The market sees the glass as almost full

Link

What should we take away from market developments on may 29, 2026?

Insights from Xavier Chapard.

Overview

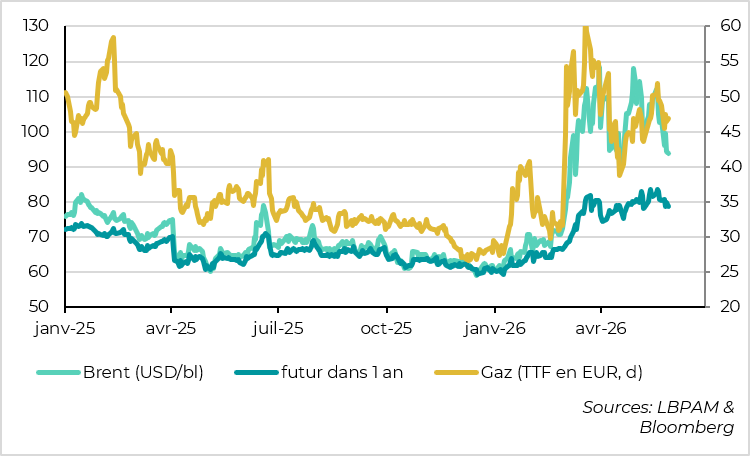

► Energy prices fell sharply this week and have returned to their levels from the beginning of the mid-May ceasefire, with oil now well below $100 after exceeding $110 earlier in the month. Talks between the United States and Iran are ongoing and progressing according to both sides, but without any concrete breakthrough and without preventing “defensive” strikes.

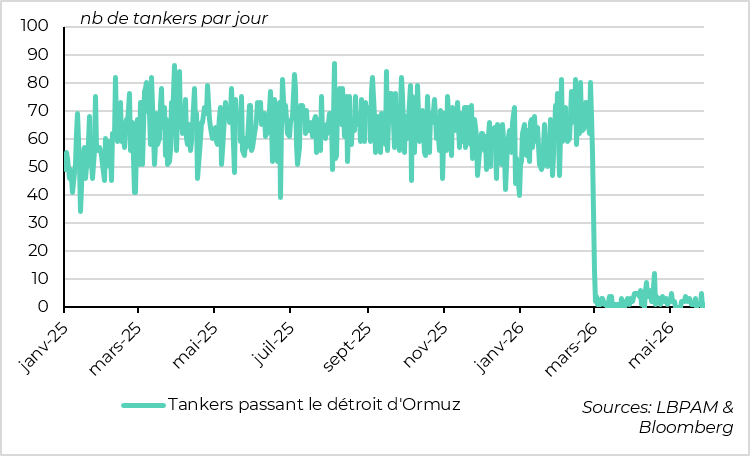

►Given the near-total blockage of the Strait of Hormuz for the past three months, removing around 10% of global oil (and gas) supply, the price shock has been surprisingly contained. In our view, this reflects (1) optimism that a resolution will be found quickly, and (2) the fact that inventories (U.S. and Chinese for oil, European for gas) have so far significantly cushioned the supply shock.

►This is positive in the sense that we remain in our central scenario, which dampens but does not derail the global economic and financial cycle, despite a longer-than-expected disruption in the Strait of Hormuz.

However, this does not mean that the risk of a much more adverse scenario has diminished, as the ability of inventories to decline will become limited as early as this summer, and optimism about a resolution of the conflict remains fragile given the lack of visible progress on the many sticking points in the negotiations.

► After the continued market rebound this week, our relatively optimistic scenario is now fully priced in. This limits short-term upside potential and increases the risk of a correction should our adverse scenario materialize. Under these conditions, we believe it is prudent to move to a neutral positioning on risky assets.

► In the United States, consumption remains resilient thanks to the labor market and wealthier households, but it is weakening under the impact of inflation, which is weighing on real incomes. This should keep growth below 2% by mid-year.

On the price side, inflation accelerated slightly less than expected in April, but the Fed’s preferred measure still rose to 3.3%, a high since 2023. With inflation remaining more than one percentage point above target and risks to employment contained, we believe the Fed will keep rates unchanged and adopt a neutral stance in June, despite the arrival of its new chair.

