Still no visibility on how the crisis will be resolved

Link

What are the key takeaways from the market news on April 3, 2026? Xavier Chapard provides some insights.

Overview

► After a month of war, President Trump’s address to the nation did not provide any new information, as he continued to alternate between threatening and reassuring messages.

On the one hand, the United States will ‘hit Iran extremely hard over the next 2–3 weeks,’ the war is not a problem because ‘the economy will come back strong’ afterwards, and other countries can deal with the Strait of Hormuz on their own.

But on the other hand, ‘Iran is no longer a threat’ (war aim achieved?), negotiations for a ‘deal’ with the Iranians are ongoing, the United States will protect its allies in the Gulf, and there was no mention of the possibility of troops on the ground.

Surprisingly, the more reassuring news came from the Iranians, who are leaving the door open to ending the war (under conditions).

►Overall, attacks continue on the ground from both sides, and the resumption of traffic in the Strait of Hormuz remains minimal. The current situation of ‘escalation to de‑escalate’ leaves markets facing fairly binary short‑term risks that are difficult to assess. Under these conditions, markets have been very volatile, moving with the flow of contradictory information, but without any real trend for the second week in a row. For risk assets, which have fallen significantly but have not overreacted given the scale of the shock and the uncertainty, both upside and downside potential remain substantial.

We remain relatively optimistic over the medium term, given our scenario of de‑escalation after a few weeks of conflict and a decline in energy prices during the second quarter. But the risks of a much more negative scenario remain high. Conversely, we believe that the current level of interest rates offers opportunities: de‑escalation would reduce inflationary risks and the likelihood of significant policy rate increases, while continued escalation would heighten recession risks and increase demand for safe‑haven assets.

►The latest U.S. economic data have been surprisingly strong.

The rebound in retail sales and industrial activity in January and February suggests that the economy was re‑accelerating slightly at the beginning of the year after the slowdown at the end of 2025.

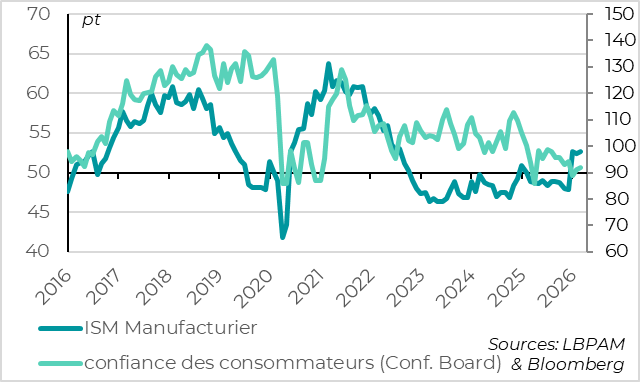

And this momentum appears to be continuing in March despite the war in Iran, as shown by the increase in car sales, the rise in the manufacturing ISM, and the improvement in consumer confidence.

The latter is benefiting from the stabilization of the labor market, which should be confirmed by the official employment reports for March published today.

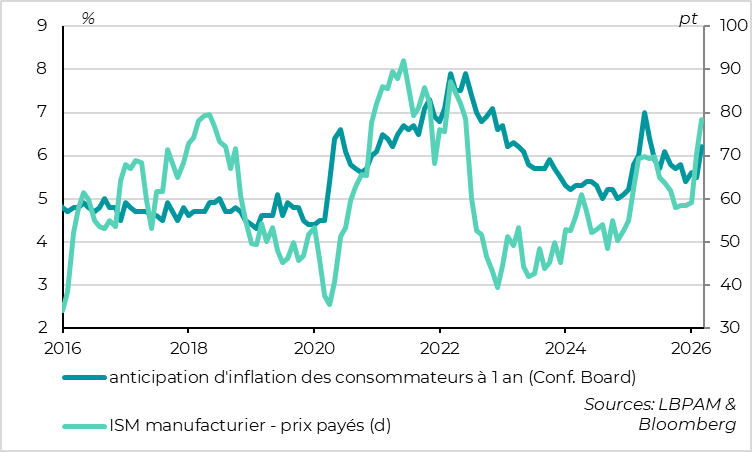

►That said, the March surveys also confirm that energy‑related inflation will not spare the United States, which will weigh on household purchasing power and on consumption in the middle of the year.

