President Xi did not bring any easing of tensions regarding the war

Link

What are the key takeaways from the market news on May 19, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► There was a slight hope that last weekend’s meeting between Presidents Trump and Xi could help pave the way toward a resolution of the conflict between the United States and Iran. Unfortunately, this hope has been disappointed. The Strait of Hormuz remains largely closed, and the price of a barrel of oil is holding around $110. As a result, the oil shock continues to spread throughout the global economy.

►It appears that President Xi prioritized discussions on Taiwan’s future in order to secure a U.S. stance more closely aligned with China’s views. This was partially successful, as President Trump mentioned the need for easing tensions between the island and the mainland and suggested that he opposed Taiwan’s independence from China. The U.S. president’s remarks seem to run counter to the long-standing position of American diplomacy.

►At the same time, the Chinese authorities do not appear to have offered any specific assistance toward a rapid reopening of the Strait of Hormuz. This lack of enthusiasm in helping to persuade their Iranian ally to move toward an agreement seems to illustrate the maxim attributed to Napoleon: “Never interrupt an enemy who is making a mistake.”

►Indeed, in this crisis, the Chinese authorities view the United States as a loser, as it is weakening. However, the economic weakening caused by rising energy costs, along with constraints on production chains, is affecting the entire world. Europe is among the most impacted regions, as reflected in economic data.

►This rise in energy prices appears to be starting to spread to other goods and services, as shown by consumer price index releases in many countries, particularly in the United States. This partly explains the sharp increase in interest rates in recent days. The U.S. 5‑year sovereign yield has risen by nearly 40 basis points (bps) over the past month, while it has increased by more than 20 bps in Germany. This rise is driven both by higher inflation expectations and by an increase in term premiums, in a context of heightened uncertainty regarding the direction of monetary and fiscal policies. At the same time, this increase in yields has dampened risk appetite, leading to a pullback in equity markets.

►As we have already pointed out, the longer this energy shock persists, the more lasting its effects on inflation could be, while also affecting growth prospects. At this stage, despite the lack of progress toward reopening the Strait of Hormuz, we believe that both sides in the conflict are seeking a way out. However, given the current uncertainty, we have decided to significantly and tactically reduce our exposure to risk assets.

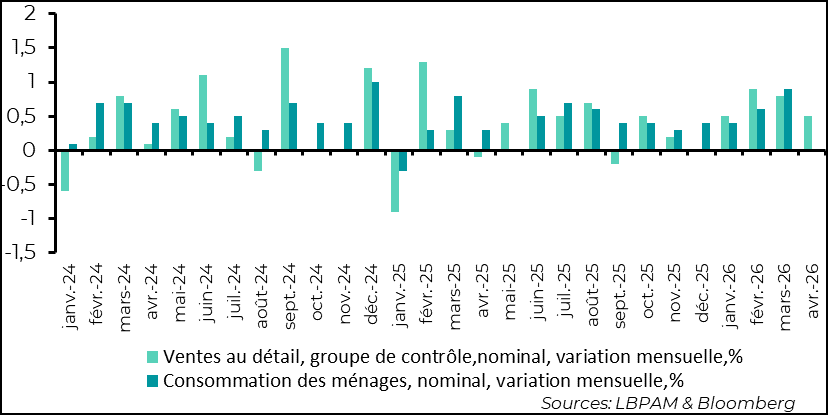

►Moreover, the U.S. economy has proven more resilient than that of most other countries. Business cycle indicators across the Atlantic stand in contrast to those in the euro area, as reflected in the PMI indices. The latest consumption data for April are also solid. Retail sales rose by 0.5% over the month for the so‑called “control group,” used to estimate total consumption. In real terms, the increase is more modest (around 0.1%), but it follows a 0.8% rise in the previous month.

►This dynamic is partly explained by the increase in household income in March and April, linked to tax benefits granted under the budget law (notably the exemption of taxes on tips). However, this effect is expected to fade, reinforcing the negative impact of inflation on purchasing power.

Nevertheless, GDP growth in the second quarter of 2026 is likely to be stronger than expected, especially as investment remains resilient, notably supported by spending related to artificial intelligence.

However, we believe that consumption could weaken further in the third quarter of 2026, particularly as wage growth may slow (after +3.6% year-on-year in April, according to the Atlanta Fed). A labor market that remains strong could support consumption, but also increase inflationary pressures, thereby complicating the conduct of monetary policy.