►In the euro area, the European Commission’s May survey stabilized after two sharp declines, suggesting that activity is slowing markedly but not collapsing in Q2. This is somewhat reassuring after the sharp drop in the PMI in May, particularly for France, even though risks remain tilted to the downside in the coming months.

At the same time, companies report that the increase in their selling prices did not accelerate further in May despite rising costs, suggesting that second-round effects from the energy shock on inflation should be more limited than in 2022. Under these conditions, we still believe that the ECB could adopt a more neutral tone after the expected rate hike in June.

Going Further

Global: PMIs broadly stable in April, with regional differences

Global: The energy shock is less abrupt so far, but risks remain

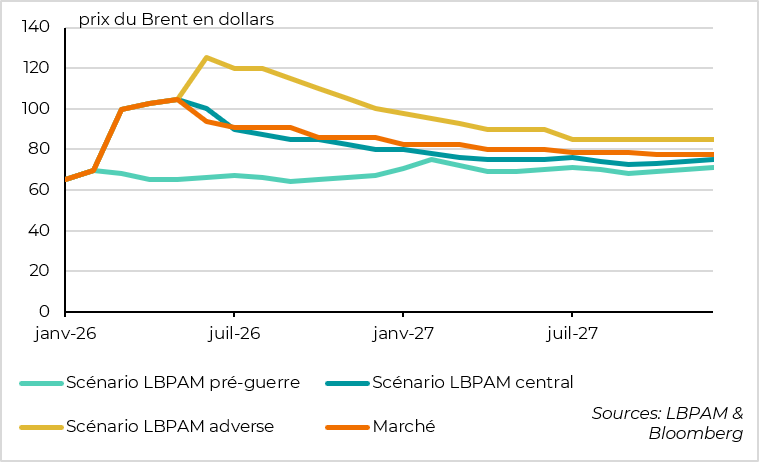

The price of oil has fallen back below $100 per barrel over the past week, supported by hopes surrounding negotiations between the United States and Iran. It is now at its lowest level since the early days of the mid-April ceasefire, after having climbed back above $110 earlier in the month.

That said, prices remain $25 above their pre-conflict levels, and one-year oil prices are still $15 higher than before the crisis. Gas prices are following a fairly similar trend.

If we were to stop there, the energy shock would be significant but not decisive, both for inflation (a temporary shock of around 0.75 percentage points year-on-year) and for growth (around -0.3 percentage points).

However, the blockage of the Strait of Hormuz continues to significantly reduce energy supply

However, despite reports of a few tankers getting through, the Strait of Hormuz remains almost completely closed, meaning that around 10 million barrels per day are missing from global oil supply (~10%).

While hopes of a reopening in the coming weeks remain (our central scenario), the risk of a prolonged supply shock is significant. Given the scale of the disruption, one might have expected a much stronger price shock in both oil and gas.

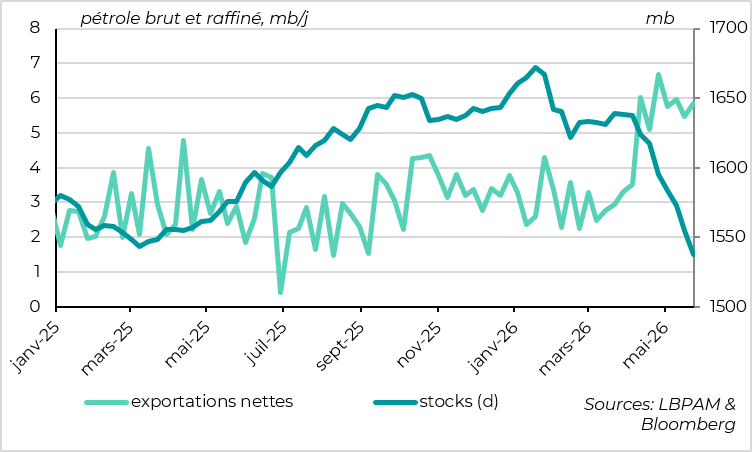

The United States have significantly increased their exports by drawing on their inventories

Beyond hopes of a relatively quick resolution, the relatively contained reaction of energy prices likely reflects larger-than-expected adjustments in flows over the past two months. However, these adjustments are unlikely to be sustainable beyond a few weeks.