The U.S. economy is therefore less exposed to the energy shock than other major economies, but it is not immune. And this maintains the risk that inflation — already persistent before the shock — will not converge toward the 2% target.

Under these conditions, we believe that the Fed will wait at least until next year before lowering its rates.

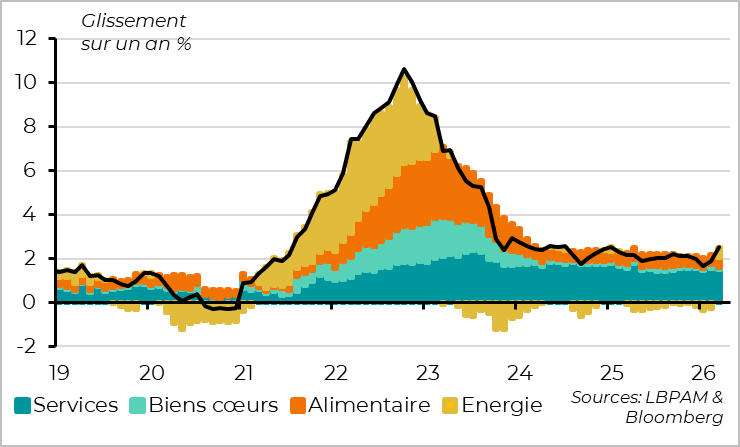

►In the euro area, inflation accelerated sharply in March due to energy prices, rising from 1.9% to 2.5%. And it will continue to accelerate in the second quarter.

However, this increase is slightly less pronounced than expected by both the consensus and the ECB, because core inflation slowed from 2.4% to 2.3%. This shows that inflationary pressures had normalized before the energy shock, which reduces the risk of a strong and lasting acceleration in core inflation.

This is why we think the ECB is likely to raise rates only once this year, rather than the three increases anticipated by the markets.

►By contrast, in Japan, the quarterly Tankan survey — which came in very strong — reinforces our scenario of two rate hikes by the BoJ this year, with a first hike possible as early as the end of the month if geopolitical uncertainty eases somewhat by then. Indeed, Japanese business confidence continued to improve in March, reaching its highest level since 1991, long‑term inflation expectations remain on an upward trend, and corporate financial conditions remain solid despite the rate increases already implemented.

Going further

World: First signs of a marked slowdown in activity in March

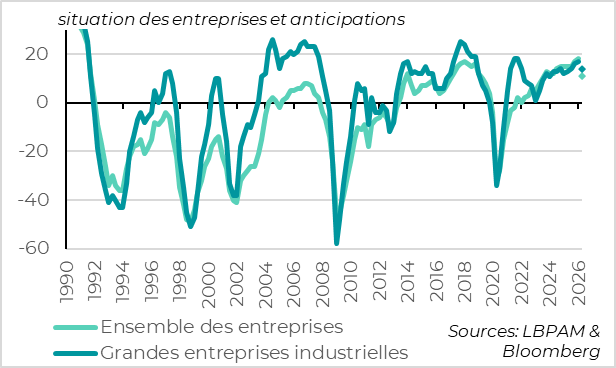

Business and consumer confidence increased in March

Recent U.S. activity data are reassuring.

Before the shock in March, the economy was slightly re‑accelerating and the labor market appeared stable.

Retail sales picked up again in January (+0.1%) and February (+0.5%) after stagnating at the end of 2025. Similarly, industrial production rebounded in January and February (+0.7% and +0.2%) after having declined in the fourth quarter of 2025.

This positive momentum seems to have continued in March despite the initial effects of the war in Iran. Car sales are still increasing, returning to their pre‑shutdown level. Most importantly, employment appears stable, with 62,000 private‑sector jobs added according to ADP, a further decline in unemployment claims — now below last year’s level — and no notable increase in layoff announcements in March.

