The ECB raises its rates to counter inflation risks

Link

What are the key takeaways from the market news on June 12, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► Despite U.S. attacks on Iran and Iranian retaliation, and above all the belligerent rhetoric of the U.S. president, the market continues to bet on a resolution to the conflict. Above all, the dominant view today is that the Strait of Hormuz will reopen in the near term.

►Yesterday, the U.S. president announced during the day that a major attack on Iran was imminent, before stating a few hours later that the attacks would not take place, emphasizing that negotiations with the Iranian authorities were progressing. This sequence, to say the least surprising, culminated in a further decline in oil prices (Brent), bringing it down to $89 per barrel, its lowest level since April 20.

►Although, according to some sources, vessels are managing to transit through Hormuz, we are still far from a full reopening. However, these signs are encouraging. Oil prices stabilizing around $90 per barrel in the coming months would already be reassuring for the global economy and for markets.

►At the same time, as uncertainty around the Strait of Hormuz persists, the major central banks will deliver their verdict in the coming week on the policy stance they intend to adopt in response to the energy shock.

►The ECB was the first to act. As was widely expected, it decided to raise its key interest rates by 25 basis points (bp), for the first time since autumn 2023. With inflation accelerating (3.2% in May), primarily driven by energy prices, monetary authorities are concerned about a potential de-anchoring of inflation expectations.

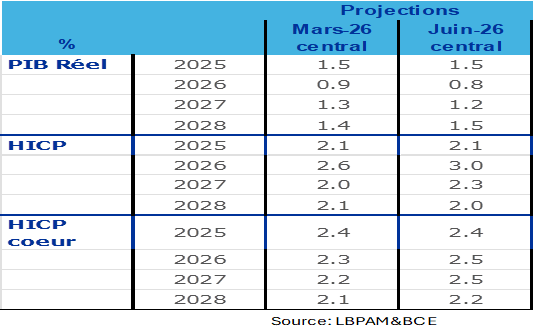

►These concerns are reflected in the ECB’s latest projections for price developments in the coming years, which are seen as slightly higher than in March. In the new forecasts, inflation would only return to 2.0% in 2028, rather than 2027 previously. At the same time, ECB economists expect growth to prove more resilient after the slowdown in 2026.

►While the risk remains that inflation could prove more persistent given the duration of the energy shock, we continue to believe that the negative effects on demand should prevent an inflation overshoot that would require a much more restrictive monetary policy. Accordingly, we maintain, for now, our projection that this hike will be the only one in 2026 and likely in 2027 as well.

►We will have the Fed next week. For members of the monetary policy committee, the decision to maintain their current policy stance and to emphasize the need to remain cautious about inflation risks will be relatively straightforward, given the inflation data that have just been released.

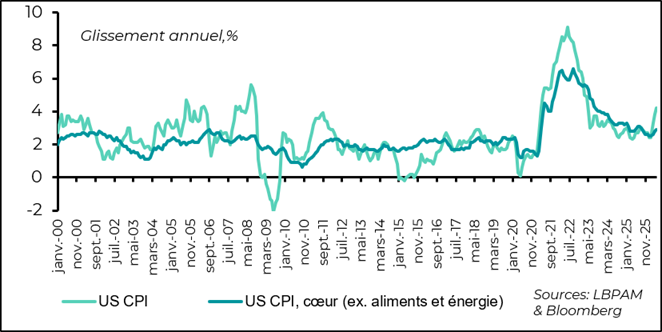

►Inflation, as measured by the Consumer Price Index (CPI), accelerated, as expected, to 4.2% year-on-year, driven by energy prices. The level reached is the highest since April 2023. Core inflation recorded a more moderate increase, rising to 2.9%.

►Some components of inflation sent less reassuring signals, such as services inflation—particularly excluding energy and housing—which showed a notable acceleration, rising to 3.7% year-on-year. In addition, the measure calculated by the Cleveland Fed, which excludes prices with extreme movements (both upward and downward), continued its upward trend, reaching 2.9% year-on-year. Finally, producer prices increased much more than expected, and, importantly, the components included in the calculation of the Personal Consumption Expenditures (PCE) deflator—the Fed’s preferred gauge—accelerated sharply, suggesting that the PCE should also pick up in May.

►Another piece of information highlighting the negative impact of the energy shock in the United States is the further decline in the small business confidence index. The overall index has reached its lowest level since October 2024.

Going Further

ECB: first rate hike since September 2023

Growth would be slightly weaker and inflation higher

Yesterday, the ECB decided to raise its key interest rates by 25 basis points (bp), for the first time since autumn 2023. This hike was widely expected, which explains the reaction in the bond market, particularly to the decision of the monetary authorities.

This increase was partly justified by the ECB staff’s new economic projections. These suggest that, given the duration and magnitude of the energy shock, inflation is expected to remain somewhat higher than previously estimated at the March meeting. Thus, in the baseline scenario, headline inflation would only converge to 2% on average by 2028, rather than 2027.

At the same time, growth projections for 2026–2027 are expected to be slightly lower than previously anticipated.

These projections provide a framework for the ECB’s current actions. Nevertheless, there are, of course, significant uncertainties regarding the outcome of this crisis and its economic impact. In this context, the ECB has added a more moderate scenario to the previously considered ones, which had assumed larger shocks. In this scenario, inflation dynamics would be much more benign, with headline inflation falling below the 2% target as early as 2027, to 1.8%.

For now, we remain in the camp advocating a moderate ECB response to the risk of a potential escalation of the energy shock feeding through into broader prices and triggering an inflationary spiral.

At this stage, if the current trend in energy prices persists, a more moderate scenario appears more aligned with reality.