On the supply side, the United States have increased their oil exports (both crude and refined) by nearly 3 Mb/d since the start of the war. This offsets a significant share of the lost supply from the Middle East. However, since U.S. oil production has remained stable, this increase in exports has come from a drawdown in inventories, particularly strategic reserves and gasoline stocks.

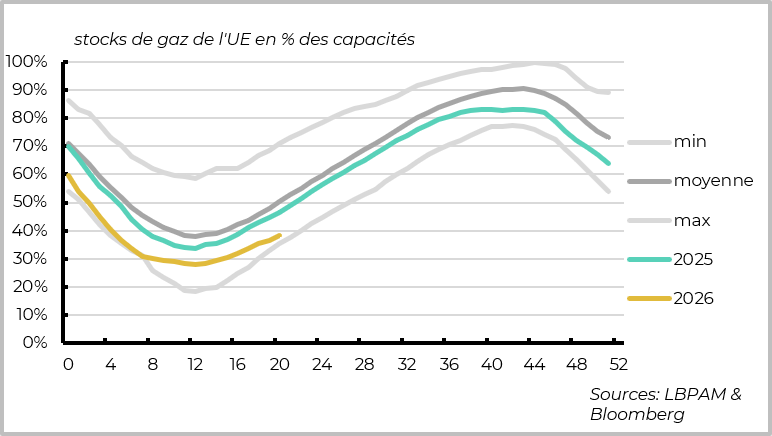

Europe is delaying the rebuilding of gas inventories

On the demand side, China reduced its oil imports by 2.5 Mb/d in April compared with the previous month. Consumption likely declined somewhat, especially in highly oil-intensive industries, but not to that extent. China’s large oil inventories therefore appear to have absorbed the difference.

As for gas, Europe has not yet begun restocking in preparation for next winter, as is usually the case at this time of year. This is helping to ease short-term pressure on gas prices, but it increases the risk that purchases will need to accelerate this summer, even if prices remain elevated.

The market is now pricing in our favorable scenario

Overall, market energy prices have returned in line with our central scenario, even though energy supply from the Middle East remains significantly reduced for longer than we had anticipated. This is positive in the sense that the negative shock to growth and inflation is meaningful, but still not large enough at this stage to derail the global economic and financial cycle.

That said, the risk of a more adverse scenario remains significant if the Strait of Hormuz does not reopen quickly, as the ability of inventories to offset the loss of supply is becoming increasingly limited, or if confidence in a swift resolution to the crisis deteriorates. In such a case, energy prices could rebound to new highs and remain elevated for longer, which would weigh on the global outlook.

As markets are now pricing in our relatively favorable central scenario, this limits the short-term upside potential for risky assets. At the same time, the risk that our adverse scenario (i.e., Hormuz remaining blocked through the summer) materializes is still very present, which could trigger a significant correction. Under these conditions, we believe it is appropriate to adopt a more neutral stance on risk in portfolios.

United States: consumption remains resilient but is weakening due to inflation

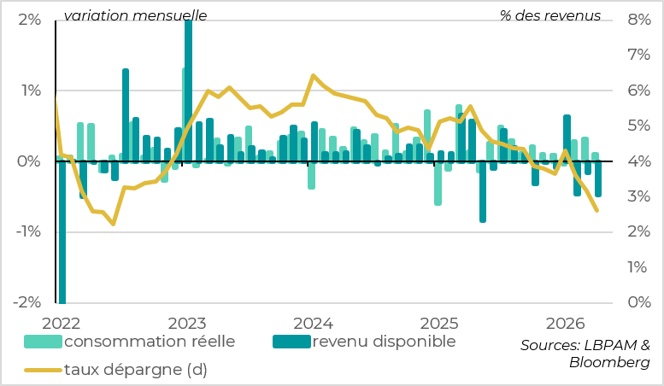

Consumption remains resilient despite the decline in households’ real incomes

Q1 growth was revised slightly lower in the second estimate, from 2.0% to 1.6%, partly due to consumption, which grew by only 1.4% over the quarter (down from an initial estimate of 1.6%). This confirms the slowdown at the turn of the year, even though the revision mainly reflects a weaker contribution from inventories (a volatile component), while final private domestic demand remains solid (2.4%), supported by strong corporate investment (particularly related to AI).