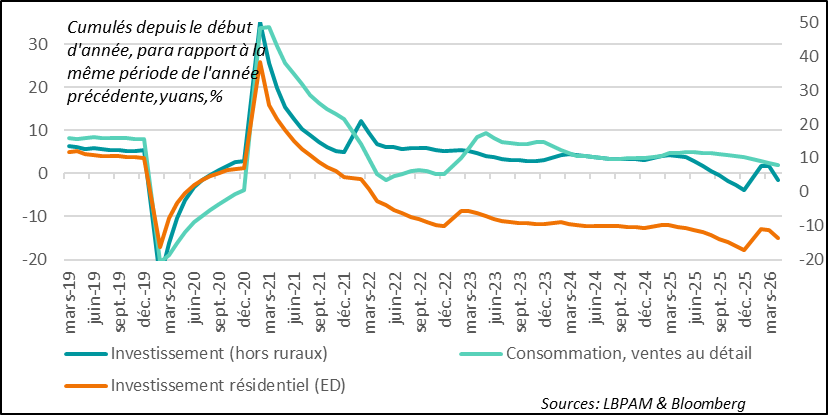

►While the U.S. economic environment remains solid, the latest Chinese data on domestic demand have been disappointing. Retail sales rose by only 0.2% year-on-year in April, signaling a clear slowdown. This is partly explained by the end of government support measures aimed at boosting consumption. In addition, investment surprised significantly on the downside, with a contraction of 1.6% over the first four months of the year compared with the same period last year. Residential investment also deepened its decline over the same period, falling by 13.7%.

This weakness in demand is likely to push the authorities to strengthen support measures in order to meet the GDP growth target (between 4.5% and 5%). Despite their strong performance, exports will not be able to sustain growth on their own.

►Finally, in the United Kingdom, the political outlook for Prime Minister K. Starmer has deteriorated. By the summer, it is likely that a rival within his party will attempt to replace him. In this context, the risk is that markets will maintain upward pressure on long-term UK yields as long as a credible path for restoring public finances is not presented by the authorities.

Going Further

Iran war: pressure on interest rates has suddenly intensified

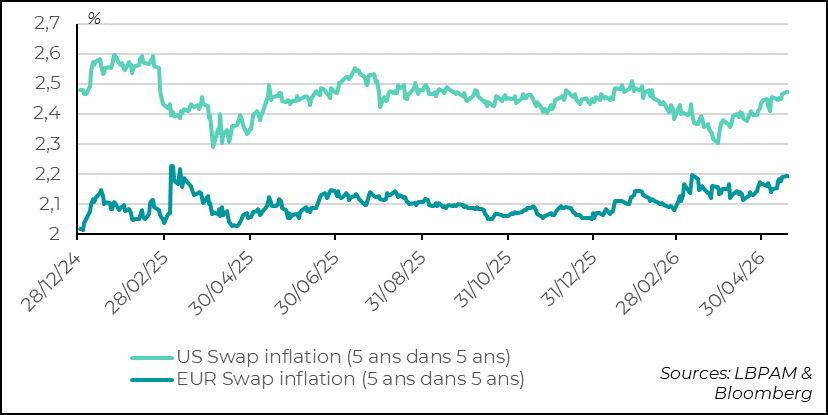

The rebound in inflation is fueling a rise in expectations

The persistence of the oil shock, linked to the deadlock over reopening the Strait of Hormuz, is maintaining upward pressure on energy prices, which is beginning to spread more broadly to overall prices. Nevertheless, at this stage, this pressure remains relatively contained. This concern about a lasting inflationary shock is now clearly visible in market expectations. Indeed, since the ceasefire agreement reached in early April, expectations have continued to trend upward on both sides of the Atlantic. In the United States, they have risen by more than 10 basis points, while the increase has been slightly more modest in the euro area.

Overall, the trend remains upward and is reflected in expectations of a tightening of monetary policies over the coming quarters.

