The German recovery plan is beginning to support growth

Link

What are the key takeaways from the market news on February 27, 2026? Xavier Chapard provides some insights.

Overview

► Trade uncertainty (U.S. tariffs) and geopolitical uncertainty (U.S.–Iran negotiations) have been absorbed mainly by long-term interest rates, which fell to their lowest levels in three months at the end of February for both the United States (4%) and Germany (2.7%). This allowed equities to remain slightly bullish, while oil prices stayed volatile just above 70 dollars per barrel.

►The global 10% tariff (excluding goods exempted from reciprocal tariffs), implemented under Section 122 to replace the tariffs deemed illegal by the Supreme Court, went into effect on Tuesday, without immediately being raised to 15% as D. Trump had announced. This slightly reduces the average tariff rate (from 15% to 12%, compared with 2.5% before the start of the trade war) and is expected to slightly increase the U.S. budget deficit (a few tenths of a percentage point of GDP on top of a deficit already expected to be around 6% of GDP)… but it does not fundamentally change the macroeconomic outlook. That said, many uncertainties remain: what about the reimbursement of the illegal tariffs collected, which represent about 0.5 percentage point of GDP? Will the global tariff be raised to 15%? And how will it be replaced once the 150‑day period allowed under Section 122 expires?

►Meanwhile, economic data have remained rather supportive, bolstered by accommodative fiscal policies, which leads us to stay well‑exposed to risky assets and cautious on bonds.

►In the United States, the latest employment data seem to confirm the stabilization of the labor market, with jobless claims remaining very low and a slight rebound in consumer confidence in February. This is reassuring for short‑term growth and should strengthen the Fed’s wait‑and‑see stance. We expect only one additional Fed rate cut, while markets are pricing in two by the middle of next year.

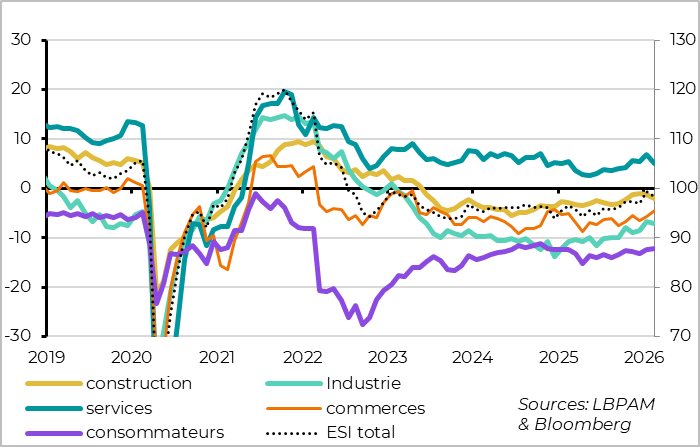

►In the Eurozone, the European Commission’s confidence survey eased slightly in February after its strong increase in January, mainly due to a small decline in confidence among French businesses. But like the PMIs and the German IFO, the survey remains consistent with stable growth at the start of 2026, close to potential. We continue to expect an acceleration over the course of the year, supported by the German recovery plan.

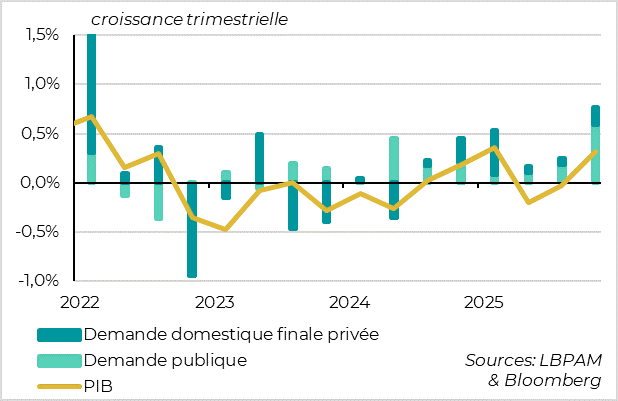

►In this regard, the breakdown of German GDP for Q4 2025 is very reassuring, as it shows that the return to growth was driven by an acceleration in public demand, particularly public investment (+10% over the quarter). This suggests that Germany’s historic investment plan is beginning to take shape.

►In Asia, the yen and Japanese long-term yields came under renewed pressure this week following the government’s proposal to appoint two very dovish economists to the Bank of Japan this year. This revived concerns that the Prime Minister, who has historically favored low interest rates, might pressure the BoJ not to raise rates. While this is clearly a dovish signal from the government, it does not fundamentally change the outlook in our view. These are only two of the nine voting members on monetary policy, and they are replacing two members, one of whom was also very dovish. We continue to anticipate two BoJ rate hikes this year and believe that the yen offers attractive diversification in the event of a risk‑off shock.

