The global economy remains hostage to the war

Link

What are the key takeaways from the market news on May 5, 2026? Sebastian Paris Horvitz provides some insights.

Overview

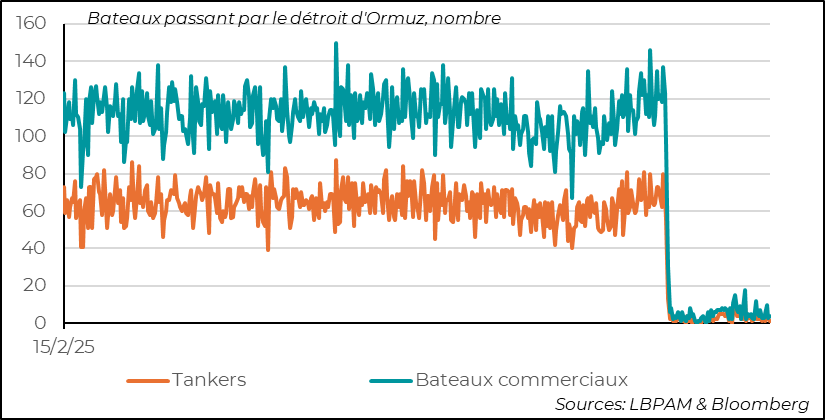

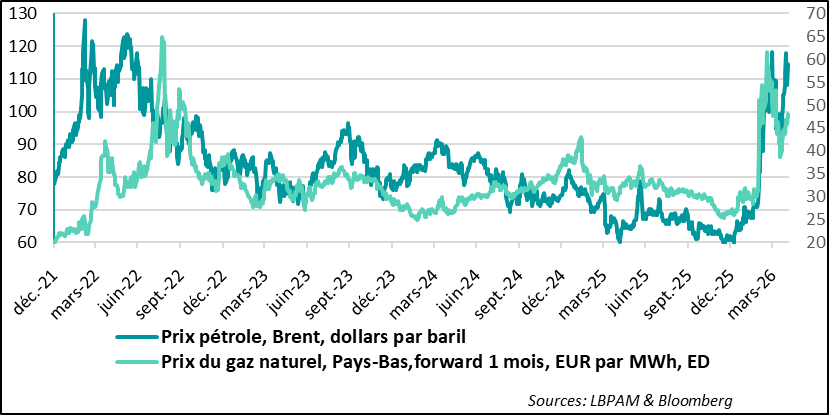

► The barrage of statements from President Trump, alternating between tough and conciliatory tones, while Iranian officials appear unwilling to resume talks, is far from bringing us closer to a resolution of the crisis. As a result, the Strait of Hormuz remains closed due to an Iranian and American blockade. Under these circumstances, it is not surprising that the price of a barrel of oil (Brent) remains well above 100 dollars. In fact, the past few hours have seen a series of skirmishes, including an Iranian attack on a port in the United Arab Emirates. This renewed rise in tensions raises fears of a resumption of attacks and bombings.

►Without an exit from this war, it is clear that risks to the global economy are increasing, as a major energy shock—combining sharp price increases and shortages—continues. We still believe that a resolution of the conflict is clearly in the interest of both belligerents. For President Trump, the continuation of this war, which is very unpopular with Americans, is politically (midterm elections) and economically (declining purchasing power) very costly. For the Iranian authorities, it is equally clear that this war continues to weaken the regime in power. However, the deadlock in negotiations reflects an inability to find compromises, preventing any progress through an increasingly opaque tunnel.

►Resolving this crisis through force—particularly through a resumption and intensification of American and Israeli bombings—does not appear compatible with a timeframe that would be “acceptable” for the global economy. Such a development would prolong the current energy shock, with even greater costs. Just one additional month with oil or gas prices at today’s levels could deal a far more severe blow to global growth, including by weakening sectors that are currently still holding up.

