One step forward, then two steps back

Link

What are the key takeaways from the market news on April 16, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► After the enormous relief brought by the announcement of a ceasefire between Iranians and Americans on April 8, this past weekend the prospect of a more lasting agreement seemed to fall apart. Indeed, after the Iranian authorities announced that the Strait of Hormuz had been reopened, the United States refused to lift the military blockade they had put in place. This triggered a cascade of events resembling a renewed escalation. Iranian authorities first reinstated their blockade and fired on two vessels attempting to make the crossing. For their part, the Americans seized an Iranian vessel, and President Trump issued a series of highly belligerent statements against Iran.

►Obviously, these events once again caused oil prices to surge. After reaching a one-month low of USD 87 per barrel (Brent), the price rose back above USD 95 yesterday. Beyond the negative signal that such a high price sends for the global economy, fears of a return to war have resurfaced, notably following remarks by D. Trump, who said he was ready to destroy Iran’s electricity generation infrastructure and all of its bridges, as he had already announced at the time of the ceasefire.

►Despite the fury, a new opportunity for an extension of the ceasefire, or even for a more lasting agreement, will play out tomorrow. Indeed, after contradictory announcements, there should be a new meeting between Iranian and American delegations in Islamabad. It is worth noting that during the previous round of negotiations, despite its failure, a ceasefire was nonetheless achieved. This time, the stakes are certainly higher: the challenge is not only to find common ground and restore trust between the two belligerents, but also to reassure economic actors about the possibility of a path toward the normalization of global oil and gas supply, with the reopening of the Strait of Hormuz.

►We continue to believe that, on both sides, the economic and political incentive to end this conflict is considerable. Nevertheless, the latest developments can only be a cause for concern. A continuation of the conflict, with the risk of higher energy prices or even shortages, would have a very negative impact on the global economy. The idea, sometimes put forward, that the United States would be relatively spared by this war is false.

►Our central scenario continues to be based on a rapid end to the conflict and a normalization of the economic cycle. Nevertheless, the outcome of the negotiations, which will take place from tomorrow until Wednesday evening, when the ceasefire expires, is crucial to validate this scenario. A favorable outcome would confirm our rather constructive view on risk assets.

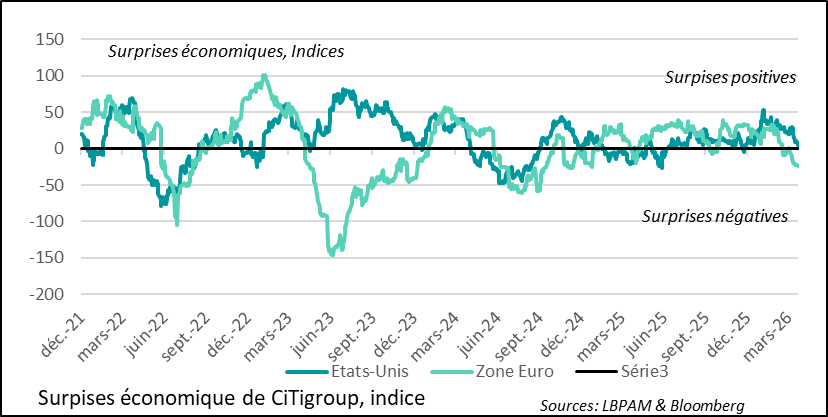

►At this point, this war is already weighing on short-term growth. The latest economic data, on both sides of the Atlantic, show a clear trend toward disappointment relative to expectations. This is currently more the case in the euro area than in the United States. To reverse this trend, economic momentum needs to improve, which will require a reduction in the energy shock and a return of confidence.

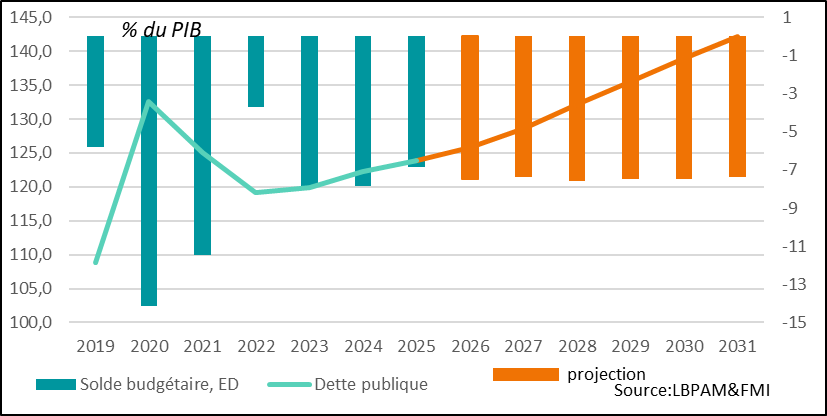

►Similarly, this war will have negative consequences for public finances in many countries that are already facing strained public budget conditions. Indeed, in its latest report, the IMF has urged governments to exercise restraint with regard to potential support measures aimed at cushioning the energy shock. More importantly, the IMF once again emphasized the unsustainable trajectories of public finances in many countries, foremost among them the United States, with public debt expected to exceed 140% of GDP by 2031. In the short term, part of the reduction in the U.S. public deficit achieved last year will be reversed, as the U.S. tax authorities have begun reimbursing USD 166 billion in tariffs that were declared illegal by the Supreme Court last February.