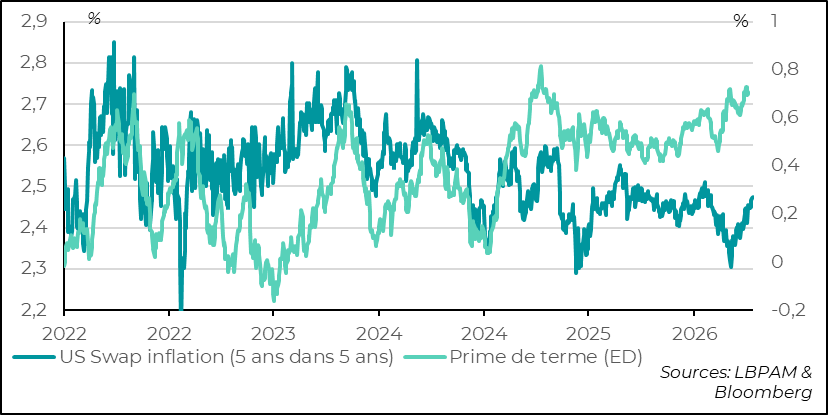

Uncertainty is driving the increase in term premiums

The surge in inflation has been a key driver behind the rise in interest rates, but it has also been accompanied by increased uncertainty regarding the future path of monetary and fiscal policies. As a result, the term premium on 10-year yields, as estimated by the Fed, has risen significantly over the period.

In the United States, interest rates are now close to the levels seen at the beginning of the Trump administration, with the 10-year yield exceeding 4.6%. In the euro area, this shock has also led to a sharp rise in yields, with the German 10-year rate surpassing the highs reached in 2023, at 4.15%.

This increase in interest rates is clearly not supportive of growth and acts as a headwind for risk assets. After the strong rebound in equity markets in April, this rise in yields reinforces the cautious stance we have adopted toward risk assets. Greater visibility on the normalization of energy trade, in particular, is needed before we can return to a more constructive positioning.

United States: consumption remains strong

The American consumer continues to support growth

Retail sales data in the United States for April came in significantly stronger than expected. Indeed, they rose by 0.5% over the month when considering the so‑called “control group,” which is used to estimate consumption in GDP. Notably, this increase follows the strong rebound in the previous month, when spending had risen by 0.8%.

In real terms, the April increase is much more modest (around 0.1%) than in the previous month, but it remains noteworthy given the acceleration in inflation over the period.

This solid performance in household spending can partly be explained by the rise in income over the past two months, notably linked to tax refunds for certain households, as предусмотрed in the budget law adopted last year, particularly the removal of taxes on tips.

However, this effect is expected to fade in the coming months, and it is likely that the negative impact of inflation on purchasing power will somewhat weaken consumption dynamics.

At the same time, the recent strength of the labor market, along with favorable indicators from unemployment benefit claims, which remain relatively stable, suggests that consumption should continue to hold up, even as wage growth seems to be slowing, as indicated by the Atlanta Fed’s estimates showing a 3.6% year‑on‑year increase in wages in April.

Stronger‑than‑expected resilience in consumption, particularly if supported by a solid labor market, could lead the Fed to exercise greater caution in the conduct of monetary policy. In this context, K. Warsh, who will become the new Fed Chair this month, may face difficulties convincing his colleagues to cut policy rates, as he had initially intended.

China: domestic demand is weakening

Domestic demand disappoints in April

After a relatively robust start to the year, the latest figures on China’s domestic demand have been fairly disappointing. Indeed, all components of demand came in well below expectations.

Consumption, measured by retail sales, slowed significantly. Its growth stands at 1.9% since the beginning of the year compared with the same period last year, marking a clear decline from the 2.4% recorded in March. This deceleration partly reflects the end of government support measures aimed at boosting purchases of cars and household equipment.

On the investment side, the data were also disappointing. Since the beginning of the year, investment has contracted by 1.6% compared with last year, following a 1.7% increase the previous month. This development reflects a degree of wait‑and‑see behavior among companies, linked to the lack of momentum in the domestic economy, as well as the continued downturn in the construction sector. Real estate investment has thus fallen by 13.7% since the start of the year compared with the same period last year.

These results are likely to prompt the authorities to maintain their targeted support policies in order to achieve their GDP growth target, set between 4.5% and 5% for the year. Indeed, despite the recent strength in exports and a relative easing in trade tensions with the United States, the external sector will not be able to support the Chinese economy on its own.

Sebastian Paris Horvitz

Director of Research