The decline in oil prices is confirmed

Link

What are the key takeaways from the market news on June 30, 2026? Sebastian Paris Horvitz provides some insights.

Overview

►Despite the mutual attacks between the United States and Iran over the weekend, both countries have returned to the negotiating table. As a result, both the market’s expectation and our own are that the Strait of Hormuz will continue to reopen. Energy prices should stabilize at low levels in the short term and are likely to remain relatively subdued in 2027, at around USD 75 per barrel of Brent crude, reflecting an oil market that would remain oversupplied, as it was before the conflict.

►This more favorable energy price environment, even though gas prices in Europe are declining more slowly, is a highly positive development for the global economy. In particular, it should help prevent an overreaction from monetary policymakers. This underpins our more moderate outlook than the market’s regarding the future path of policy rates set by the major central banks.

►Yesterday, at the opening of the ECB Forum in Sintra, Christine Lagarde indicated that the recent decline in energy prices is broadly in line with the more optimistic scenario presented at the latest monetary policy meeting, under which inflation would converge relatively quickly—by 2027—towards the ECB’s 2% target. Against this backdrop, we do not see a need for a more restrictive monetary policy stance. The euro area inflation figures for June, due to be released today, should confirm a further modest easing in price pressures.

►Obviously, given the recent comments from several central bankers—including Isabel Schnabel, who remains highly concerned about inflation—the risk is that a more hawkish approach could prevail at the ECB’s July meeting. However, this is only our alternative scenario.

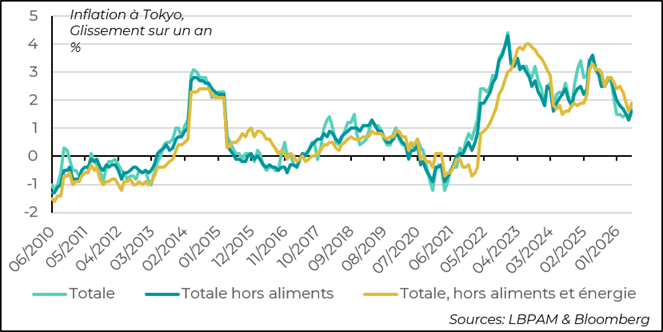

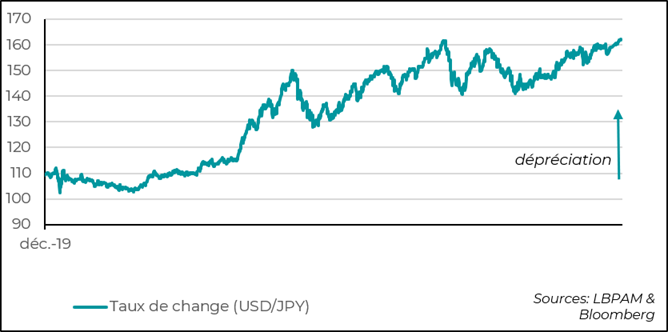

►In Japan, Tokyo’s June inflation data—widely regarded as a leading indicator of nationwide inflation—came in slightly above expectations. Notably, core inflation excluding fresh food and energy accelerated to 1.9% year-on-year, despite the price control measures that remain in place. These figures should reinforce the Bank of Japan’s commitment to continuing its monetary policy normalization. We continue to expect at least one policy rate hike by year-end. Persistent downward pressure on the yen suggests that monetary policy remains excessively accommodative.

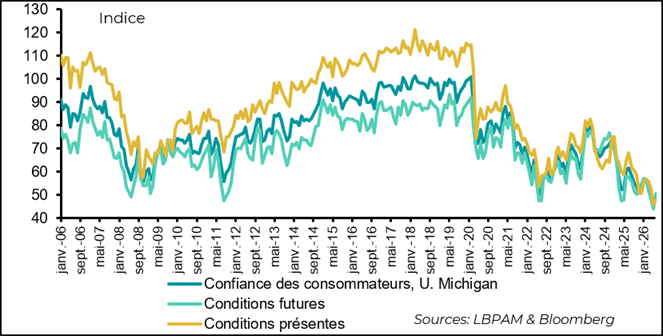

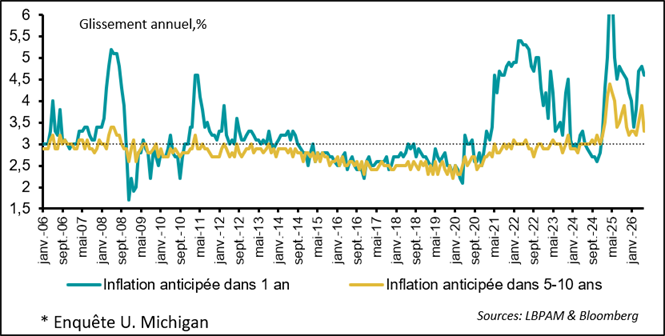

►In the United States, the gradual decline in gasoline prices since late May, combined with growing expectations that the Strait of Hormuz will remain open, has, as anticipated, led to a modest rebound in consumer confidence, according to the University of Michigan survey. However, confidence remains historically low. In particular, medium-term inflation expectations (over the next 5–10 years) have fallen significantly since last month. Nevertheless, at 3.3%, they remain above their average level of recent years.

►Also in the United States, the Supreme Court reaffirmed the Federal Reserve’s special status by rejecting the possibility that President Trump could dismiss Governor Lisa Cook from the Federal Reserve Board without valid cause. This ruling reinforces the Fed’s independence from the executive branch. At the same time, the Supreme Court curtailed the autonomy of other federal agencies—particularly those with supervisory and regulatory powers—which had prevailed for nearly a century, thereby granting the President broader authority over the appointment and removal of their leaders.

