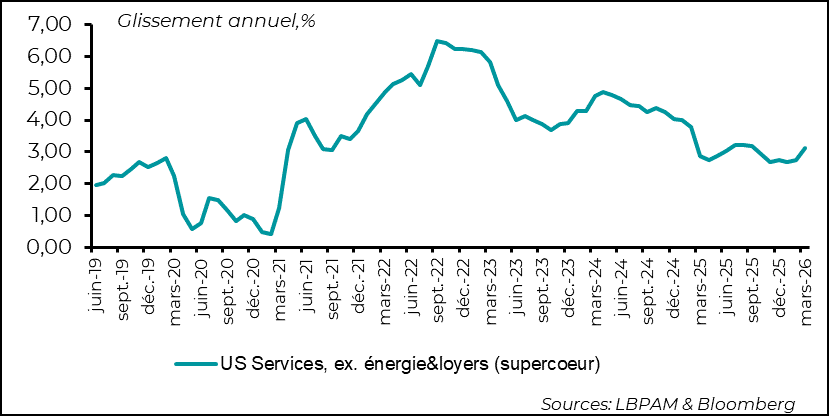

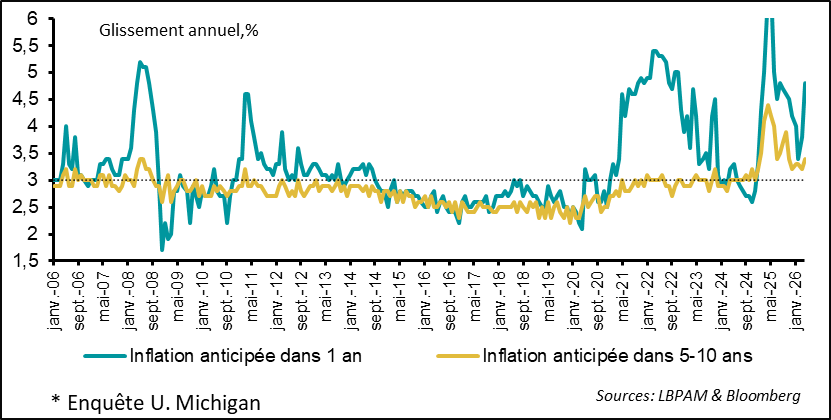

►President Trump continues to downplay the economic impact of this crisis. Nevertheless, its effects are already clearly visible in consumer prices. Indeed, the sharp rise in energy prices (+21%) led to a marked acceleration in inflation in March, reaching 3.3% year-on-year—its highest level since April 2024. At the same time, core inflation increased much more moderately, to 2.6%. However, it should be noted that so-called ‘super-core’ services prices, excluding energy and rents and often highlighted by Federal Reserve Chair Jerome Powell, are once again accelerating. This trend should reinforce the Federal Reserve’s decision to maintain a wait-and-see stance on monetary policy.

►At the same time, the University of Michigan released its preliminary April consumer sentiment survey, which fell to its lowest level since the late 1970s. The political divide remains very pronounced in this survey, with Republican-leaning respondents remaining broadly optimistic.

►Upcoming consumption data will help determine whether the shocks to household purchasing power will lead to a greater-than-expected moderation in spending, particularly following the relatively weak figures recorded in Q4 2025.

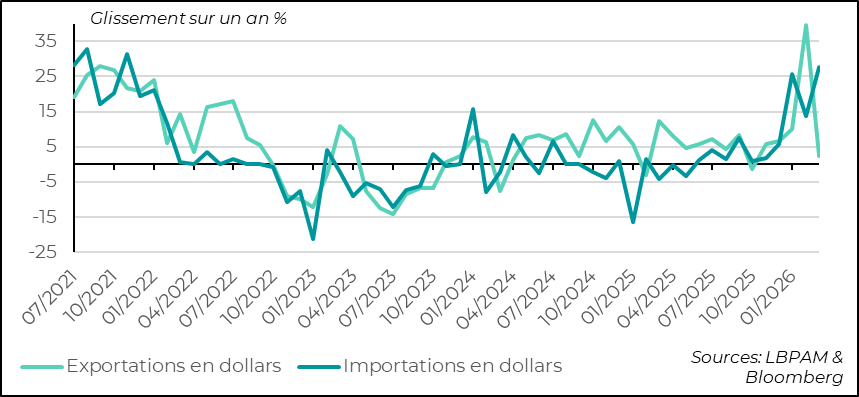

►In China, March foreign trade data show a sharp slowdown in year-on-year export growth in dollar terms, with exports rising by 2.5%, compared with nearly 40% the previous month. However, these figures should be interpreted with caution. On the one hand, they are affected by distortions related to the seasonality of the Lunar New Year, and on the other, by the strong export growth recorded last year, driven by front-loading ahead of the implementation of U.S. tariffs. Moreover, disruptions linked to the closure of certain maritime routes also appear to have contributed to this slowdown. By contrast, imports—particularly of raw materials and especially petroleum products—rose sharply, amplified by significant price effects. Chinese authorities will therefore need to remain vigilant in the face of any lasting deterioration in the country’s export engine.