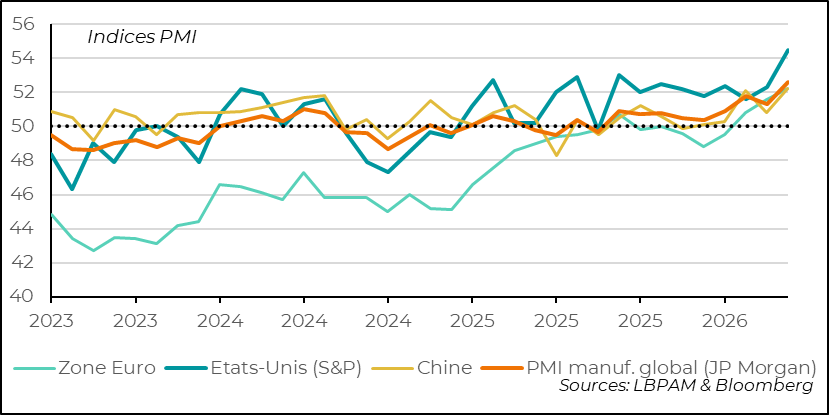

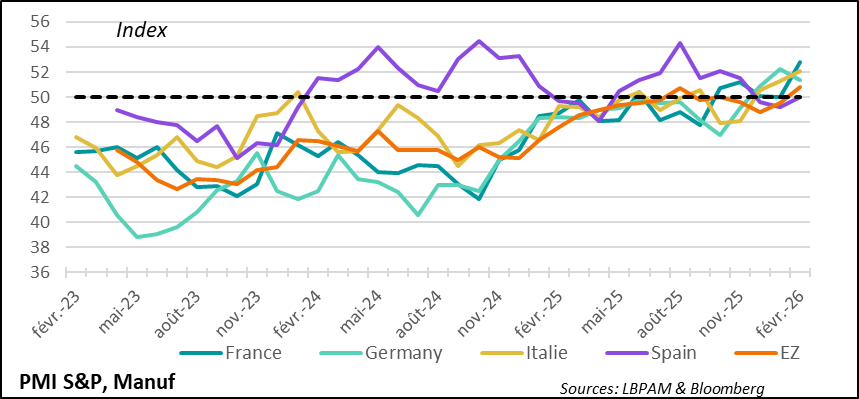

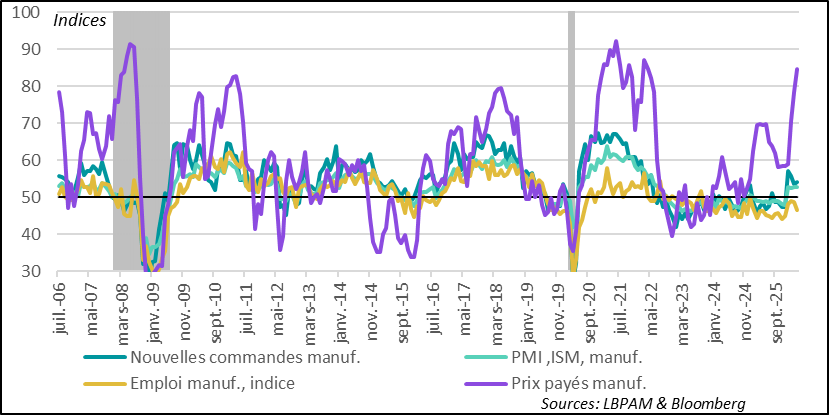

►It is true that, so far, industry in particular appears to be holding up against the shock of the war. This has been confirmed by JPMorgan’s global PMI indicator, which is based on S&P’s PMI surveys across a wide range of countries and rose in April to reach its highest level in more than four years, at 52.6. This growth dynamic is broadly shared among the countries surveyed. Nevertheless, this positive news may not last. Indeed, the acceleration in activity has been largely driven by a front‑loading of orders by companies, reflecting fears of further cost increases (mainly energy-related) and potential supply shortages ahead.

►It is worth noting that the strength of industrial activity has also benefited, quite markedly, the countries most exposed to the expansion of infrastructure related to artificial intelligence (AI), notably Japan, Taiwan, South Korea, and the United States, to name the most significant ones. At the same time, in the euro area, industrial activity has remained well oriented across all countries, even if part of the continued improvement there is more closely linked to inventory-building effects. Finally, across the board, input costs have reached very high levels, which could become a drag on future activity.

