The disillusionment with President Trump’s promises to end the war

Link

What are the key takeaways from the market news on June 02, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► Since the beginning of the ceasefire two months ago, the U.S. president has repeatedly announced an imminent agreement to end the conflict with Iran. Unfortunately, to date, no agreement has been reached.

►Nevertheless, markets have become convinced that the latest announcements were more credible. In fact, for many observers, ourselves included, both parties must quickly find a way out. The economic and political costs of maintaining the status quo are considerable.

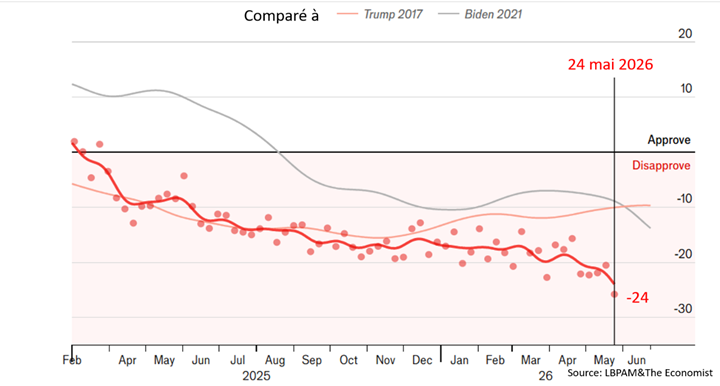

►In particular, according to The Economist’s regular poll on public opinion of the president, D. Trump’s unpopularity—driven by the war and the loss of purchasing power—has reached its lowest level since the survey was launched in 2009.

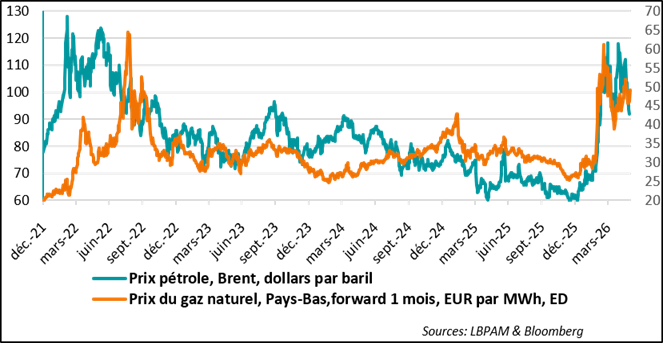

►Against this backdrop of expectations for a swift resolution, the price of a barrel of oil has been steadily declining over the past two weeks, falling from $105 per barrel to $95 yesterday. This decline is primarily based on the assumption of a two-step plan: an extension of the current ceasefire for two months, allowing time to finalize discussions on Iran’s nuclear program, the lifting of sanctions on the country, and potentially the return of its financial assets.

►In these circumstances, given the lack of progress so far, one can only be concerned about the final outcome. Nevertheless, despite the significant uncertainties surrounding the progress of these negotiations, we still expect an agreement—even a minimal one—that would allow the reopening of the Strait of Hormuz. This would lead to a gradual normalization of maritime transport, particularly for oil and gas.

►In this scenario, the energy shock should gradually fade by the end of the year. At the same time, the negative effects already underway are still expected to weigh on growth.

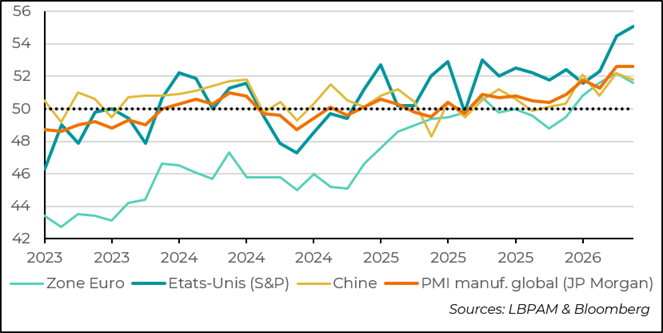

►However, these negative effects are distributed quite unevenly. On the corporate side, PMI surveys for the manufacturing sector continue to hold up fairly well across most of the world. Thus, the global manufacturing index published by JPMorgan, based on S&P’s final surveys for May, remained stable compared to the previous month, still in expansion territory. By contrast, activity in the services sector appears much less resilient across the board. This reflects the negative impact of rising energy costs on demand.