Going Further

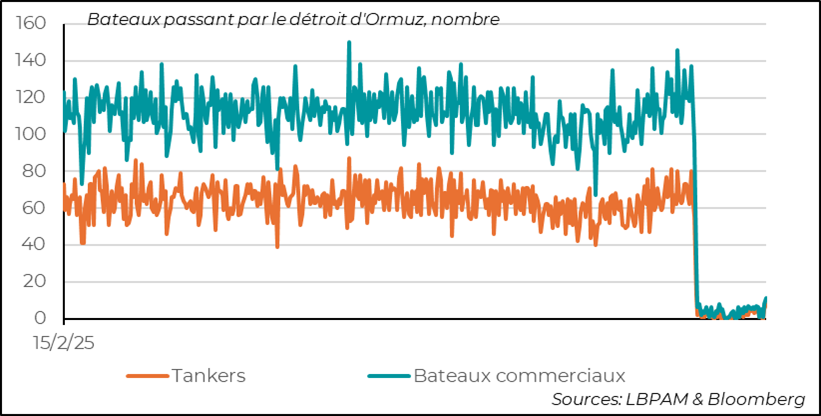

War in the Middle East: The Strait of Hormuz More Closed Than Ever

The Strait of Hormuz was beginning to see a very slight improvement… before the latest escalation

The slight improvement in traffic through the Strait of Hormuz observed during the negotiations between the United States and Iran is likely to fade quickly, in light of the announcement of a tightening of the U.S.blockade of the strait. Clearly, this is bad news for a gradual return to normal flows of oil, gas, and other commodities transiting through this vital maritime route.

Indeed, following the U.S. announcement of a blockade enforced by warships, the price of a barrel of oil quickly rose back above $100. However, this increase proved short-lived, as oil prices soon fell back below the $100 threshold.

This development can be explained, on the one hand, by market expectations—shared by us—that an agreement will ultimately be reached between the two belligerents, as this would serve their mutual interests. This view was reinforced by statements from President Trump suggesting a possible resumption of talks.

A relatively swift reopening of the Strait of Hormuz appears necessary in order to avoid excessively negative effects on the global economy, which is already grappling with very high energy prices and elevated costs for other commodities transported via this strategic maritime route.

At this stage, it is already clear that global growth will bear the scars of this crisis during the first and second quarters. Nevertheless, in order to maintain our central scenario of a gradual normalization of the economic cycle from the summer onward, a rapid and lasting restoration of maritime flows appears essential.

United States: Consumer Confidence at a Low Amid the Energy Shock

U.S. Inflation Accelerates Sharply in March, Rising Back Above 3%

In March, U.S. year-on-year inflation moved back above 3%, driven in particular by a monthly increase of more than 20% in the energy component. This development was widely expected, given the sharp rise in gasoline prices, which climbed back above $4 per gallon—a level not seen since the summer of 2022.

At the same time, no significant spillover to other price components has been observed so far. Core inflation edged up only slightly to 2.6% year-on-year, while its monthly increase remained moderate at 0.2%.

Services Inflation Picks Up Again

Moreover, it is well established that the longer energy price increases persist, the greater the risk of spillover effects to other components of inflation, even though these effects could be partially contained by the negative impact on demand.

That said, it should be emphasized that services inflation—particularly so-called ‘super-core’ services inflation, excluding energy and rents, a measure closely monitored by Federal Reserve Chair Jerome Powell—accelerated again on a year-on-year basis during the month, moving back above 3%. This development provides an additional argument for the Federal Reserve to maintain a cautious stance, and therefore to remain patient in assessing the effects of the energy crisis on the economy.

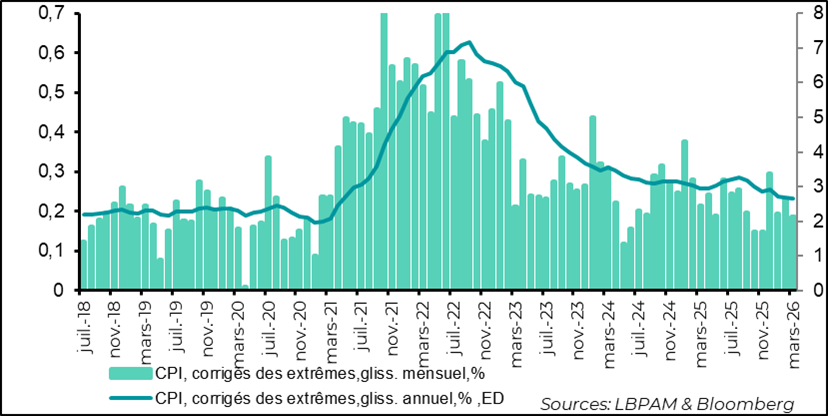

Trend measures remain reassuring

Another measure that has proved useful in the recent period is one that excludes price effects from goods and services displaying atypical behavior. As such, the Cleveland Fed’s indicator, which trims extreme price movements on both the upside and the downside, remained relatively stable in March.