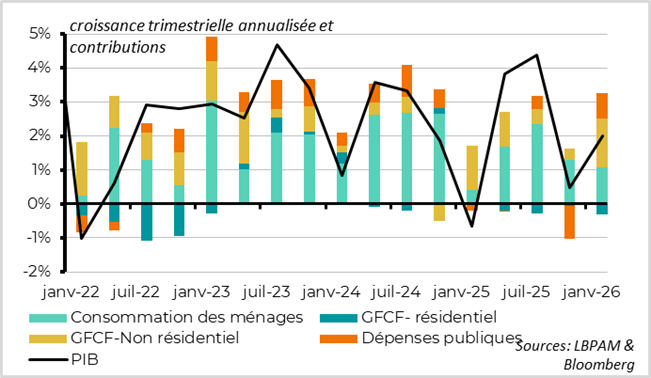

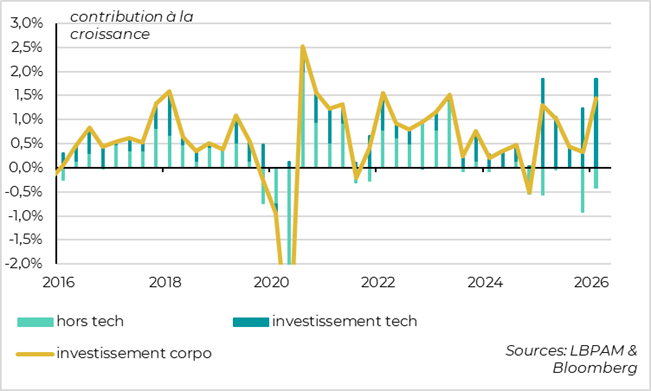

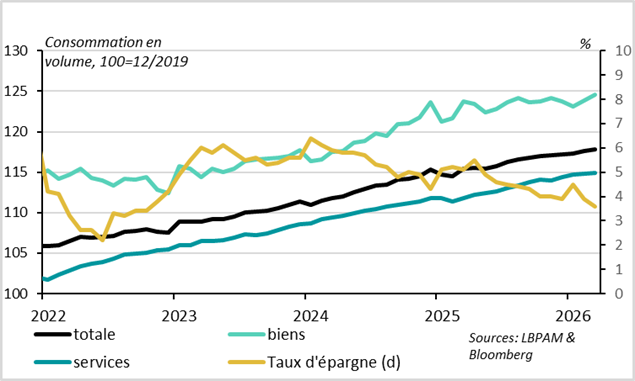

►As highlighted, the resilience shown by U.S. industry is driven in particular by activities related to the development of artificial intelligence (AI). The robustness of this segment has, moreover, made a significant contribution to GDP growth in the first quarter of 2026, with growth reaching 2% on an annualized basis. Nevertheless, despite a slowdown, consumption remains one of the pillars of the U.S. economic expansion. It continues to be supported by still relatively favorable financial conditions, while the labor market remains fairly stable. At the same time, the March consumption data show that although spending was solid given income growth, it was made possible by a further decline in the savings rate. This decline does not appear sustainable.

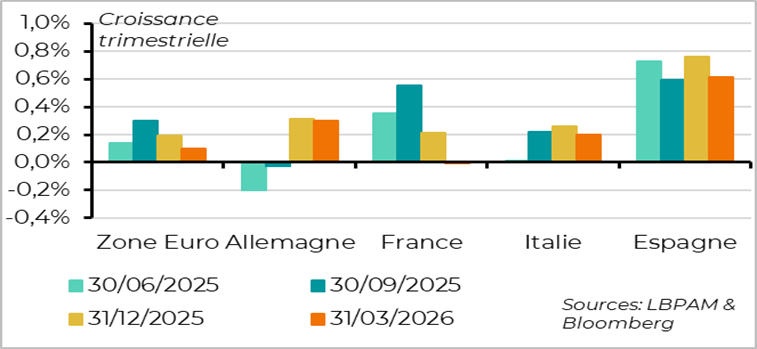

►In the euro area, GDP growth in the first quarter of 2026 came in slightly below expectations, at 0.1%. Nevertheless, excluding the evolution of Irish GDP, which is always very volatile, the region’s expansion reached 0.2%. Among the major economies, France was the biggest disappointment, with GDP stagnating, while Spain remained the strongest performer, posting growth of 0.6%. However, this resilience in growth now appears to be undermined by the energy shock. Indeed, the resilience of the industrial PMI in April seems to reflect mainly a surge in precautionary orders by firms aiming to anticipate higher costs and potential shortages. In fact, the impact of the shock appears to be much more visible in the services sector. It seems clear that rising energy costs and the associated uncertainty have nipped in the bud the recovery momentum that had begun to take shape at the start of the year.

