Relief: reopening of the Strait of Hormuz

Link

What are the key takeaways from the market news on June 16, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► On Sunday, President Trump announced that an agreement had been reached with Iran. This announcement was confirmed by the Iranian authorities. However, for now, no details are available. Nevertheless, what the American president emphasized is that the Strait of Hormuz will reopen by Friday.

►This reopening would take place, as has been mentioned several times in the past, as part of a 60-day extension of the current ceasefire. During this period, the issues that appeared to be the main causes of the conflict will be discussed, including Iran’s nuclear program.

►This discussion framework obviously appears fragile, given the lack of agreement during the talks over the past two months. However, we continue to believe, along with a large share of the market today, that the incentives on both sides to bring this conflict to an end are so strong that a return to war seems unlikely, although not impossible.

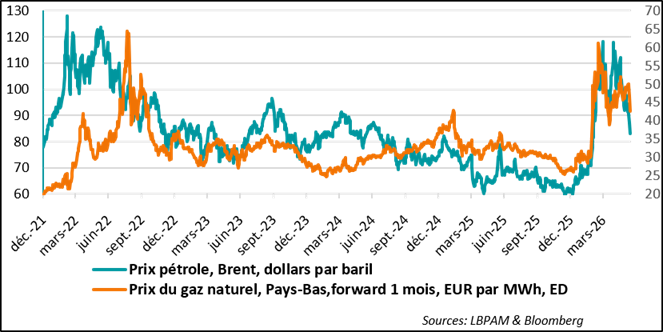

►We expected the reopening of Hormuz to occur earlier, but the most important thing is that it is now happening. The oil and gas markets, in particular, will be able to normalize gradually. The sharp drop in the price of a barrel of oil (Brent), which fell below 84 dollars yesterday (compared to 107 at the beginning of May), reflects a certain degree of market optimism, but it appears justified to us.

►We expected a slower decline in oil prices, but we maintain our projection of a convergence toward 70–75 dollars by mid-2027. This development is clearly very favorable for the global economy. It should help to ease, or even dissipate, the inflationary shock. This would provide momentum to growth and support demand, while fiscal support (in the United States, Germany, and Japan, in particular) should remain supportive.

►The euro area, in this scenario, should be a major beneficiary, after having been more severely affected by the energy shock.

►At the same time, the reversal in energy prices should ease central banks’ concerns regarding the inflation outlook. Admittedly, given the duration of the energy shock, there are still risks that it could spread to other prices, which makes central banks’ caution necessary.

►However, with regard to the euro area in particular, given the negative impact on activity, we believe the risks of persistent strong inflationary pressures are limited. This supports our view that the ECB will keep its key interest rates unchanged in the coming months, although the risk of an additional rate hike cannot be completely ruled out.

►We will get this week an updated reading of the current stance of both the BoE and the Fed. For both, we expect a status quo. However, the market will be particularly attentive to the communication of K. Warsh, the new Fed Chair. Given the short-term uncertainties, expectations are for a firm stance on inflation. This would help reassure economic agents about the Fed’s independence, despite calls from D. Trump for the adoption of a more accommodative policy.

►The sharp decline in oil prices driven by the imminent reopening of Hormuz has, unsurprisingly, boosted risk appetite, with the fossil fuel sector, as expected, undergoing an adjustment.

This increased allocation to risky assets has been amplified in the United States and in other markets with a high concentration of technology stocks by the wave of investor enthusiasm following SpaceX’s market debut. As a result, technology stocks, which had been under pressure in May, have recovered a large part of their previous losses.

As for sovereign bonds, yields have declined in response to falling oil prices, which have eased inflation expectations.

►This mix of euphoria around technology, still driven by AI, and relief over the decline in oil prices should continue to support the market’s momentum, but valuations are becoming more stretched and are likely to limit further gains in the indices.

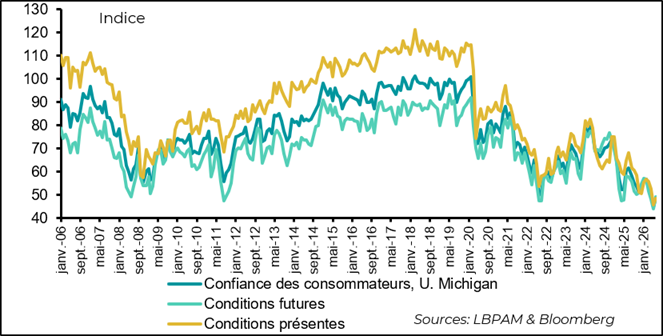

►Moreover, as is well known, economic data in the United States have so far been more favorable than expected. Nevertheless, some indicators continue to show pockets of weakness. The preliminary University of Michigan survey on consumer confidence for early June shows that it remains at a historically low level, even though it has rebounded from last month’s trough.

