Markets Are Already Pricing in an Extended Ceasefire and the Reopening of Hormuz

Link

What should we take away from market developments on April 17, 2026?

Insights from Xavier Chapard.

Overview

► The ceasefire in Iran continues to hold, and a ten‑day ceasefire begins today in Lebanon. At the same time, however, the US blockade of Iranian ports is fueling tensions, while opposing positions over control of the Strait of Hormuz and Iran’s nuclear program continue to hamper progress in negotiations.

►Markets are nevertheless focused on ongoing talks to extend the ceasefire beyond next Tuesday. Such an extension could become permanent and could happen “very soon,” according to Donald Trump. Global equities, led by the United States, have already surpassed their pre‑war levels, while the VIX index (implied volatility of US equity markets) has fallen back below its pre‑war level, to around 18%. By contrast, the rebound in bond markets has been more limited, as investors continue to price in higher inflation expectations and policy rates than before the conflict.

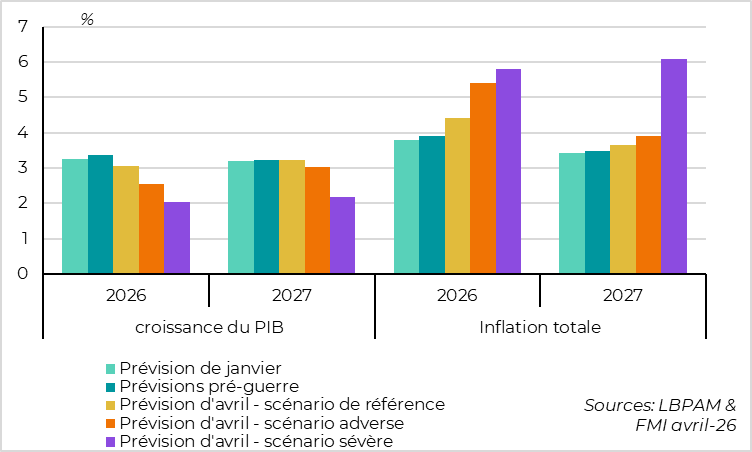

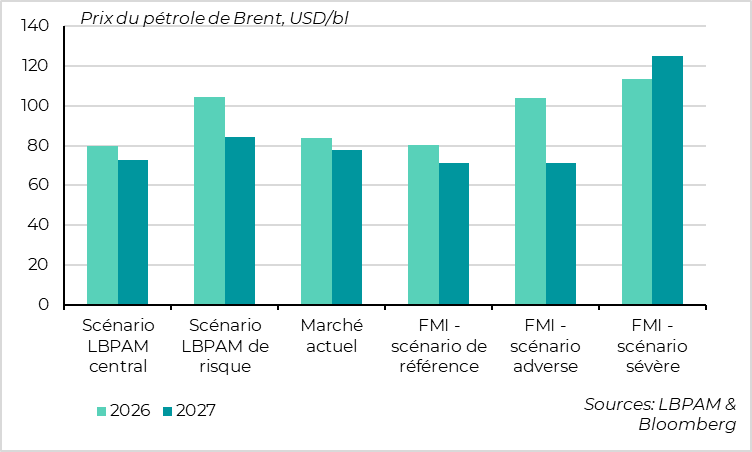

►In line with our own assessment, the IMF has only marginally revised down its global growth forecast for this year (–0.2pp), allowing global growth to remain above 3%. This “central” scenario is based on the assumption of a relatively contained energy shock, similar to ours. The IMF nevertheless remains cautious about the risk of a larger and more persistent shock, and presents more adverse alternative scenarios under which global growth would fall close to recessionary territory should average oil prices exceed USD 100 per barrel over the next two years.

► This framework is consistent with our central scenario, which assumes a gradual de‑escalation starting in April, allowing for a relatively rapid—albeit incomplete—decline in energy prices by the summer. In this environment, the global cycle would be preserved despite a slowdown expected around mid‑year, particularly in Asia ex‑China and in Europe. That said, we still believe the risks surrounding a more negative outcome remain significant (around 30%, down from 35% prior to the ceasefire). Beyond the absence of a lasting agreement between the United States and Iran, the main risks stem from a potential resumption of hostilities and, above all, from oil and gas flows through the Strait of Hormuz remaining severely constrained beyond April. Such a scenario would begin to directly impact the real economy through shortages and could reverse the normalization in business sentiment, thereby threatening the global cycle.

► Against this backdrop, the market rebound appears justified, even though it has been faster and stronger than we initially expected. This reduces near‑term upside potential but does not preclude a continuation of the rally over the medium term. This is all the more so as the recovery in corporate earnings appears to be confirmed at the start of the first‑quarter reporting season. That said, greater caution seems warranted in the short term, given the still‑meaningful probability of adverse news that is no longer priced into risky assets.

