In the United Kingdom, Starmer decides to step aside

Link

What are the key takeaways from the market news on June 23, 2026? Sebastian Paris Horvitz provides some insights.

Overview

►After the signing of the memorandum of understanding between the United States and Iran, the start of negotiations to finalize the peace treaty was chaotic. Indeed, the continuation of mutual attacks between Israel and Hezbollah in Lebanon led to the withdrawal of the Iranian authorities from the talks and their threat to close the Strait of Hormuz.

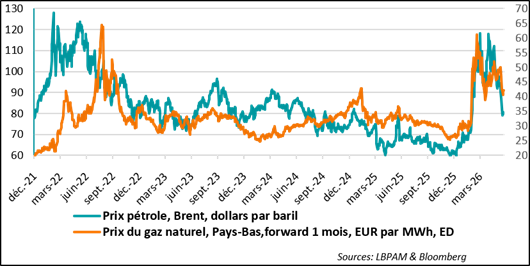

►However, after yet another intervention by D. Trump with Israel, the discussions, which are taking place in Geneva, were able to resume, and the Strait of Hormuz continued to reopen. After some fluctuations, the price of a barrel of oil (Brent) resumed its downward trend, remaining well below 80 dollars.

►Despite potential “incidents,” it seems to us that a path toward an agreement will be found. Indeed, as has been said many times, both countries need to emerge from this crisis. We therefore maintain a scenario of a resolution of the crisis, which should be favorable for markets.

►In the United Kingdom, K. Starmer, the current Prime Minister and leader of the Labour Party, has finally thrown in the towel, announcing that he would step aside. It appears that Labour members of Parliament made it clear to him that he would not have their confidence in the event of a leadership challenge, which was expected to take place in the coming month.

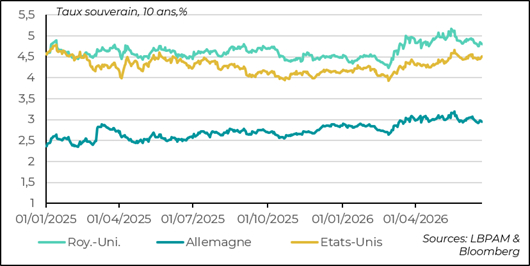

►The most likely outcome is that A. Burnham is expected to take his place, following his election to Parliament last weekend. The transfer of power should take place by early September, when Parliament resumes its sessions. The reaction of the bond market has been almost non-existent, with investors focusing instead on the decline in oil prices.

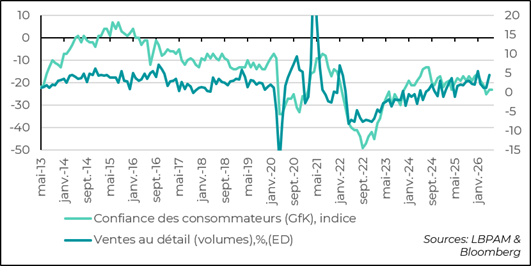

►We will see whether A. Burnham succeeds in restoring confidence while maintaining a disciplined fiscal policy, as he has pledged. In the latest GfK survey on consumer confidence for the month of June, it remains stable, but still, along with March 2025, at its lowest level since Labour came to power.

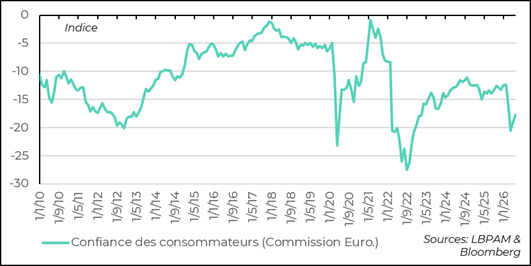

►While the eurozone economy remains depressed, it is interesting to note from the European Commission’s preliminary survey on consumer confidence for the month of June that it continues to rebound, albeit from the extremely low level reached last April (the lowest since December 2022). One can expect this rebound to continue as the energy shock gradually eases following the decline in prices, even if gas prices may fall more slowly.