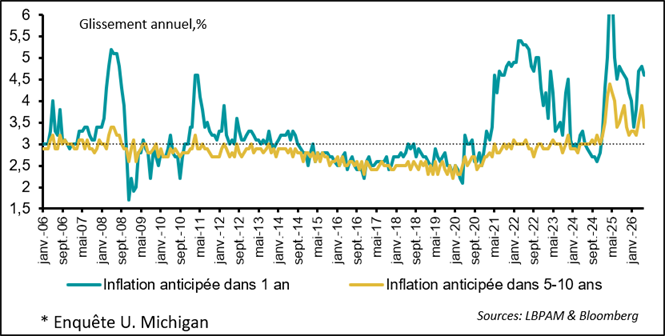

In addition, medium-term inflation expectations (3.4%) have edged down, although they remain elevated. This can be explained by the decline in gasoline prices since the end of May. This trend may be seen as reassuring for the Fed.

►In Japan, as expected, the BoJ raised its policy rate to 1%, its highest level in 31 years. In its statement, the Bank indicated that normalization should continue. However, the signal remained relatively cautious, still citing uncertainties in the Middle East. We believe that another rate hike should take place before the end of the year. At the same time, the impact on the currency was minimal, with the yen remaining extremely weak.

Going Further

Hormuz: even a gradual reopening is driving a sharp decline in energy prices

The announcement of the upcoming reopening of Hormuz is pushing energy prices downward

Energy prices have accelerated their decline following confirmation that an agreement has been reached to allow the Strait of Hormuz to reopen. The price of oil (Brent) was trading below 83 dollars per barrel this morning. Meanwhile, gas prices in Europe also followed the downward trend, albeit more cautiously, falling back below 43 euros per MWh, from 50 euros last week.

This decline may appear relatively rapid given the time required to normalize flows through the strait and, therefore, global oil supply. Nevertheless, it is consistent with a convergence of oil prices toward even lower levels around year-end. Our assumption of a Brent price in the 70–75 dollar range by mid-2027 appears reasonable.

Naturally, significant uncertainties remain regarding the final outcome of the conflict and the content of any agreement that may be reached between Iran and the United States in ongoing negotiations. However, on both sides, achieving a lasting resolution to the conflict appears to be an important objective.

The faster-than-expected dissipation of this shock is positive news for the global economy, as reflected in market reactions.

Inflation expectations declining

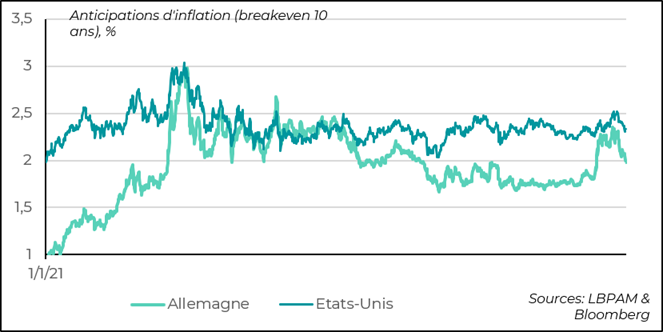

In particular, we have seen a rapid easing of inflation expectations in the bond market following the sharp decline in energy prices. This adjustment has been especially pronounced in the euro area.

This development should reassure the ECB regarding the potential inflationary pressures triggered by this shock in the European economy.

We maintain our view of a status quo in the ECB’s monetary policy. The market has become significantly less aggressive, scaling back its expectations for further rate hikes. That said, the risk of an additional increase in key interest rates remains if, in the coming months—by August in particular—inflation data were to show a stronger-than-expected pass-through of the energy shock, especially in services.

In our view, maintaining a stable monetary policy, combined with the continuation of Germany’s fiscal stimulus plan, should—at a time when the energy shock is fading and confidence is improving—support a rebound in the European economy by autumn, breaking the negative spiral observed in recent months.

United States: household confidence and housing market still struggling

Confidence still at historically low levels

The preliminary University of Michigan consumer confidence survey for June shows that U.S. households, overall, maintain a negative view of the economic situation. Indeed, the confidence index remains at a historically low level, even though it has rebounded from the extremely low point reached last month.

In part, this slight improvement may reflect the strengthening of the labor market in recent months, with job creation exceeding 180,000 per month.