Moreover, the outlook for growth seems relatively optimistic. It appears that the shock has had a stronger impact on demand, which should be reflected in the data for the second and third quarters. In this context, price pressures are likely to be more contained, in our view. Above all, it remains to be seen whether the transmission of this shock is as significant as the ECB anticipates. If not, the ECB is likely to remain cautious. As usual, monetary authorities have emphasized that they remain data-dependent.

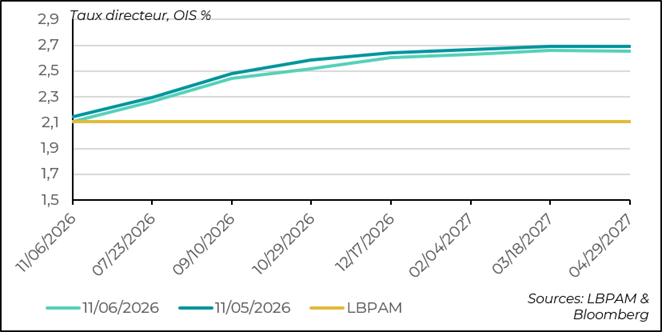

The market maintains a more aggressive view of the ECB’s reaction function

These considerations lead us to maintain a less aggressive view of the ECB’s future policy path than the market’s. Indeed, markets are pricing in two additional rate hikes, whereas we believe the ECB should remain more cautious and wait for incoming economic data in the coming months before adopting a more aggressive stance. It is worth noting that market-based inflation expectations have declined significantly and remain well anchored.

Admittedly, the duration of this conflict could lead to stronger indexation effects than we anticipate. At the same time, it is fairly clear that the impact on growth has been among the most significant in the developed world, despite the continued support provided by fiscal stimulus policies in certain European countries, notably Germany.

United States: Rising inflation and growing concerns among small businesses

Inflation accelerated sharply in May

As expected, headline inflation rose sharply in May, reaching 4.2% year-on-year. Core inflation increased more moderately, to 2.9%. Unsurprisingly, energy prices were the main contributor. Given the recent evolution of energy prices, with expectations of a reopening of the Strait of Hormuz already translating into a downward trend in gasoline prices in the U.S., it is likely that the peak in energy price increases has been reached.

Nonetheless, it remains to be seen how this energy shock will feed through into the U.S. economy, especially considering that even before the shock, the disinflation process—particularly in services—was progressing relatively slowly.

Trends calling for caution

In this context, some indicators of the transmission of the energy shock should send a signal of caution to the Fed. Indeed, a key variable is the behavior of services prices excluding energy. These show a clearly upward trend. In particular, the measure often highlighted by J. Powell, the Fed Chair—namely services prices excluding energy and housing—is showing a fairly strong upward trend, accelerating to 3.7% year-on-year.

In addition, the measure of prices considered relatively sticky, published by the Atlanta Fed—that is, prices that adjust only slowly—has also resumed an upward trend.

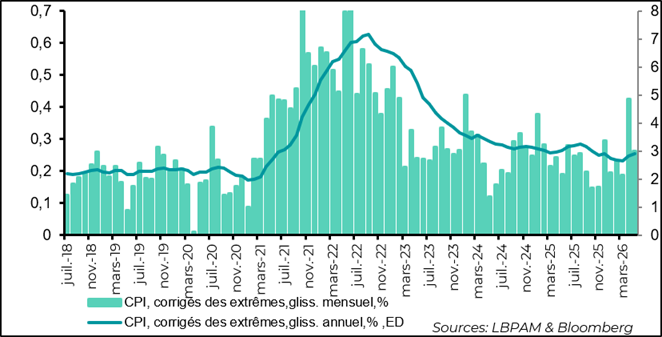

The trend indicator that excludes extreme movements is rising

This message is also reflected in trend indicators that exclude, from monthly price movements, those that have experienced extreme changes (a total of 16% of prices with sharp increases or decreases are excluded). This indicator has also resumed an upward trend.

These developments should lead the Fed to adopt at least a wait-and-see stance. Some members of the monetary policy committee will likely advocate for a shift in tone in the statement, in order to remove the accommodative bias that has been maintained so far.

It remains to be seen how K. Warsh, the new Fed Chair—under strong pressure from D. Trump, who appointed him to lower interest rates—will manage communication around this new economic environment, characterized by rising inflationary pressures while growth has continued to hold up.

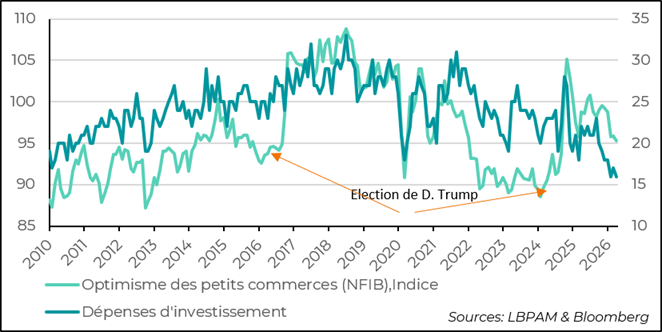

Small businesses are growing concerned

While the U.S. economy as a whole has proven very resilient so far, it is worth noting that in some sectors, the negative effects of the energy shock are beginning to weigh. This is the case for small businesses.

Indeed, the NFIB small business confidence survey declined again in May. The index has erased all of the strong gains recorded since D. Trump’s election.

Rising costs are becoming a major constraint, along with increasing uncertainty. This is reflected across most underlying indicators, particularly investment intentions. This is consistent with our view of a slowdown in activity this summer in the United States, driven in part by consumption, following what is likely to be relatively robust GDP growth in Q2 2026.

Sebastian Paris Horvitz

Director of Research