Going further

United States: Signs of labor‑market stabilization appear to be confirmed in February

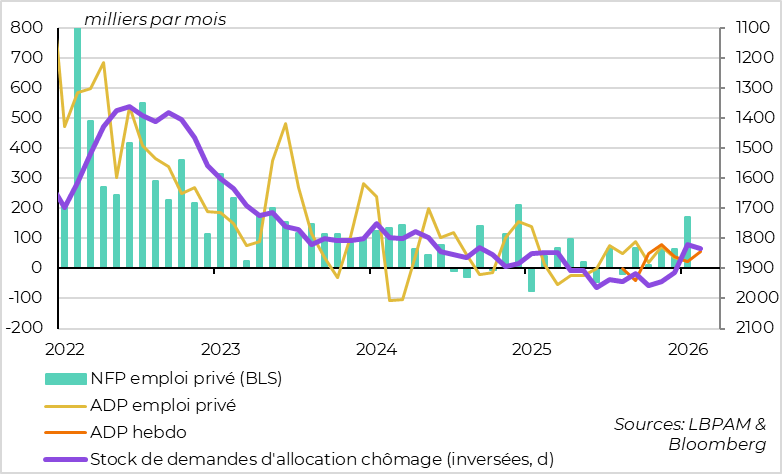

The latest employment figures continue to surprise on the upside

The exceptionally strong official January employment figures (130,000 job creations and a drop in the unemployment rate to 4.3%) were reassuring, but needed to be interpreted with caution given the usual volatility of these data at the start of the year and the weakness of alternative indicators. However, the first data available for February are once again surprising to the upside. This bodes well for the official reports due next week and seems to confirm that the labour market is picking up somewhat at the start of the year after slowing sharply last year.

Jobless claims remain low in February even though seasonality is far less favourable than in January. New claims have reversed their late‑January/early‑February increase over the past two weeks, and continuing claims have returned close to their early‑year lows by mid‑February. In addition, private‑sector job creation has edged up in early February (+12.75 thousand) according to weekly ADP data, reaching its highest level since November.

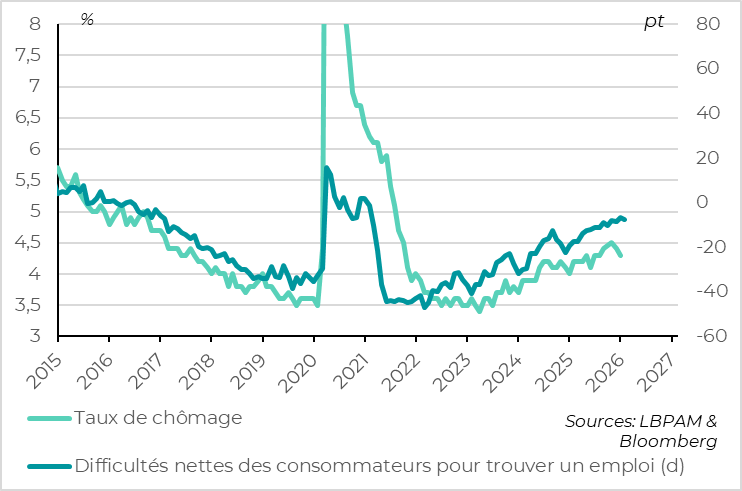

Households are slightly less pessimistic about the labour market in February

Most importantly, households do not seem as pessimistic about the labour market in February as they were in January, according to the Conference Board’s confidence survey. This is reassuring for the unemployment rate, which is probably the most important indicator for the Fed in the current context.

Consumer confidence increased slightly in February, from 89 to 91.2 points, after a somewhat smaller decline in January than initially estimated (84.5 in the January estimate). The improvement in February mainly reflects better household expectations, which can be volatile. But households also indicate that current labour‑market conditions are stabilising. The gap between the share of households reporting that jobs are plentiful and those saying jobs are hard to get — one of the best leading indicators of the unemployment rate — widened slightly in February, from 6.8 to 7.4 points.

Overall, these data are reassuring after some disappointing macro releases (December retail sales, February PMI). Above all, they support the Fed’s wait‑and‑see stance, adopted since the beginning of the year due to the easing of labour‑market risks and the persistence of inflation. In this context, we still believe that market expectations of more than two Fed rate cuts this year remain exaggerated, and we stay cautious on U.S. rates.

Eurozone: Growth is not accelerating at the start of 2026, but it remains solid

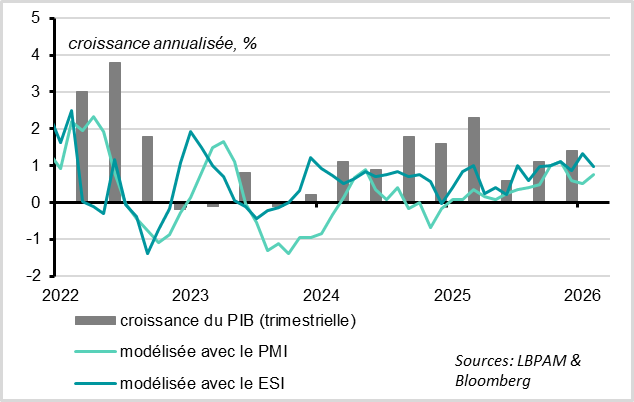

Economic Sentiment and PMIs point to stable growth in February

The European Commission’s Economic Sentiment Indicator (ESI) eased in February, from 99.4 to 98.3, but this comes after a very strong increase in January that had brought it to its highest level in three years. As was the case last month, it is moving in the opposite direction from the PMIs, which picked up slightly in February. The gap between the euro area’s two best cyclical indicators is therefore narrowing, and both point to stable growth of around 0.3% per quarter.

