The path to peace seems to be narrowing

Link

What are the key takeaways from the market news on April 7, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► Yesterday, President Trump stated that today at 8 p.m. was the deadline for Iran to comply with U.S. demands, including, in particular, the reopening of the Strait of Hormuz. Beyond that point, the United States would launch a massive attack on the country’s energy infrastructure.

The Iranian authorities, through Pakistan, have so far responded negatively to the U.S. demands. They consider that there can be no ceasefire without security guarantees for the country, without the lifting of sanctions, and without reconstruction aid.

►We therefore remain at an impasse. However, President Trump’s extremely bellicose statements over the weekend are once again creating risks of escalation, further distancing any prospects for peace. This has therefore kept markets under tension, starting of course with the oil market, where the price per barrel remains close to 100 dollars. This is all the more true as the bombings have continued in Iran, while the latter continues to target the region’s energy infrastructure.

In addition, the American president seems reluctant to heed calls for de-escalation from allied countries as well as from China.

►Crucially, the Strait of Hormuz remains closed. Even though around twenty ships were able to pass over the weekend (mostly Iranian), this is negligible compared with the 135 vessels that passed through each day before the war.

As long as the strait remains closed, prices will stay very high, with risks of hydrocarbon shortages in certain regions, particularly in some Asian countries.

►We still maintain, as our central scenario, that the crisis will be resolved soon. However, it is clear that the probability of a very negative alternative scenario has increased. In such a scenario, with the war dragging on, oil prices would remain high (or even much higher than they are today), posing a significant risk of undermining global growth and pushing inflation to levels far above current expectations.

►In this environment, we remain tactically very cautious in our asset allocations, but in line with our central scenario, we still maintain a constructive outlook for the rest of the year despite the fog of war.

►Beyond the risks that this war poses to the economic outlook and to the persistence of lasting geopolitical tensions in the Middle East and around the world, a first consequence linked to geopolitical instability has come from the United States, with President Trump requesting that Congress approve a 2027 defense budget of 1.5 trillion dollars, representing an increase of more than 40%. The proposal would be accompanied by significant cuts to government social spending. At this stage, long-term U.S. interest rates have not reacted much, but the risk of seeing public deficits become even larger than expected is increasing.

►We have already seen the first scars of the war on economies, starting with rising inflation, itself driven by higher energy prices.

In contrast, activity data have delivered mixed signals. This is partly normal given the recent outbreak of hostilities.

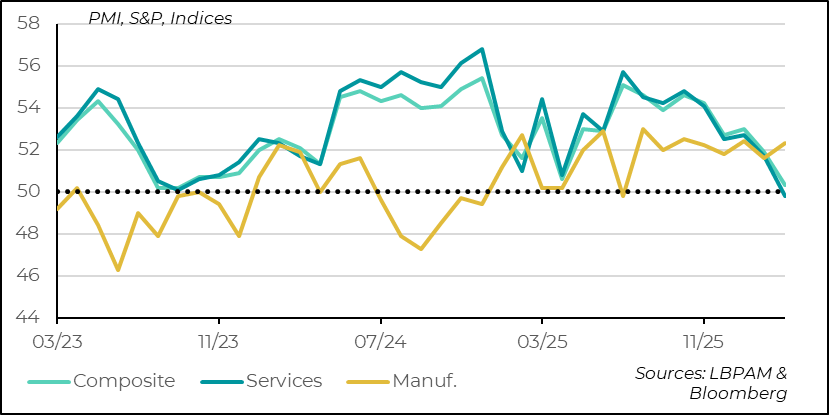

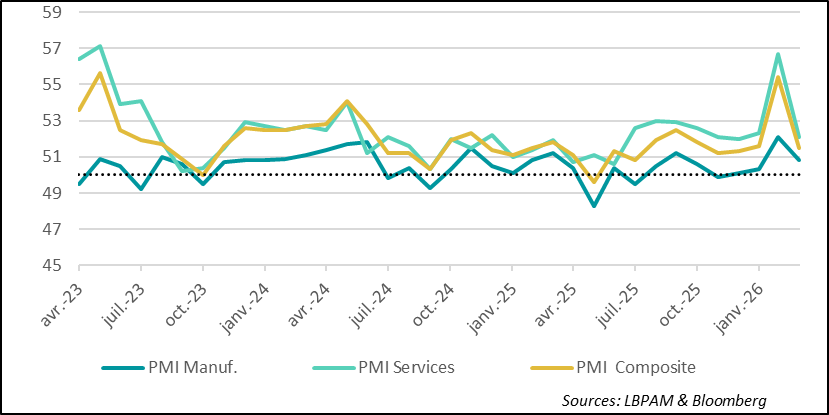

However, the March S&P PMI surveys — both for manufacturing and the first releases for services — show that the most significant impact to fear is on confidence.