More surprisingly, and unlike the rest of the world, household and business surveys did not decline in March. This suggests that the impact of the energy shock on activity is, for now, limited.

Consumer confidence increased slightly according to the Conference Board survey, reaching a three‑month high, although it remains historically depressed (91.8 points). This improvement reflects the stabilization of households’ current situation, supported by labor market resilience, which offsets a slight decline in expectations for the coming months.

On the corporate side, the manufacturing ISM rose again in March to 52.7, its highest level in four years. The rebound in industrial production therefore appears to be continuing, even though leading indicators (orders, employment) edged down slightly.

The decline in PMIs is broad‑based, but more pronounced in Europe

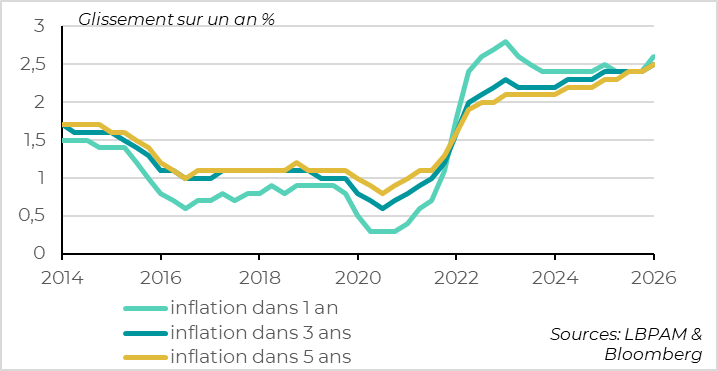

By contrast, price indicators show that the United States will not be spared from rising inflation. The ISM manufacturing prices‑paid index jumped by 8 points to 78.3, its highest level since mid‑2022. Similarly, households’ one‑year inflation expectations rose from 5.5% to 6.2% in March.

However, these expectations remain reasonable given the surge in gasoline prices — from under $3 to over $4 per gallon in a month — and they remain below the level observed after the reciprocal tariffs were announced last April.

The rise in gasoline prices and in certain directly affected goods and services (airfares, etc.) is expected to push inflation from 2.5% to 3.5–4% in the second quarter.

Beyond that, second‑round effects from energy prices on other prices and wages have historically been weaker in the United States than elsewhere, meaning that the scars of this shock on inflation should almost disappear after a year. But because the United States was already facing overly persistent inflation before the energy shock, this shock could extend the uncertainty around returning to target until next year.

U.S. indicators hold up slightly better in March

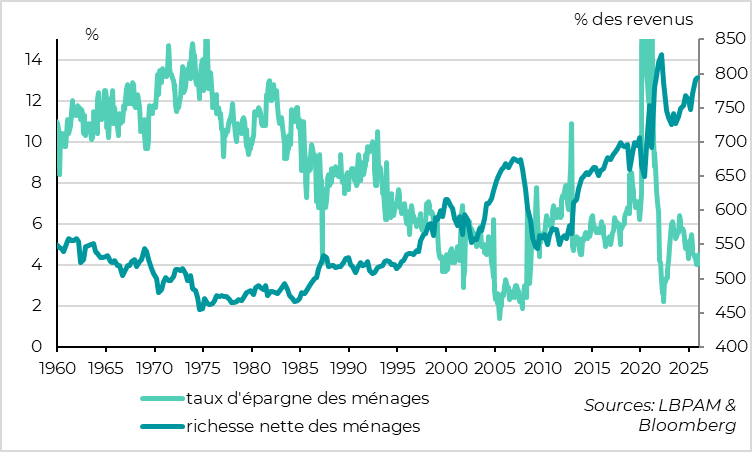

As for activity, the rise in energy‑related inflation will nevertheless weigh on household purchasing power. Households have already smoothed last year’s supply shocks (the slowdown in employment and tariffs) and benefited from the very favorable wealth effects of recent months, which means their savings rate is already low at the onset of this shock (at 4.5%).