Going Further

Opening of Hormuz: setbacks, but it continues

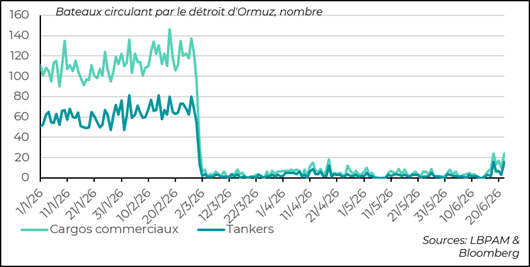

Early signs of an opening of the Strait of Hormuz

Despite a difficult start, the negotiations between the United States and Iran, which took place in Geneva, seem to have made progress on the points outlined in the memorandum of understanding signed a few days ago. While the announcements made by both countries do not always appear aligned, it does seem that progress has been achieved regarding the supervision of Iran’s nuclear program by UN experts, while the United States is said to have committed to returning a large portion of the assets that had been confiscated.

The chief Iranian negotiator reportedly indicated that 12 billion dollars would be returned.

Negotiations are expected to continue soon, with a committee made up of high-ranking members of both countries’ administrations.

Despite continued verbal attacks by D. Trump against Iranian leaders, as well as certain maximalist proposals that appear to have been put forward by the United States — including one from President Trump’s son-in-law, which aimed to require that the returned funds be used exclusively to purchase American food products — and which could derail these talks, it does seem that an agreement is being reached that should bring at least temporary calm to the region.

According to statements by Omani officials, there would also be no “toll” imposed on the Strait of Hormuz.

Overall, shipping traffic has indeed resumed in the strait, albeit very slowly, according to the available data.

Oil and gas prices continue to decline

In this context, it can be observed that oil and gas prices continue to decline. The price of a barrel of oil (Brent) is now well below 80 dollars. As for gas prices in Europe, the decline has been somewhat slower. The heatwave affecting part of Europe, which is pushing energy demand higher, may be contributing to slowing the adjustment in prices. As a result, the price per MWh remains nearly 50% above the level seen at the beginning of the year, although it is about 30% below the levels recorded in March.

A rapid decline in oil prices appears very likely, but the decrease in gas prices may prove to be slower. This dynamic is particularly important to monitor in order to assess how quickly the energy shock is dissipating. The faster the dissipation, the stronger the rebound in the global economy is likely to be, especially as central banks could then adopt a less restrictive stance.

United Kingdom: seeking to reassure in order to revive the economy

Consumer confidence stabilizes in May

Following the uncertainty surrounding K. Starmer’s future, one can expect that the arrival of a new Prime Minister will bring greater stability. Indeed, after K. Starmer’s decision to resign, A. Burnham’s arrival is expected to help restore stability. One of the key conditions for rebuilding confidence will be maintaining fiscal discipline, something A. Burnham has pledged to do.

In this context, it is reassuring to see that the latest consumer confidence survey for the month of June shows stability, following last month’s rebound. Nevertheless, it remains at a very low level.

However, this rebound in confidence goes hand in hand with a slight recovery in consumption, as retail sales (in volume) for May came in stronger than expected, even though, on a year-on-year basis, they were supported by favorable base effects.

Interest rates remain high

It is well known that, beyond inflation dynamics, the fragility of the fiscal situation has been a major factor weighing on the level of interest rates. Overall, despite similar levels of inflation, long-term interest rates still carry a significant premium compared to the eurozone and the United States (despite much higher inflation in the latter).

Thus, if the new UK government, which will be established in September, manages to reassure markets about the fiscal trajectory, while the Bank of England adjusts its policy gradually, as we expect, we could see a decline in long-term yields, providing additional support to the UK economy.

At this stage, however, such a scenario remains somewhat fragile.

Eurozone: towards a rebound in confidence

Rebound in confidence in June after being heavily affected since March

As is well known, growth dynamics have been heavily affected by the energy crisis triggered by the conflict in the Middle East. Not only has the sharp increase in energy prices eroded purchasing power, but the impact on business and household confidence has also been very pronounced. In this context, it is reassuring to see that the European Commission’s preliminary survey on consumer confidence for the month of June shows that, on the household side, confidence has continued its rebound, which began in the previous month.

Given weak demand, this rebound is welcome and supports our scenario of an economic recovery starting in the autumn. However, the energy price shock still needs to dissipate, and for now this may prove somewhat slower in Europe, particularly due to gas prices. A rapid reopening of the Strait of Hormuz should help to gradually ease the shock.

Above all, a faster deceleration in energy prices would help the ECB avoid overreacting and prevent it from adopting an overly restrictive policy that could weigh on the region’s economic recovery in the months ahead.

Sebastian Paris Horvitz

Director of Research