At the start of Q2, consumption is still holding up, rising by 0.1% in April after a strong 0.3% increase in March. This leaves a positive carry-over for the quarter, at 1.7%. However, consumption momentum is slowing on a monthly basis, especially for essential spending (i.e. by lower-income households), suggesting that a growing share of households is facing tighter budget constraints.

This is consistent with income data, which stagnated in nominal terms in April and, due to inflation, declined for the third consecutive month in real terms (-0.5% in April). The savings rate therefore fell again, from 3.2% to 2.6% in April, reaching its lowest level since the post-Covid rebound and the 2022 energy shock.

Under these conditions, we expect consumption to slow somewhat further around mid-year, although still favorable wealth effects should continue to support spending among higher-income households.

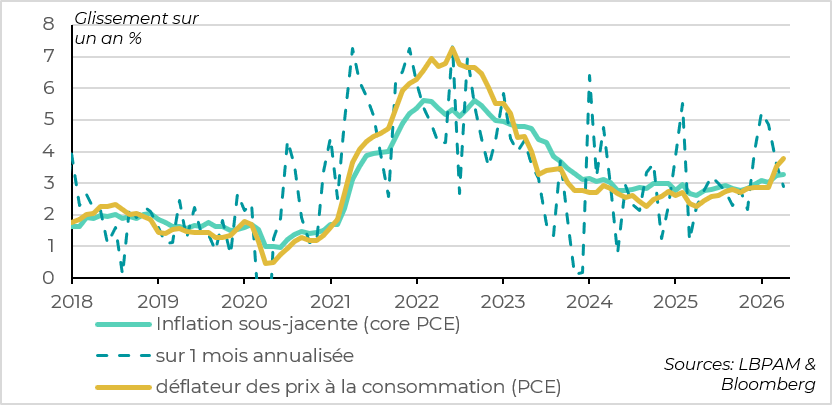

Inflation accelerated as expected in April

On the price side, the consumption price deflator accelerated as expected in April, driven by energy prices, rising from 3.5% to 3.8%, its highest level since 2022. This is weighing on households’ purchasing power.

Beyond that, the Fed’s preferred inflation measure, the core deflator excluding energy and food, also edged up slightly, from 3.2% to 3.3%. In fact, core price increases in April were somewhat less strong than feared (+0.2%), particularly in categories that best reflect domestic pressures (i.e. services excluding rents). This is somewhat reassuring after several upside surprises, as it suggests that inflation momentum is not deteriorating further.

However, for the Fed, the fact that underlying inflation has reaccelerated to a two-year high and remains more than one percentage point above target this year means it cannot lower its guard against inflation risks. This is especially true as recent labor market data (jobless claims, consumer confidence) suggest that risks on that side of its mandate remain contained. Under these conditions, we believe the Fed will keep rates unchanged this year and adopt a neutral communication stance regarding the future path of rates in June.