Thus, almost everywhere, business confidence in future prospects has declined.

►In the United States, while activity in the manufacturing sector appeared rather resilient in March according to the S&P PMI survey, the situation was much more disappointing in the services survey. Indeed, for the first time since January 2023, activity in the sector is believed to have contracted.

The main reason cited by firms was the consequences of the war, particularly rising costs.

Most importantly, confidence in future prospects fell to its lowest level in five months.

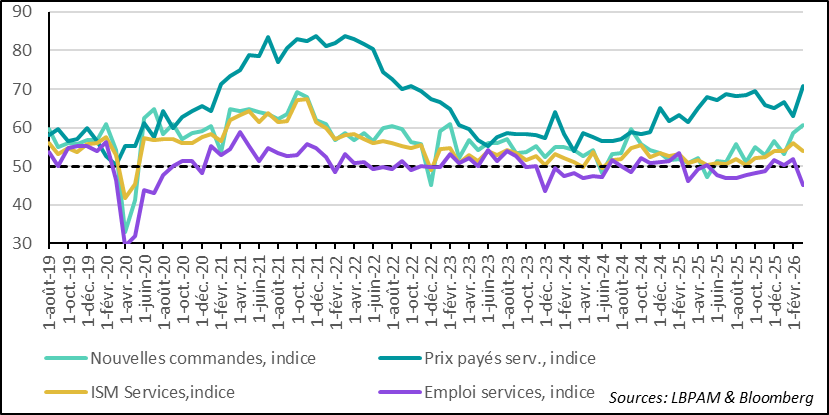

Rising costs were also visible in the ISM services survey. However, that survey delivered a slightly less negative message regarding activity in the sector: although it showed a slowdown, it did not point to a contraction.

Nonetheless, the employment indicator fell sharply, likely reflecting concerns about future prospects.

►At the same time, the March employment report in the United States came out much more positive than expected. Net job creation far exceeded forecasts, with 178,000 jobs added, partially offsetting the job losses (revised to 133,000) from the previous month.

Also important for monetary policy, the unemployment rate fell back to 4.3%. This remains consistent with a Federal Reserve that is likely to keep its policy unchanged in the coming months.

►In China, despite the greater resilience we expect from the economy in the current context, it is worth noting that the March S&P (RatingDog) PMI surveys — both for services and manufacturing — turned out to be somewhat disappointing. They seem to indicate that the strong momentum seen at the beginning of the year has slowed, particularly in the services sector.

This remains consistent with our projection that growth should hold up over the year (remaining within the new official range of 4.5–5.0%), but without a strong acceleration.

Growth should continue to be supported by investment, especially in technology, and by exports.

Going Further

United States: Activity still appears to be holding up, even though the effects of the war are becoming more visible

The S&P services PMI survey shows the first negative effects of the war

The S&P services PMI survey for March delivered a rather negative message regarding the impact of the war on activity. Indeed, the composite index fell back below 50, moving into contraction territory for the first time since January 2023. According to the survey, rising costs — mainly energy-related — appear to be weighing on demand, while the uncertainty created by the war, combined with government policies, particularly tariff measures, is affecting business confidence.

The survey highlights the concerns we had about the negative dynamics that this geopolitical crisis could trigger for the U.S. economy, which had so far been performing well. In particular, confidence in future prospects declined, reaching its lowest level in five months.

As we have emphasized repeatedly, it is crucial that the energy shock and the accompanying uncertainty dissipate quickly in order to avoid a more lasting negative effect on the economy. At the same time, caution is needed when interpreting data during such a highly disrupted period. Indeed, contradictory signals from the United States persist, sometimes offering a more positive view of the economic outlook. For example, the S&P manufacturing PMI for March came in somewhat more favorable, despite the sharp rise in costs.

The ISM services survey provides a less negative assessment of the sector’s momentum

The ISM services survey for March delivered a less negative message regarding the sector’s cyclical momentum. Although the index declined compared with the previous month, it remained in expansion territory. Most importantly, in terms of future dynamics, new orders rose sharply during the month, reaching their highest level since February 2023.

Unsurprisingly, the most notable element of the survey was the strong rise in costs. The prices-paid index reached its highest point since October 2022. This is, of course, a challenge for businesses, and at this stage it is difficult to assess how much of these cost increases can be passed on to customers and ultimately reflected in consumer prices.

The unemployment rate declines in March

The good news regarding the state of the U.S. economy came from the labor market. Indeed, the March employment report was much more favorable than expected, with job creation — according to the establishment survey — far exceeding forecasts (178,000 compared with 65,000 expected).

Most importantly, the unemployment rate fell back to 4.3%. However, this decline was partly due to a drop in the participation rate.