Even if employment and growth should withstand the energy shock, consumption and overall activity are still expected to slow in the middle of the year.

Euro area: Inflation accelerates in March, but slows excluding energy

Inflation rises sharply in March due to energy

Euro‑area inflation jumped by 0.6 percentage point in March, rising from 1.9% to 2.5%, although this remains slightly below what could have been expected given the shock to energy prices. It is notably 0.1 percentage point lower than the inflation forecast published by the ECB two weeks ago.

Energy prices rose sharply, increasing by 6.5% in March. And this rise is expected to continue in the coming months, even if oil and gas prices begin to ease before the end of April. We anticipate that headline inflation will exceed 3% over the next two months.

Goods and services prices reverse their unexpected increase from February

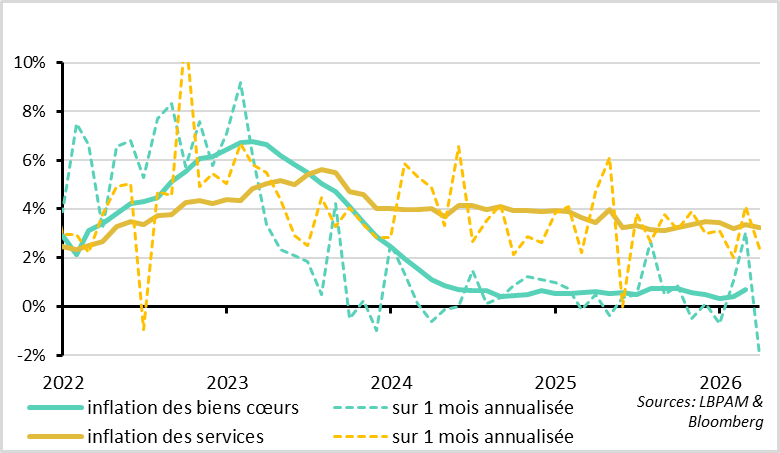

But excluding energy, the other components of inflation slowed in March. Food inflation fell from 2.5% to 2.4%. Most notably, manufactured goods inflation (0.5% after 0.7% in February) and services inflation (3.2% after 3.4%) reversed their February increases. This confirms that the earlier rise was driven by temporary, specific factors (Olympics-related effects in Italy, sales periods in France, etc.).

Core inflation was therefore normalized before the energy shock

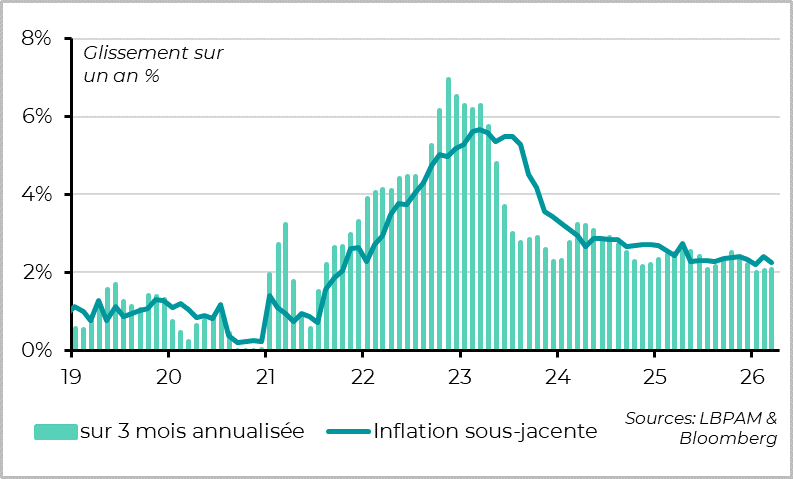

In fact, core inflation (that is, excluding energy and food) slowed from 2.4% to 2.3%, and the sequential increase in core prices has been consistent with the 2% target over the past three months. This confirms that inflationary pressures were normalized before the start of the war in Iran. We are far from the situation before the war in Ukraine, when core inflation was already at 4% and accelerating.