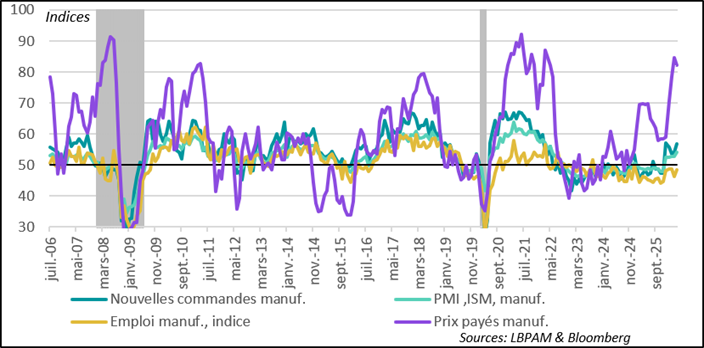

►On a regional level, differences are also pronounced. In the United States, industrial activity remains very strong, particularly in the technology sector, which is also supported by investment tax credits. This sector continues to play a dominant role in the performance of the U.S. stock market. The ISM survey for May also confirmed this strength, with the index reaching its highest level in four years.

►In Europe, industrial activity is also holding up, but its expansion is much less robust than across the Atlantic. In particular, new orders are significantly weaker. The only positive news in S&P’s final survey was the upward revision of activity in France, although it still remains in contraction territory.

►At the same time, unsurprisingly, the May PMI survey confirms that cost pressures at the global level remain strong, given the persistence of high energy prices. Indeed, the index of prices paid by companies has reached its highest level since 2022.

►The effects of inflation on demand are clearly visible, particularly in the euro area, where economic data have been strongly disappointing for the past two months.

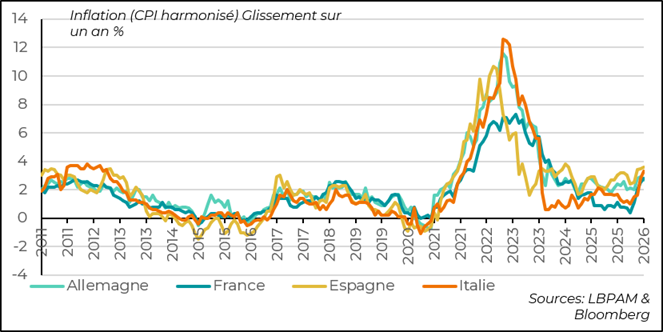

►Indeed, inflation figures for May for the four main economies came in, as expected, higher on a year-on-year basis. Spain and Italy are showing inflation well above 3%, while in France and Germany, although rising, it remains below that level. However, today’s release for the euro area as a whole is expected to confirm that headline inflation stands at around 3%, largely driven by higher energy prices.

►However, the focus will mainly be on core inflation, in order to assess whether increases in energy prices are feeding through to other prices (second-round effects). Members of the ECB’s Governing Council are divided on how to respond to this shock. We still believe that a rate hike in June is highly likely, as it would help firmly anchor expectations. While market-based expectations in the bond markets remain consistent with the central bank’s target, household surveys point to a rising trend in medium-term expectations.

►In Japan, the inflation reading for the city of Tokyo in May—an अग्र leading indicator of nationwide inflation—came in lower than expected. Headline inflation on a year-on-year basis slowed again to 1.4%, down from 1.5% the previous month. Core inflation, meanwhile, declined to 1.6%.

►Obviously, interpreting Japanese data is heavily affected by base effects, but also by the implementation of subsidies aimed at reducing energy costs. Petrol prices are still capped. Nevertheless, the BoJ is likely to take into account its own inflation forecasts, which remain close to its target levels. This is why we continue to believe that the BoJ should raise its rates in June, in order to continue the normalization of its monetary policy. This rate increase should help ease the persistent downward pressure on the currency.

Going Further

Iran War: A Slow Exit, but an Exit Nonetheless from the Current Crisis

The potential reopening of the Strait of Hormuz is pushing energy prices downward

Statements by President Trump about an imminent agreement with Iran to reopen the Strait of Hormuz have contributed to a decline in oil prices over the past 15 days. As a result, the price of a barrel of Brent crude has been below $100 for the past week. Although this level remains high, it should be seen as an initial easing of the energy shock that the global economy has been facing since the start of the war in Iran.