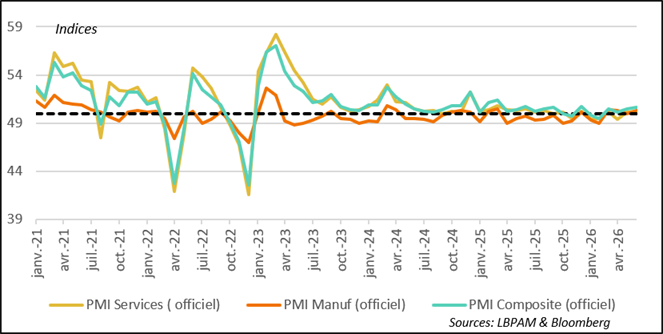

►In China, the release of the official PMI data for June showed that, despite a very modest rebound in activity, overall economic momentum remains weak, particularly in the services sector. We continue to believe that the authorities will maintain their policy of targeted support measures for the domestic economy in order to achieve their GDP growth objectives, especially given that the export sector remains resilient.

Going Further

United States: Consumer Confidence Rebounds Slightly on Lower Energy Prices

Consumer Confidence Rebounds Slightly, but Remains at Historically Low Levels

The University of Michigan’s final June consumer sentiment survey showed a modest rebound in confidence. Nevertheless, sentiment remains at historically low levels, with a still very wide gap between respondents identifying with Republican views and the rest of the population.

The fact that confidence remains so weak continues to warrant close attention regarding the strength of the U.S. consumer. However, consumer spending has so far proven relatively resilient.

Gasoline Prices Have Declined Significantly Since Late May

One of the key drivers behind this modest improvement in consumer confidence is, of course, the decline in gasoline prices over the past month. During the latest week, the average price of a gallon of gasoline finally fell below the USD 4 mark.

This decline in fuel prices is a positive development for household purchasing power. However, given the relative resilience of consumer spending so far despite the squeeze on real incomes, we expect consumption to show some signs of moderation in the near term before regaining momentum in the autumn, supported by a labor market that should remain robust.

Inflation Expectations Are Adjusting Favorably

The decline in gasoline prices has also quickly translated into a moderation of inflation expectations. In particular, medium-term inflation expectations (5–10 years ahead) have moved lower, returning close to their lowest levels since the outbreak of the conflict with Iran, although they remain above the average observed in recent years.

This is clearly positive news for the Federal Reserve.

Nevertheless, we continue to believe that, given the resilience of the U.S. economy and the persistence of elevated inflation, the Fed may ultimately need to adopt a slightly more restrictive stance in order to ensure that inflation expectations remain firmly anchored. Such an approach would also be consistent with the signals provided by K. Warsh, the new Fed Chair, who has expressed a desire to see inflation return rapidly to the 2% target.

That said, it seems unlikely that the Fed, under K. Warsh’s leadership, would raise interest rates ahead of the congressional midterm elections scheduled for November. Against this backdrop, a rate hike in December currently appears to be the most likely scenario.

Japan: June Inflation Confirms the Continuation of Monetary Tightening

Tokyo inflation for June came in slightly above expectations. In particular, core inflation excluding energy and fresh food accelerated to 1.9% year-on-year, despite the price-control measures implemented by the authorities, which continue to cap energy prices.

This figure shows that underlying inflation dynamics remain fully consistent with the Bank of Japan’s projections, which foresee inflation remaining close to its 2% target.

In fact, it could be argued that inflation may, over time, accelerate more than is currently anticipated, particularly once government subsidies on energy prices are phased out.

Against this backdrop, we continue to believe that the Bank of Japan will need to press ahead with the normalization of its monetary policy. We expect at least one further policy rate increase by year-end, especially as tensions in the Middle East continue to ease and Japan maintains an expansionary fiscal stance.

The Yen Remains Close to Its Lowest Levels

Moreover, the yen remains close to its recent lows, and depreciation pressures continue to be significant. So far, the government has found it difficult to contain these pressures, despite repeated warnings of possible foreign exchange intervention.

Admittedly, almost all major currencies have recently come under downward pressure against the U.S. dollar as expectations of further Federal Reserve rate hikes have strengthened. Nevertheless, it is clear that the yen still appears substantially undervalued.

Against this backdrop, we believe that an adjustment in monetary policy represents the most appropriate strategy to support the currency and contain any potential inflationary pressures.

China: Economic Activity Remains Relatively Weak

Activity Shows a Marginal Improvement, but Remains Weak

China’s official PMI survey for June came in slightly stronger than expected, but the data primarily highlight the fact that economic activity remains subdued. Both the manufacturing and services PMIs are hovering only marginally above the 50 threshold that separates expansion from contraction.

Tomorrow’s release of the S&P Global PMI surveys will provide additional insight, but the available evidence already suggests that activity—particularly in terms of domestic consumption and investment—remains relatively sluggish.

For the time being, policymakers continue to rely heavily on the resilience of exports, which have been supported in particular by strong demand linked to investment in artificial intelligence infrastructure.

However, we believe that, in order to achieve the government's 4.5%–5.0% GDP growth target, the authorities will continue to provide targeted support to the domestic economy over the coming months, especially through measures aimed at boosting household consumption.

Sebastian Paris Horvitz

Director of Research