The rise in costs generated by the energy shock will exert some upward pressure on core inflation in the coming months and slow its decline in the coming quarters due to second‑round effects. However, under our scenario of easing energy prices during the second quarter, we believe that core inflation should not re‑accelerate much beyond 2.5% and should resume a slightly downward trend from the second half of the year. Core inflation would ultimately return fully to 2% only in the second part of next year, rather than this year.

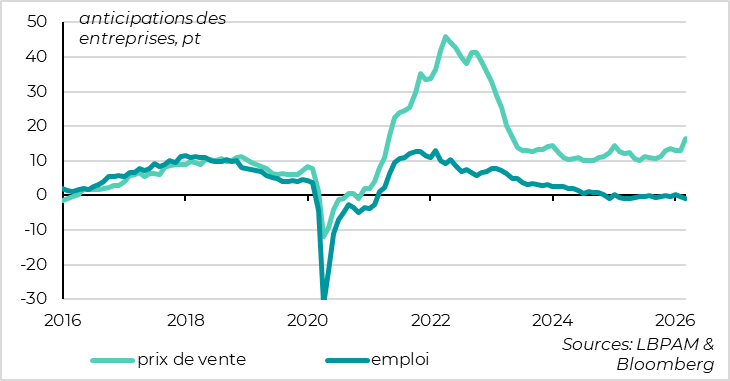

Costs are accelerating sharply, while selling prices are rising somewhat less

The first business surveys show that there will indeed be second‑round effects, with firms expecting to pass on part of their cost increases to selling prices. The indicator for expected selling prices rose in March, reaching its highest level since mid‑2023.

However, the magnitude of these effects — and therefore the persistence of inflation — should remain limited. Expected selling‑price increases are far more modest than in 2021 and 2022, and they are concentrated in goods rather than services. Moreover, labor‑market conditions remained stable in March, at a neutral level, which reduces the risk of a price‑wage spiral.

The March surveys will not fully reassure the ECB regarding the risk of more persistent inflation, but they tend to support our view that this risk is more limited than in 2022. This is why we believe the ECB will raise rates only once this year, compared with the three increases currently anticipated by the markets.

Japan: Business confidence leaves the door open to interest‑rate hikes

Business sentiment is at its highest level since the early 1990s

Japanese companies report that economic conditions are the best since 1991 in the first quarter, according to the Bank of Japan’s (BoJ) quarterly Tankan survey. This survey, conducted after the start of the war (between February 26 and March 31), is very positive, even though it likely does not yet fully capture the impact of the energy crisis and firms expect slightly less solid conditions for the second quarter.

More specifically, the indicator of current conditions rose from 17 to 18 points, and expectations for the second quarter stand at 14 points. The increase in confidence is driven by large manufacturing firms, which is not surprising given the weakness of the yen and the favorable tech cycle in Asia. But conditions are also strong in other sectors and for small firms, suggesting that domestic momentum is also supportive.

Inflation expectations continue to rise

The details of the survey show that inflationary pressures continue to rise, which is reassuring in terms of a lasting exit from deflation.

Corporate inflation expectations increased again in the first quarter, both in the short and long term, with three‑ and five‑year expectations reaching their highest levels since the survey began twelve years ago.

Moreover, indicators of capacity constraints and labor‑market tightness remain stable at elevated levels.

Financial conditions for companies remain positive

Finally, the survey shows that corporate financing conditions and banks’ credit supply remain positive despite the Bank of Japan’s rate hikes over the past two years, which have brought the policy rate to its highest level since the mid‑1990s, at 0.75%.

This survey should greatly reassure the BoJ about its ability to raise rates further without disrupting the reflation cycle of the Japanese economy. Despite the uncertainty caused by the energy shock, we continue to expect two rate hikes this year, with a good probability that the BoJ will raise rates as early as its next meeting at the end of April.

Xavier Chapard

Strategist