►From a macroeconomic perspective, Chinese growth surprised on the upside in the first quarter, re‑accelerating from 4.5% to 5.0%. This performance nevertheless remains highly unbalanced, with growth once again driven by industrial production and exports, while consumption and private investment remain weak. A positive development is the gradual exit from deflation after three years of falling prices. We believe that, with continued targeted policy support, China should reach the midpoint of its annual growth target (4.5–5.0%) this year, even though longer‑term prospects remain challenging. In an unsettled global environment, China therefore represents a relative source of stability.

► In the United States, recent data have been reassuring, even as the economy had shown some loss of momentum ahead of the conflict. Initial jobless claims remain very low in early April, suggesting that the labor market remains solid. In addition, the first regional Fed surveys for April do not yet point to any meaningful slowdown in activity.

► In Europe, euro‑area inflation for March was revised slightly higher, to 2.6% from 2.5% previously. This revision reflects solely stronger gasoline prices, while the deceleration in core inflation (2.3%) and services inflation (3.2%) remains intact. This development should not alter the ECB’s assessment, especially as a growing number of Governing Council members are signaling that a rate hike as early as April would likely be premature. We therefore continue to expect a single ECB rate hike in June, even as markets still price in two.

► Finally, in the United Kingdom, monthly GDP rose by 0.5% in February following a 0.1% increase in January, confirming that the economy had started to recover after stagnating in the second half of last year. This rebound, however, predates the energy shock, which is expected to weigh more heavily on the UK economy than on other major advanced economies. In this context, we continue to believe that the Bank of England will keep rates unchanged this year: while inflation should remain above target, economic growth is likely to run below potential after the first‑quarter rebound.

Going Further

China: Resilient growth, but increasingly unbalanced

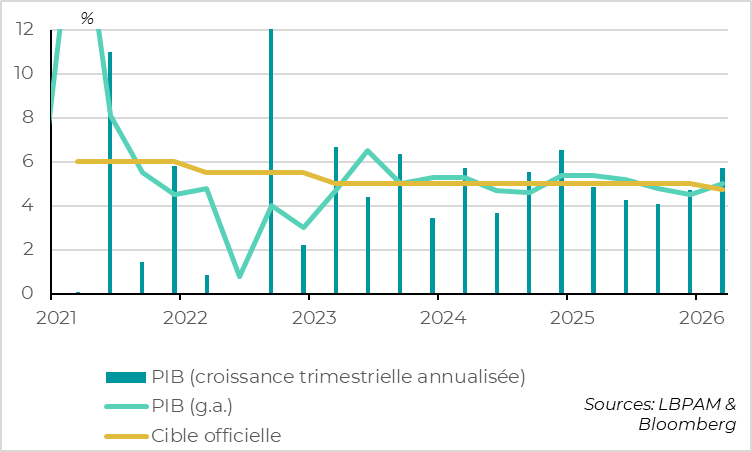

Chinese growth rebounds to 5% in Q1 2026

Chinese growth re‑accelerated from 4.5% to 5.0% year‑on‑year in the first quarter of 2026, driven by a strong rebound in sequential growth, close to 6% at the start of the year. This outcome is reassuring after the sharp slowdown observed at the end of 2025 and came in slightly above market expectations (consensus was 4.8%).

At the same time, prices embedded in GDP have stabilized for the first time in three years. The GDP deflator stood at –0.1% year‑on‑year, its least negative reading since mid‑2023. The move of producer prices into positive territory in March, driven by higher commodity prices, together with the deceleration in property price declines, should allow the GDP deflator to exit deflation as early as this quarter.

The solid Q1 growth performance strengthens policymakers’ confidence in their ability to achieve the annual growth target of 4.5–5.0%. Combined with the reduced risk of deflation, this lowers the urgency for broad‑based stimulus measures despite the energy shock. Moreover, the direct impact of the energy shock on the Chinese economy should remain limited, given a favorable energy mix, substantial oil and gas inventories built up over recent years, and domestic price controls. By contrast, China remains highly exposed to a slowdown in external demand, which would represent an important indirect transmission channel should the energy shock prove larger and more persistent than expected..

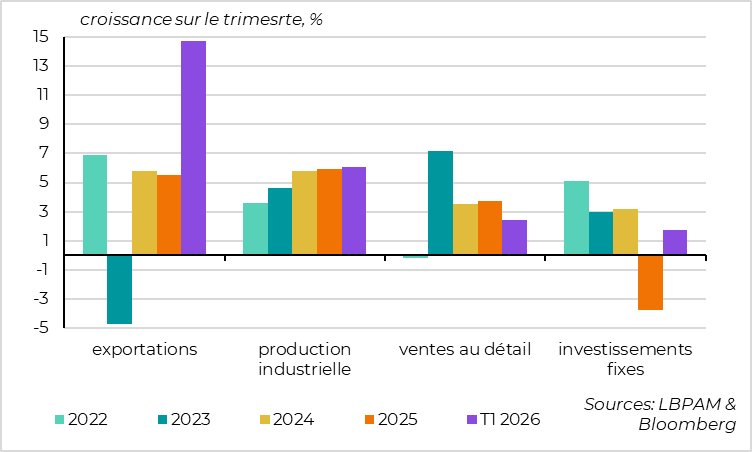

Growth still driven primarily by industry and exports

Despite the strong headline growth figure, the composition of China’s growth is even more unbalanced than in the past two years.