The downside is that the ESI remains below its long‑term average (100), as it has for the past four years, suggesting that growth is not yet accelerating above potential. But the positive side is that the trend in cyclical indicators remains slightly upward and consistent with resilient growth—already a decent outcome given ongoing trade and geopolitical uncertainties.

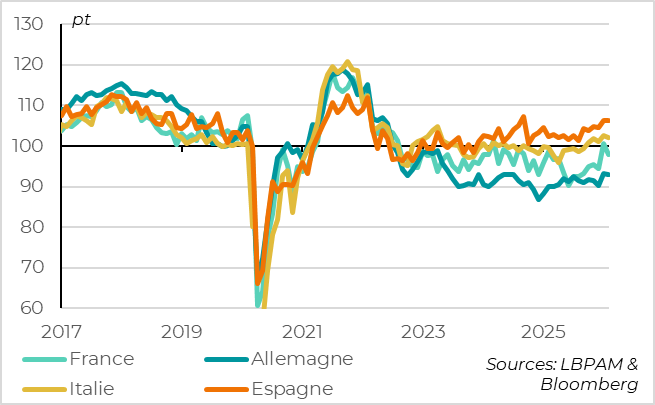

Economic Sentiment softens in France but remains stable in the rest of the Eurozone

The decline in Economic Sentiment comes from France, where business confidence has softened after a strong increase in January. This is also what the February INSEE survey shows, although both indicators remain consistent with slightly positive growth.

Outside France, Economic Sentiment is stable in the other large euro area countries, which is rather encouraging after their January increase. The indicator remains low in Germany, which is somewhat disappointing given that it is likely more relevant for tracking the impact of the German stimulus plan since, unlike the PMI, it includes the construction sector, which should benefit from higher infrastructure investment. Still, it has reached its highest level in two and a half years, and the IFO survey suggests that the outlook is improving more clearly.

Business confidence is easing, but household confidence is improving

Business confidence is easing slightly after several months of gains, both in industry and services. This likely reflects the persistent uncertainty weighing on business sentiment and limiting investment prospects. This is also consistent with corporate credit demand, which remained weak in January.

However, confidence continues to improve for retailers and households. This suggests that consumption remains well‑oriented, supported by a resilient labour market and the high level of household savings.

Overall, euro area growth does not appear to be accelerating markedly at the start of 2026, but it remains solid. We continue to expect growth to move slightly above potential over the course of the year, driven by rising household purchasing power and the German stimulus plan.

Germany: Public demand has been strongly supporting growth since late 2025

Public demand has been accelerating noticeably since late 2025

The second estimate of German GDP for Q4 2025 confirms the return to growth (+0.3% q/q) and, more importantly, that this growth is being driven by domestic demand, particularly public demand.

Household demand is increasing, with a 0.5% rise in private consumption and the first increase in private residential investment in two and a half years. This offsets another decline in corporate investment.

But most importantly, it is the sharp acceleration in public demand that is driving growth. Public consumption rose by 1.1% over the quarter following the delayed approval of the budget in September, and public investment jumped by 10%, the strongest increase since the Covid period.

After the strong rise in public orders at the end of 2025, this confirms that German fiscal policy is beginning to provide significant support to growth. Budget data for January indicate that this continues at the start of 2026. We continue to expect the German government to implement a large share of its very ambitious investment plan—focused on defence and infrastructure—which underpins our more positive view than consensus on growth in Germany and the Eurozone over the next two years.

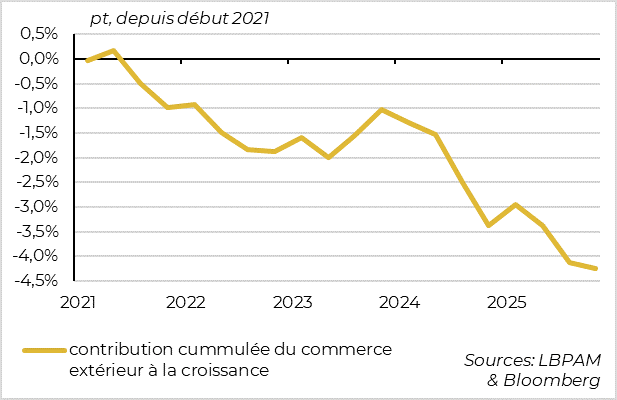

Germany’s external trade has been weighing heavily on growth since the Covid period

Moreover, the Q4 GDP figures confirm that Germany’s former growth engines remain depressed, which gives the government an additional incentive to stay proactive.

External trade continues to weigh on growth (‑0.1 pp in Q4), for the eighth consecutive quarter. In addition to the direct impact on activity, this also drags on industrial investment. Since 2021 and the beginning of the energy shock, net exports have shaved more than 4 percentage points off Germany’s cumulative growth.

Xavier Chapard

Strategist