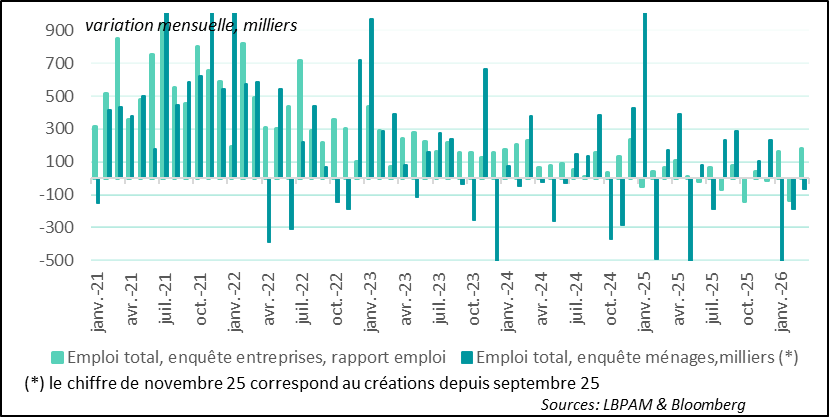

Household and business surveys point to different dynamics

This decline in participation, as estimated using data from the household survey, reflects people leaving the labor market. In addition, this survey shows that job losses occurred during the month. It should nevertheless be noted that this survey is much more volatile than the establishment survey.

The healthcare sector remains the largest creator of jobs

The establishment survey also brought good news regarding job creation, indicating that a majority of sectors added jobs over the past month. At the same time, the figures include a distortion linked to the end of the strike that had affected part of the healthcare workforce (this had subtracted more than 30,000 jobs from the February figures).

Meanwhile, despite the rebound in job creation following the sharp contraction in February (–133,000), two sectors continue to be the largest contributors to payroll growth: leisure and healthcare. The latter is in fact the only sector that has exceeded its pre‑Covid employment level. This largely reflects a structural trend driven by population aging.

By contrast, in manufacturing, even though 15,000 jobs were created in March, a total of 82,000 jobs have been lost since President Trump took office.

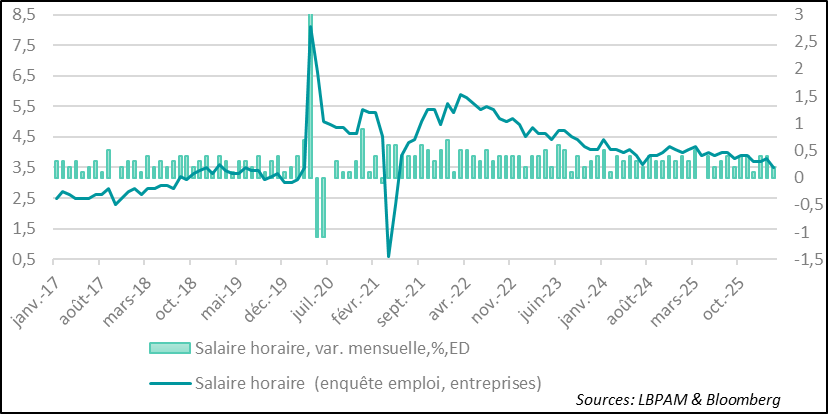

Wages are decelerating

The survey also revealed that despite strong job creation during the month, wage pressures actually eased, with hourly earnings rising by only 0.2% on the month, or 3.5% year‑on‑year, well below the 3.8% recorded the previous month.

This seems to indicate that, despite a labor market still close to full employment, wage pressures are not really present. This appears consistent with a situation in which weakening activity reduces workers’ bargaining power. Even if these figures will be viewed favorably by the Federal Reserve, other measures of wage growth will be needed to obtain a more reliable picture.

Overall, even though the first negative marks of the war are appearing in some economic indicators, it still seems that activity in the United States remains resilient.

China: PMI surveys show a weakening of the early‑year growth momentum

The Chinese economy appears to be losing the momentum it showed at the beginning of the year

The S&P (Ratingdog) PMI surveys for March turned out to be far more disappointing than expected. Thus, following the slowdown in manufacturing, the services survey delivered an even more disappointing message, erasing almost all of the previous month’s rebound. Nevertheless, activity continues to expand.

On a more positive note, the survey shows that firms remain optimistic about future prospects. Another important message was that growth was clearly supported by domestic demand, which could indicate that consumption remains well oriented.

At the same time — and this is one of the factors that should support the Chinese economy — it appears to be more shielded from rising energy costs. Indeed, in the survey, cost increases remained very moderate during the month, in contrast with what has been observed in Europe or the United States.

Our projection for the Chinese economy remains GDP growth within the authorities’ 4.5–5.0% range. Although the growth strategy still relies on investment — particularly in the technology sector — and on exports, we believe that targeted measures to support consumption will be implemented during the year in order to meet the growth targets.

Sebastian Paris Horvitz

Director of Research