►Today, Kevin Warsh’s confirmation hearing before the Senate will take place, following his nomination by President Trump to take the helm of the Fed next month, when J. Powell’s term as chair comes to an end. The most likely outcome is that he will be confirmed. The main obstacle comes from a Republican senator, T. Tillis, who has already stated that he will not vote in favor of the nomination as long as the legal proceedings against J. Powell, related to the renovation of the Fed’s buildings in Washington, are not dropped. However, for markets, the most important issue will be K. Warsh’s commitment to preserving the independence of the institution. He has always stated that he would adhere to this principle. Nevertheless, in recent years he has been very critical of the Fed, accusing it of overstepping its authority. These comments have always been quite vague and difficult to reconcile with reality. One of his flagship positions is that the Fed should drastically reduce its balance sheet. In the current monetary framework in which the Fed operates, this would be impossible without potentially creating financial tensions that would weaken the U.S. and global economies. That said, it is difficult to see how he could secure the approval of the Board of Governors to pursue such an approach today.

Going Further

Economic outlook: The war in the Middle East continues to weigh on the economic outlook

Economic data tend to fall short of expectations

It is evident that the longer this war drags on, pushing commodity prices higher—first and foremost oil and gas prices—the more the global economic outlook will deteriorate. Indeed, on both sides of the Atlantic, the latest economic indicators are showing significant downside surprises, particularly in the euro area. As a result, the shock has already begun to undermine the favorable momentum we had at the beginning of the year.

Beyond the direct impact of higher costs, confidence is deteriorating and is weighing on the spending intentions of economic agents. In this respect, despite President Trump’s statements downplaying the economic impact of the war, it is clear that the U.S. administration is fully aware of the risks this conflict poses to the U.S. economic outlook.

Moreover, this deterioration in economic momentum will undoubtedly have significant consequences for the midterm elections scheduled for this autumn, weakening the prospects of Republican candidates. This is, in fact, one of the key reasons that should push U.S. authorities toward a resolution of the crisis in the days ahead.

Industrial metal prices at record highs

While economic data appear to be clearly weakening, it is true that markets continue to favor a positive resolution of the crisis. We share this same bias.

This positive view of the future economic outlook, which would support risk-taking, is also reflected in a renewed sharp rise in metal prices, particularly copper. Admittedly, higher energy and transportation costs are contributing to this increase, but it can be argued that one of the key characteristics of the current global cycle—namely, growing needs for electricity generation and therefore for transmission capacity—is pushing copper prices ever higher.

Copper prices have long been a relatively reliable indicator of the economic cycle. This role is likely taking on even greater importance in the race to develop artificial intelligence, which is extremely energy-intensive.

United States: The risk of a continued deterioration in public finances

Continued deterioration of public finances

Amid the noise of the war, the announcement by U.S. authorities that they would begin reimbursing tariff revenues collected illegally, following the Supreme Court’s decision, has largely gone unnoticed. Indeed, the U.S. government is expected to refund USD 166 billion (0.5 percentage points of GDP). However, these reimbursements will be gradual. Only 20% of the companies concerned are expected to be repaid quickly, while the process for the remainder is likely to take longer. In any case, part of the improvement in public finances recorded last year will be wiped out. Some of it will be offset by tariff increases already implemented through a different mechanism, but given recent developments, it is very likely that tariff revenues will prove to be lower than initially expected.

It is also in this context that the IMF, in its report on the state of public finances published last week, once again highlighted the unsustainable fiscal trajectories of certain countries, notably the United States—this despite tariff revenues.

According to the institution, U.S. public debt is expected to exceed 140% of GDP by 2031, with public deficits remaining above 7% of GDP. In light of the current administration’s new demands for increased military spending in particular, it seems clear that the public deficit targets set out by candidate Trump—aiming for 3% of GDP—will be difficult to achieve.

More fundamentally, the risk of a continued increase in the term premium on U.S. government bond yields is rising. Moreover, if the Fed were to move toward a rapid reduction of its balance sheet, as advocated by K. Warsh, the pressures would be even greater.

Sebastian Paris Horvitz

Director of Research