Euro area: activity is slowing markedly in Q2, but not collapsing for now

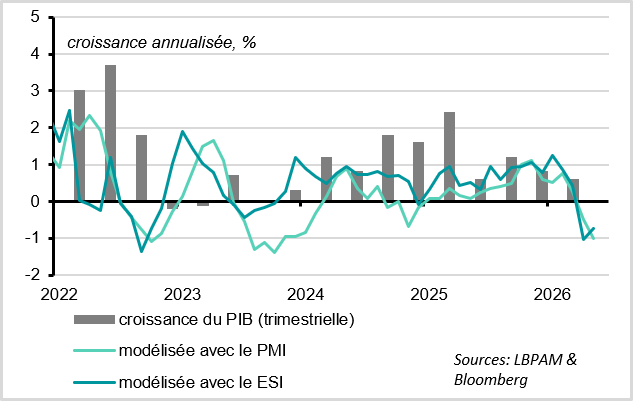

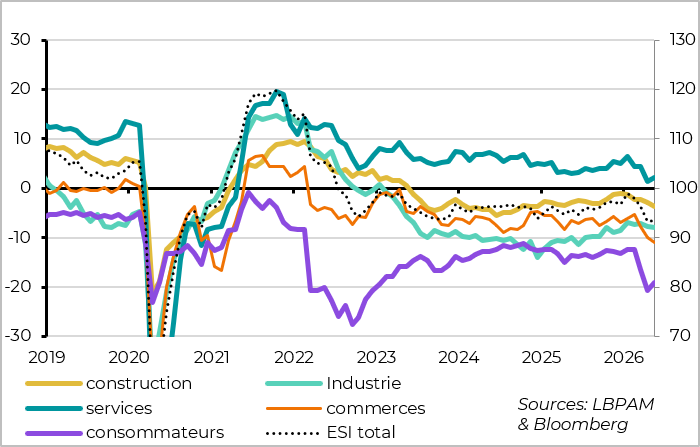

The Economic Sentiment Indicator stabilized at a low level in May

The European Commission’s Economic Sentiment Indicator stabilized in May after two sharp declines, rising from 93 to 93.5 points. This is somewhat more reassuring than the PMI, which fell sharply again in May, although both of the main surveys for the euro area point to a slight decline in activity in Q2 (around -0.2% quarter-on-quarter according to our estimates).

Sentiment has been declining mainly among households, retail, and services over the past three months

The slight rebound in the indicator in May was driven by improved confidence in services and among consumers, both of which had fallen sharply since the start of the war and remain at depressed levels. As in the PMI survey, industrial sentiment is holding up somewhat better, even though it also declined in May. The same applies to construction (which is not covered by the PMI survey), while retail continues to deteriorate sharply.

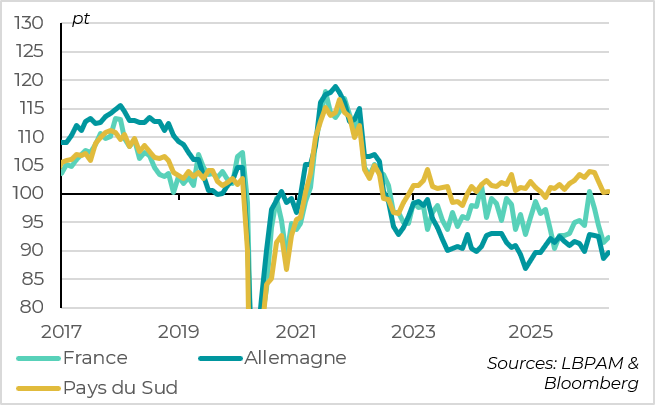

Economic sentiment stabilized across all countries in May

From a country perspective, the European Commission’s survey somewhat tempers the very negative signal sent by the PMI surveys for France, but confirms that the energy shock is calling into question the expected rebound in the German economy, despite the sharp increase in public investment.

Indeed, economic sentiment has declined markedly in France since the start of the war, but it stabilized in May, as elsewhere, and is not as weak as the French PMI (43.5). For Germany, both the Commission’s indicator and the PMI have stabilized at levels consistent with stagnant activity.

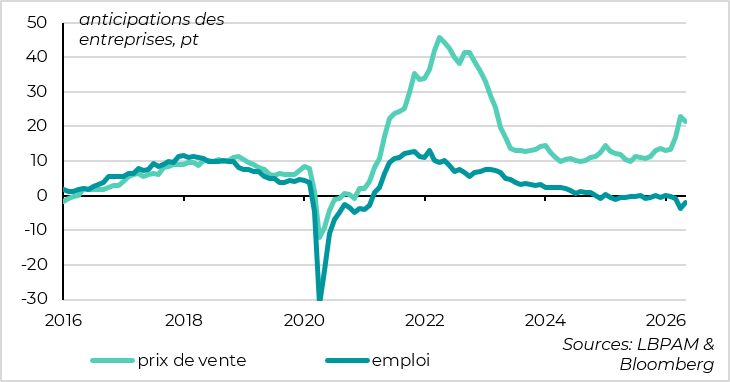

Companies expect somewhat smaller increases in their selling prices in May

For the ECB, the survey confirms the weakening of the real economy and the labor market, even if it appears less abrupt than recent data had suggested. More importantly, it confirms that cost pressures have increased, but that companies are finding it more difficult to pass them on to their selling prices than in 2022, particularly in services.

This should provide some reassurance to the ECB, which could opt for a less committal tone regarding its future decisions after the much-anticipated rate hike in June. We continue to believe that the negative impact on the economy and the limited second-round effects on inflation should lead it to stop after a single rate hike this year, at least if the energy shock does not intensify further.

Xavier Chapard

Strategist