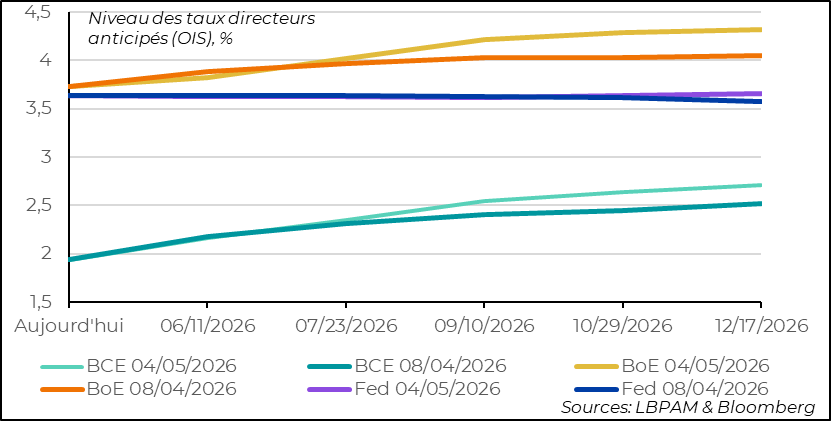

►In this context of uncertainty, last week the world’s main central banks communicated their assessment of the current shock and its implications for monetary policy. As anticipated, central bankers broadly agreed on the need to adopt a high degree of caution in the very short term. As a result, the Fed, the ECB, and the Bank of England all decided to leave their policies unchanged. Nevertheless, the Fed appears to be clearly settling into a wait-and-see stance, keeping its interest rates unchanged throughout 2026. By contrast, in Europe—both at the ECB and the BoE—the concern among central bankers is that this shock could fuel more persistent inflationary pressures. At this stage, we believe that market expectations of future ECB rate hikes (three in 2026) are exaggerated. We maintain the view that a precautionary hike in June is likely, with only a risk of a second hike by the autumn. For the United Kingdom, where inflation has been more persistent, we believe that two rate increases by the end of 2026 are possible.

Going Further

War in the Middle East: No progress in the reopening of Hormuz

War in the Middle East: No progress in the reopening of Hormuz

The hopes raised by the April 7 ceasefire for a more lasting halt to the conflict are fading day by day. As a result, the Strait of Hormuz remains closed, while tensions are rising again. On both sides, there appears to be both a willingness—and even a necessity—to put an end to the conflict, yet at the same time no progress is visible in the search for common ground and/or the concessions required to reach an agreement.

U.S. strategy seems increasingly focused on betting on the success of its “over‑blockade” of Hormuz, with the aim of completely crippling the Iranian economy and forcing a form of capitulation by the current regime.

This strategy is extremely risky for the global economy. The longer this shock persists, the more negative the consequences will be for a large number of economies worldwide. It is difficult to imagine any economy being spared from the slowdown that would result if this shock were to continue, even for just one additional month.

Energy prices have tightened again amid the deadlock

This is all the more true as oil prices remain well above 100 dollars, while gas prices in Europe are approaching 50 euros per MWh.

Following yesterday’s Iranian and U.S. attacks, the risk of the conflict once again escalating is significant. This could push prices even higher and amplify shortages that are already present in many countries, further weighing on economic activity.

For now, even though we have acknowledged that the conflict is likely to last longer than initially expected, with negative repercussions for growth, we still believe that the most likely scenario remains one of a resolution that would help ease pressures on the global economy in the coming month. Needless to say, the risks of more adverse scenarios have increased.

Central banks: Exercising caution to contain inflationary pressures

The market is anticipating too much tightening by European central banks

Unsurprisingly, central banks have chosen to act with caution in the face of the stagflationary shock caused by the war in Iran. As a result, the main central banks have decided to keep their policies unchanged. However, the future path that central banks are likely to follow appears to differ between the United States and Europe.

The Fed seems to be moving toward maintaining its current, relatively neutral policy stance throughout 2026. Indeed, inflation—which had not converged to target before this crisis—now risks remaining elevated for longer due to the surge in energy prices. At the same time, the relative resilience of the U.S. economy means that labor market conditions remain stable, thereby limiting concerns, for now, about a deterioration in employment. As a result, maintaining the current policy stance appears, in our view, to be the most appropriate course of action at this stage. In this respect, it is worth noting that three members of the monetary policy committee voted against the final statement, seeking to remove language suggesting that the institution’s bias remained tilted toward further monetary easing.