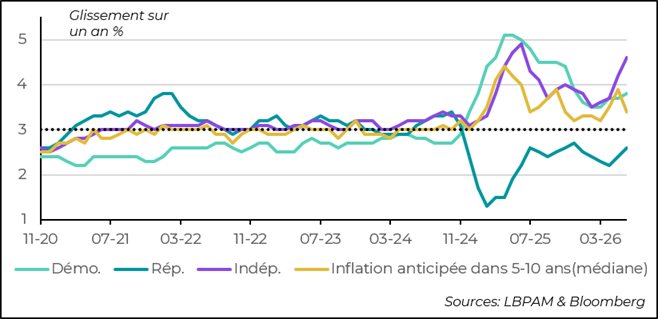

Inflation expectations declining…

This can also be explained by a decline in inflation expectations, particularly over the medium term. This trend likely reflects the drop in gasoline prices since the end of May, echoing the signs of a decrease in oil prices.

… but inflation expectations across political affiliations have remained on an upward trend

This message is also reflected in trend indicators that exclude, from monthly price movements, those that have experienced extreme changes (a total of 16% of prices with sharp increases or decreases are excluded). This indicator has also resumed an upward trend.

These developments should lead the Fed to adopt at least a wait-and-see stance. Some members of the monetary policy committee will likely advocate for a shift in tone in the statement, in order to remove the accommodative bias that has been maintained so far.

It remains to be seen how K. Warsh, the new Fed Chair—under strong pressure from D. Trump, who appointed him to lower interest rates—will manage communication around this new economic environment, characterized by rising inflationary pressures while growth has continued to hold up.

… but inflation expectations across political affiliations have remained on an upward trend

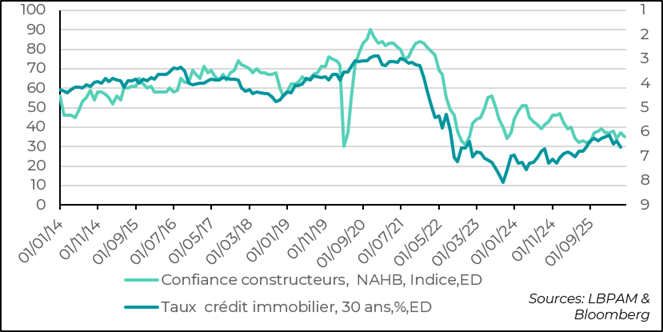

Another area of weakness in the U.S. economy is the residential construction sector. Indeed, higher interest rates are proving to be a significant headwind for the sector, despite government efforts to reduce borrowing costs.

As a result, housing is likely to continue to lag as a contributor to growth. In addition, in our view, consumption is expected to moderate somewhat this summer. At the same time, investment should remain a strong driver of growth, supported by tax credits that are boosting spending in sectors linked to the development of AI.

Japan: as expected, the BoJ raises its policy rate

Policy rates at their highest level in over 30 years

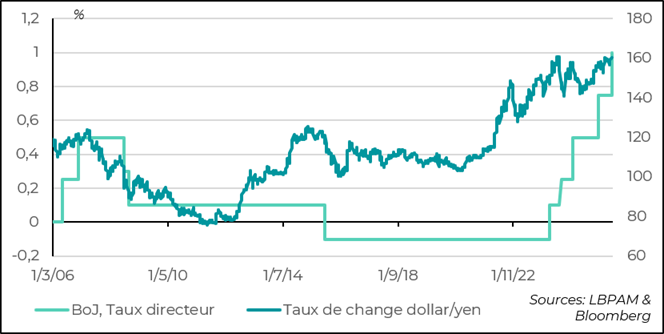

As we had anticipated for several months, the BoJ decided to raise its policy rate by 25 basis points, bringing it to 1%, its highest level since 1995. In its statement, the BoJ reiterated that the direction of monetary policy remains toward further tightening in order to move toward normalization, in a context where inflation is holding at the Bank’s target of 2%.

As expected, the BoJ did not refer to the government’s support policy that has capped energy prices, which has resulted in relatively subdued inflation in recent data. Underlying inflationary pressures should re-emerge once government support measures are withdrawn, particularly as global energy prices continue to decline.

It is worth noting that this rate hike, which had gradually been priced in by the market, had little impact on the yen. Indeed, the currency remains close to its lows against the dollar. This is likely to continue complicating the BoJ’s task and is one of the factors supporting the case for further monetary tightening. We expect at least one additional rate hike before the end of the year.

Sebastian Paris Horvitz

Director of Research