Industrial production accelerated slightly in the first quarter and continues to outperform the services sector, growing by 6.1% after 5.9% in 2025. This strength is largely driven by a sharp rise in exports, which increased by 14.7% year‑on‑year in USD terms, compared with 5.5% growth in 2025. Imports also rose markedly (+23% after stagnating for two years), but this reflects mainly higher commodity prices rather than higher import volumes, limiting their contribution to real growth.

By contrast, private domestic demand remains weak. Retail sales continued to decelerate, rising only 2.4% in Q1 after 3.7% in 2025. While retail sales capture only part of consumption, they suggest that consumer demand remains subdued. Investment spending returned to positive growth after last year’s historic decline (+1.7% in Q1 after –3.7%), but remains very modest and was driven early in the year by a rebound in public infrastructure investment (+9%). Private investment remains depressed, even if conditions have improved slightly relative to 2025: manufacturing investment rose by 4.1%, while real estate investment continued its sharp decline (–11.2%).

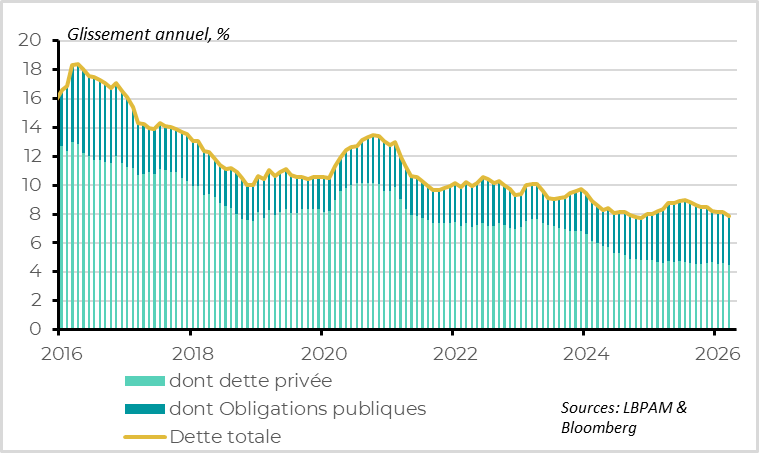

The slowdown in credit growth in March points to softer activity ahead

As for the near‑term outlook, we attach limited importance to signs of activity slowing at the end of the quarter in the March data, following a strong acceleration in January and February. These developments largely reflect calendar effects related to the Lunar New Year holidays. An unusually high number of working days in February and fewer in March likely explain the sharp deceleration in production, and even more so in retail sales and exports, in March.

By contrast, credit data send a more concerning signal for the months ahead. Credit growth to the economy continued to slow and fell below 8% for the first time since 2024. This deceleration reflects both weaker issuance of local government bonds—negative for infrastructure investment—and a continued slowdown in bank lending to households and corporates, weighing directly on private demand.

In this environment, external demand and targeted policy support remain critical to limiting the slowdown in activity around mid‑2026 and enabling the Chinese economy to reach the midpoint of its annual growth target of 4.5–5.0%, which remains our central scenario.

Market pricing is converging back toward our central scenario

That said, this ceasefire—even if fragile—and the start of negotiations—even if complex—remain very positive developments for both the economy and financial markets.

They demonstrate that both sides have an interest in halting escalation, thereby reducing the risk of extremely negative scenarios for the global economy. It has also become clear that several countries beyond the direct belligerents are involved in the process—notably China, alongside Pakistan, Turkey and Egypt—which adds credibility to the negotiation framework. This has significantly reinforced the so‑called “TACO” effect, meaning that markets should become somewhat less sensitive to belligerent statements from the US administration. This is positive in itself, as it lowers the risk of an abrupt tightening in financial conditions that would amplify the economic impact of the energy shock.