In Europe, with regard to the ECB, we believe that market expectations of three rate hikes by the end of 2026 are exaggerated. That said, it appears fairly clear that members of the Governing Council are prepared to tighten monetary policy slightly in order to clearly signal the ECB’s determination to keep medium-term inflation expectations firmly anchored. Accordingly, we believe that a 25‑basis‑point increase in policy rates in June is reasonable, with a risk of a second hike by the autumn.

For the Bank of England, the outlook may prove more complex. This shock comes at a time when inflation was still well above target, partly driven by government tax increases. As a result, we believe that the BoE is likely to raise rates twice by the end of the year. A third hike could become necessary if the UK economy proves more resilient than we currently anticipate.

Global manufacturing PMI: Beneath the resilience lies underlying weakness

Manufacturing PMIs remained well supported in April

The global PMI for April, published by JPMorgan on the basis of S&P’s PMI surveys, came in higher. In fact, it reached its highest level since 2022. This is good news for global growth. Nevertheless, behind this strong performance at the global level lie dynamics that are not necessarily indicative of a lasting continuation of this favorable trend.

According to most surveys, manufacturers report that a significant portion of the acceleration in activity has stemmed from precautionary stockbuilding. Companies appear to have brought forward orders in order to anticipate further cost increases amid the current crisis and, above all, to try to avoid potential supply shortages in the coming months.

As a result, if the crisis were to persist, a sharp slowdown in activity could materialize fairly quickly.

At the same time, it should be emphasized that part of this industrial momentum is also linked to the continued remarkable dynamism of sectors related to the development of artificial intelligence. This is clearly the case in the United States, but also in several Asian countries, notably South Korea and Japan. That said, an energy crisis that drags on for too long could also begin to weigh on the momentum of this sector. At this stage, however, it remains a key source of support for activity.

Finally, one of the most notable findings of the survey is, of course, the continued rise in input costs, which represents a negative factor for future growth.

Euro area: Growth holds up in Q1 2026, but the slowdown is intensifying despite solid industrial activity

Growth holds up in the euro area in Q1 2026

GDP growth in the euro area proved relatively resilient in the first quarter of 2026. Excluding the highly volatile evolution of Irish GDP, the euro area economy expanded by 0.2% over the quarter.

However, looking at the major economies reveals contrasting developments. While growth in Spain remained very robust, France disappointed with stagnant GDP growth, driven mainly by a negative contribution from foreign trade.

Growth holds up in the euro area in Q1 2026

The good news came from the industrial sector, which has maintained strong momentum. However, according to survey details, a large part of the acceleration in activity can be explained by strong corporate demand driven by expectations of further cost increases and, above all, by fears of potential supply shortages in the coming months. In this sense, momentum could fade fairly quickly if there is no rapid resolution to the current crisis.

In fact, it is in the services sector that the effects of rising energy prices and declining confidence are most visible. This is what the PMI surveys for services, due to be published tomorrow, are expected to confirm.

The prolongation of the energy shock has led us to lower our euro area growth forecast for the year once again.

United States: The economy is still holding up, but the energy shock is set to start weighing on activity

GDP growth held up in Q1 2026

As expected, U.S. GDP growth held up in the first quarter of 2026, recording 2% growth on an annualized basis. Beyond the rebound in public spending, which offset the effects of the Q4 2025 “shutdown,” consumption—despite slowing—continued to support growth, and above all, investment in the technology sector made a strong contribution to overall economic growth.

A significant contribution from technology investment

The most striking development at the start of this year has been a renewed acceleration in spending in areas related to artificial intelligence (AI). These expenditures have been rising very rapidly, as evidenced by the announcements made by major technology groups in their earnings releases for the first quarter of 2026.

Industrial activity is holding up well

The ISM survey on manufacturing activity came in very strong. The technology sector played a supportive role, as did new orders, which—despite a slight decline—remain robust. As in Europe, companies also appear to have anticipated potential further cost increases linked to the crisis, as well as possible shortages. Nevertheless, it does seem that U.S. manufacturing is holding up better than elsewhere, also supported by tax incentives for investment.

Consumption could weaken in the coming months

One of the key questions looking ahead, in the context of the energy shock, is whether consumers will continue to hold up. We believe that household spending is likely to slow more markedly in the coming months in response to rising costs. In addition, we think that the decline in the savings rate is reaching its limits and that, with rising interest rates in particular, the savings rate should rebound somewhat, thereby contributing to a slowdown in consumption.

Sebastian Paris Horvitz

Director of Research