It is well understood that the reopening of the Strait of Hormuz will not immediately restore normal oil and gas supply conditions. However, the oil market is expected to adjust prices quickly to reflect the anticipated easing of supply pressures by the end of the year. While prices may remain elevated in the very short term, the downward trend should strengthen in the coming months.

Of course, this favourable scenario of a normalization in global oil and gas supply remains subject to the uncertainties that have surrounded negotiations over the past two months. As recently as yesterday, despite reassuring statements from D. Trump, Iranian officials announced the suspension of talks, notably in response to Israeli strikes in southern Lebanon against Hezbollah, its ally.

Nevertheless, a fairly strong consensus has emerged regarding the need for both parties to bring this conflict to an end. Indeed, the economic and political costs for both sides have become very significant.

The war has already had a significant political cost for D. Trump

In the U.S. case, although President Trump recently stated that he is not concerned about the upcoming midterm elections in November, it is clear this is unlikely to be true.

The president’s decline in opinion polls has been historic. If we look at The Economist’s survey on the popularity of U.S. presidents, conducted since 2009, we see that D. Trump has recently reached his lowest level since the survey began. The gap between favorable and unfavorable opinions has reached -24 points.

Only an end to this war is likely to stop this deterioration.

Therefore, we maintain our baseline scenario of a resolution to the crisis in the coming weeks, while remaining cautious given the succession of disappointments over the past two months and the growing negative impact of this shock on global activity.

Manufacturing PMI: Global Activity Remains Well Oriented

The global manufacturing PMI for May continues to signal strong activity

The final S&P survey for manufacturing PMIs in May once again came in very positive, with an index that, although no longer increasing, remains at its highest level in recent years.

Global industrial activity is therefore defying the negative effects of the energy shock. Across the board, the manufacturing sector continues to expand.

However, there are marked differences between countries. One of the main contributors to this resilience in industrial activity remains the United States, where the PMI continues to gain ground.

By contrast, in the euro area, while industrial activity is holding up, the sector is losing momentum.

This clearly highlights that the energy shock has affected different regions of the world in very uneven ways.

United States: The ISM Survey Confirms the Strength of the Manufacturing Sector

The manufacturing ISM index has reached its highest level in four years

The ISM survey on activity in the manufacturing sector confirmed the findings of the S&P survey. Indeed, the overall activity index reached its highest level in four years.

All sub-indices showed robust results, except for employment, which remains in contraction territory.

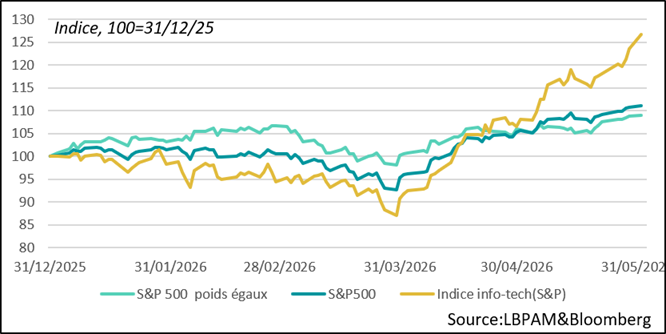

According to the survey, the expansion of industrial activity spans almost all sectors, but is being driven particularly strongly by the technology sector, which is being boosted by the development of artificial intelligence.

Indeed, the very large investments being made in this race for innovation—also supported by substantial tax credits (35% of investment spending is deductible)—are playing a leading role in the U.S. economy.

The distortion of the economy driven by AI is strongly reflected in stock market dynamics

Massive spending to build the infrastructure needed to support the growing demands of AI is leading to significant bottlenecks in supply chains, particularly in the semiconductor industry. This has recently translated into an almost extraordinary rise in stock prices of companies linked to these technologies, with market capitalizations reaching record highs.

Euro Area: Weaker Activity and Rising Inflation

Economic data have been highly disappointing in recent months

In the euro area, the energy shock has completely disrupted the growth momentum seen at the start of the year. This is particularly evident in the string of disappointing economic data releases. This stands in clear contrast to the United States.