However, once again, it remains premature to draw definitive conclusions about the trajectory of inflation. On a more reassuring note at this stage, medium-term inflation expectations in financial markets remain well anchored.

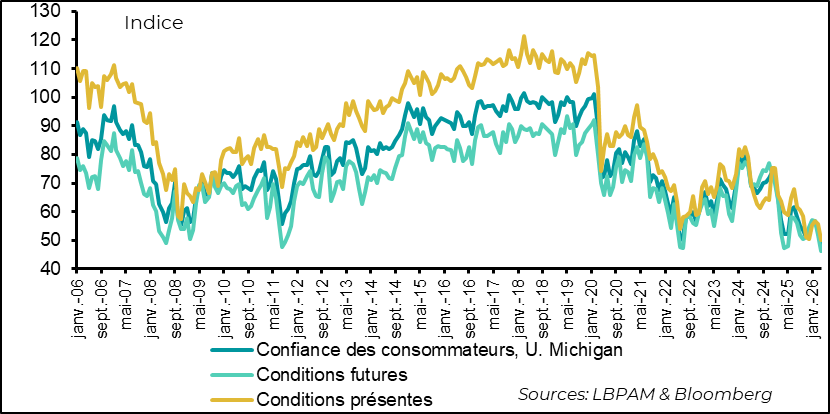

Household Confidence at a Historic Low

What is certain is that the sharp rise in energy prices has significantly dented consumer morale. Indeed, household confidence, as measured by the University of Michigan’s preliminary April survey, has collapsed to reach its lowest level on record.

At the same time, it should be emphasized that the political divide among respondents remains extremely pronounced. While Democrats and independents report very negative perceptions of the economic environment, Republicans, by contrast, continue to express markedly higher levels of confidence.

Rising Inflation Expectations

As we have emphasized, household confidence has been severely affected by rising prices, particularly energy prices. As a result, inflation expectations—both short-term and medium-term—have moved higher again. For the Federal Reserve, this is a key variable to monitor closely. At this stage, however, medium-term inflation concerns remain relatively well contained.

The most noteworthy message from this survey is that Donald Trump and the Republican Party would be wrong to assume that this crisis will have no impact on the midterm elections. In this respect, the survey results suggest that the current situation could weigh on the political climate. As such, this signal should encourage U.S. authorities to seek a swift exit from the ongoing military conflict.

Chine : Les exportations chinoises décélèrent fortement en mars

Export Slowdown and Rising Imports

Chinese exports slowed sharply in March, rising by 2.5% year-on-year in dollar terms, compared with nearly 40% the previous month. One might be tempted to attribute this loss of momentum to the blockade of the Strait of Hormuz. While the closure of this maritime route likely had some impact, the bulk of the slowdown can be explained by other factors: on the one hand, a seasonal effect linked to a later Lunar New Year, and above all an unfavorable base effect following the very strong increase in exports recorded last year in anticipation of higher U.S. tariffs.

At the same time, and largely due to the wartime context, imports rose sharply year-on-year in dollar terms, reaching nearly 28%, compared with just under 14% the previous month. This increase was mainly driven by a marked rise in imports of raw materials—particularly energy—combined with significant price effects. In addition, imports of technology goods also increased, once again amplified by price pressures.

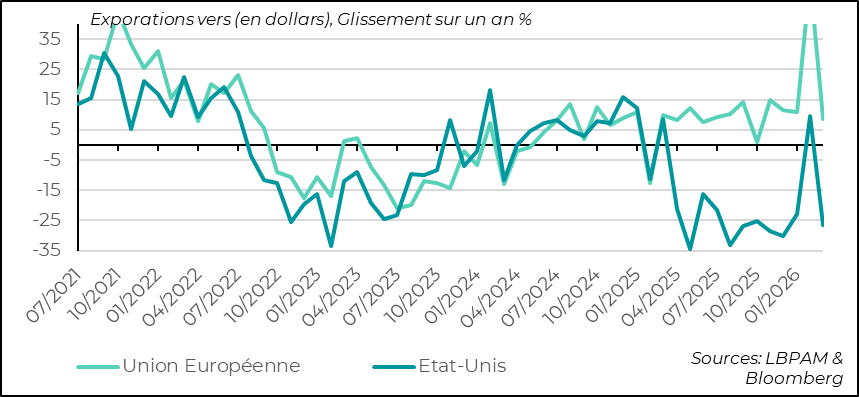

The slowdown in exports is pronounced both toward the United States and Europe

Unsurprisingly, given base effects, the growth of Chinese exports to the United States slowed sharply in March compared with a year earlier. Nevertheless, shipments to the European Union also decelerated significantly, which may partly reflect the effects of the current crisis.

Chinese authorities will need to monitor these trade flows very closely, as the country’s growth model remains highly dependent on the strength of its export engine.

Sebastian Paris Horvitz

Director of Research