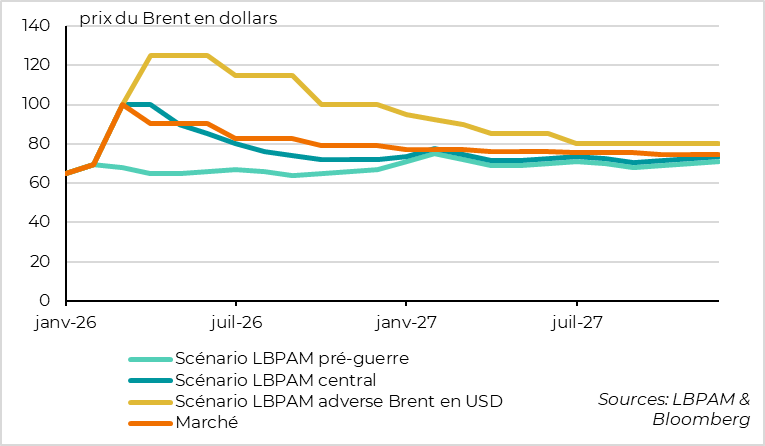

Overall, energy markets have moved back toward a scenario close to our central case, having been approaching our adverse scenario prior to the ceasefire announcement.

Under these conditions, the market rebound appears reasonable so far, particularly as it has been supported by increasingly defensive investor positioning. We remain broadly constructive on risky assets over the medium term, although gains are likely to be more gradual and more uncertain than the sharp rebound observed this week.

On rates, markets have removed only one expected rate hike for both the ECB and the BoE, and therefore continue to price more tightening than we foresee. We thus remain positive on sovereign bonds, especially at the short end of the curve

Global Outlook: The IMF, Like Us, Is Constructive but Cautious

A supportive central scenario, but markedly weaker alternative outcomes

The IMF released its semi‑annual update of global economic forecasts this week. It points to a downward revision of global growth for this year by 0.2 percentage points, although growth would still remain slightly above 3%.

The report notes, however, that economic data from late 2025 and early 2026 would have justified an upward revision of 0.1 percentage point in the absence of the conflict. In other words, the war and the associated energy shock incorporated by the IMF imply a total downward revision of 0.3 percentage points to global growth. Overall, this adjustment remains limited given the scale of the geopolitical and energy shock that emerged in March, and is broadly consistent with the revisions we have implemented since late February.

Everything hinges on the magnitude and duration of the energy shock

The IMF’s relatively modest revisions are based on a scenario in which the oil shock is assumed to be contained in both duration and intensity, broadly in line with our central scenario. Like us, the IMF expects average oil prices slightly above USD 80 per barrel this year, with European LNG prices around EUR 42.5/MWh. This implies a fairly rapid and significant—although incomplete—decline in energy prices starting in the second quarter. Under this assumption, growth and inflation would be temporarily affected around mid‑year, but the global expansion cycle would remain intact.

That said, the IMF adopts a decidedly cautious stance, referring to its central case as a “reference scenario” rather than a “baseline,” and presenting a range of more adverse alternative scenarios. In scenarios where average oil prices rise above USD 100 per barrel this year (with gas prices around EUR 75/MWh), global growth would be reduced by around 1 percentage point. Global growth would then slow toward 2%, a level historically associated with a high risk of global recession.

This approach is consistent with our own assessment, which still assigns a relatively high probability—around 30%—to a downside scenario in which oil prices exceed USD 125 per barrel in the coming weeks and average above USD 100 over the year. In such a scenario, the most exposed regions—particularly Asia ex‑China and Europe—could enter recession around mid‑year, followed by a slow and fragile recovery.

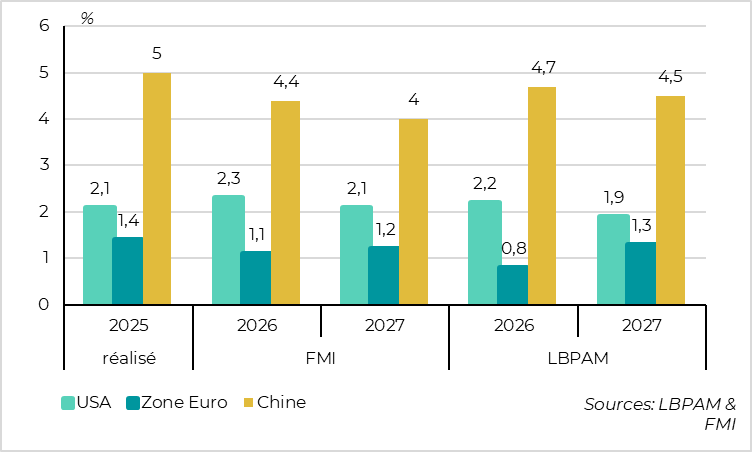

More optimism on the euro area, but a more conservative stance on China

At the regional level, the IMF’s revisions appear more limited than ours for Europe in the near term, somewhat more optimistic for the United States at the 2027 horizon, and clearly more conservative for China. This divergence in assessment is one of the key factors underpinning our continued overweight position in Chinese assets and our decision to no longer overweight European equities relative to US equities.

Xavier Chapard

Strategist