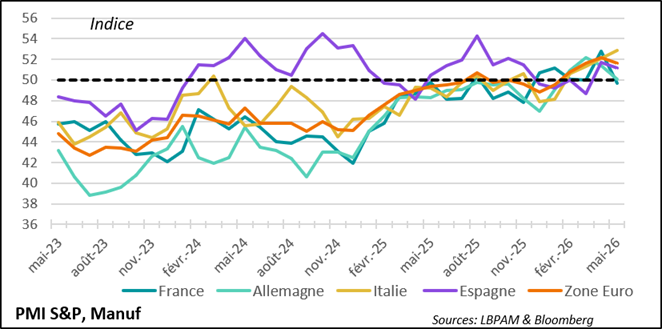

Industrial activity is holding up but is weakening in some countries

As shown by S&P’s final PMI survey for May, industrial activity remains in expansion territory, but its momentum is weakening. This is particularly the case in France and, to a lesser extent, in Germany. By contrast, in southern euro area countries, activity is holding up much better.

A rapid resolution of the crisis would clearly be very positive for the region and help restore momentum. This remains our baseline scenario for the end of the year, supported in part by Germany’s stimulus plan.

Inflation is accelerating in the euro area

The main factor affecting activity is clearly the energy shock. Indeed, the first inflation figures for May showed that headline inflation has accelerated significantly, although in several countries less than expected.

These inflation figures will be closely analyzed by the ECB to assess whether second-round effects—potentially making the inflation shock more persistent—are gaining importance given the duration of the shock.

It is difficult to believe that the shock will not spread to other prices in the coming months, due to the continued rise in energy prices. This could, in turn, affect inflation expectations.

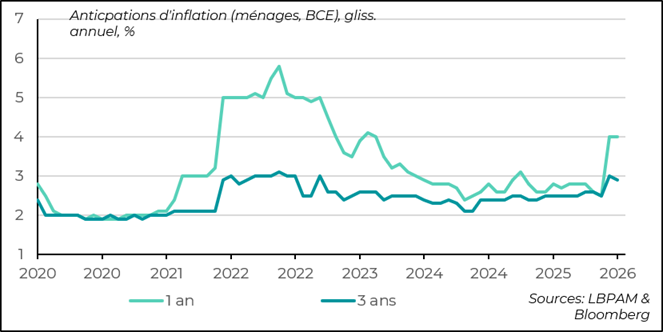

Inflation expectations are easing slightly but remain high

Indeed, the latest household inflation expectations survey for April showed that, although expectations were easing somewhat, they remained relatively elevated for the medium term (three years ahead). However, this contrasts with expectations in bond markets, which remain fully consistent with the ECB’s 2% inflation target.

Overall, we still expect the ECB to raise its policy rate in June in order to better anchor expectations. However, this would not signal the start of a broader rate-hiking cycle.

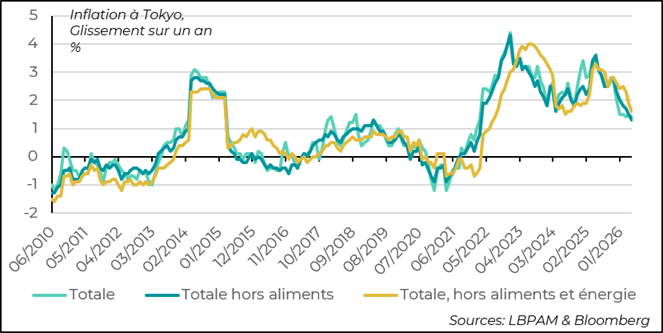

Japan: Inflation Held Back by Price Controls

Domestic demand disappointed in April

The release of Tokyo inflation data for May, which showed a further slowdown, highlights the impact of the support measures implemented by Ms. Takaichi’s government. In particular, by capping gasoline prices, inflation is being restrained and the energy shock is effectively muted.

A headline inflation rate of just 1.4% year-on-year could suggest that the BoJ will remain cautious and refrain from acting. However, we believe the opposite: if the BoJ follows its own inflation projections, it should take into account the fact that current subsidies will eventually be removed, allowing prices to adjust in the future.

In this context, we continue to expect the BoJ to raise its policy rates in June. This would support the ongoing normalization of its monetary policy, help better anchor inflation expectations, and prevent downward pressure on the yen from intensifying further.

Sebastian Paris Horvitz

Director of Research