The risk of more restrictive monetary policies could weigh on markets

Link

What are the key takeaways from the market news on June 09, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► An agreement between the United States and Iran is still not in sight, resulting in the continued blockage of the Strait of Hormuz. At the same time, the United States has managed to break a re-escalation dynamic, following an exchange of attacks between Israel and Iran. Overall, discussions are ongoing to extend the ceasefire and reopen the Strait of Hormuz.

►The continued halt in the transport of energy products from the Persian Gulf is keeping prices elevated, although still well below recent peaks. As is well known, the longer normalization takes, the higher the economic cost will be.

►The measures put in place to contain the rise in oil prices are reaching their limits, with oil inventories already experiencing a sharp decline. Moreover, OPEC’s decision to increase oil production (+188 thousand barrels) in July is unlikely to address the current production shortfall.

►In the meantime, rising energy costs are expected to continue spreading through the global economy, acting as a drag on economic activity.

►The euro area remains one of the most affected regions, with gas prices still elevated (+60% compared to pre-conflict levels). These price pressures also reflect historically low inventory levels. As is well known, GDP is likely to contract in Q2 2026, following solid resilience in Q1 2026 (+0.2% excluding Ireland). The energy shock is acting as a headwind for European equities, as the ECB prepares to raise its rates.

►However, for now, this shock has not had as significant an impact on the US economy. On the one hand, the strong momentum driven by substantial investments in AI is supporting growth. These investments are also backed by significant public subsidies. On the other hand, consumption remains resilient. The negative impact of higher energy prices on purchasing power has been offset by public transfers and a solid labor market.

Indeed, the US employment report for May came in well above expectations, with 172 thousand jobs created, nearly double what had been anticipated. Moreover, the unemployment rate remained stable at 4.3%.

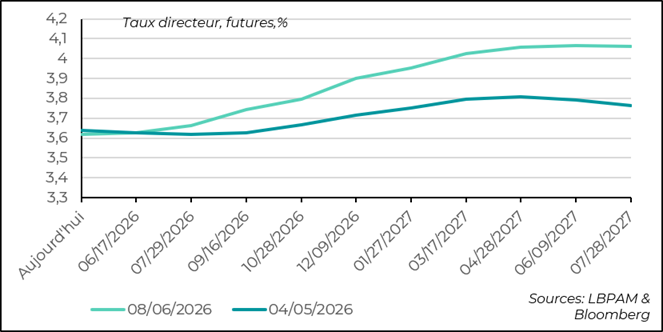

►The strength of the labor market, while inflation data clearly show upward pressure on prices, has led to a significant reassessment of monetary policy expectations in the market. Indeed, the market now expects a rate hike by the end of the year and a possible additional increase in 2027, compared with none just one month ago.

►We have long maintained that the Fed would remain cautious and did not anticipate rate cuts in 2026. It must be acknowledged that the US cyclical environment, incorporating fiscal stimulus, the energy shock, and spending on AI, is complicating the Fed’s position. The risk of a hike in policy rates has clearly increased.

►K. Warsh is likely to have a challenging start as head of the Fed, as he will need to demonstrate the Fed’s independence by maintaining at least a slightly restrictive policy, without yielding to President Trump’s calls to lower interest rates.

►However, it should be noted that, although we maintain the view of a resolution of the conflict, even if only partial, with a full reopening of the Strait of Hormuz, the possibility of a tightening of monetary conditions in the coming months would be an unwelcome headwind for risk assets.

►However, it should be noted that, although we maintain the view of a resolution of the conflict, even if only partial, with a full reopening of the Strait of Hormuz, the possibility of a tightening of monetary conditions in the coming months would be an unwelcome headwind for risk assets.

Going Further

United States: The labor market continues to strengthen, pushing the Fed toward greater caution

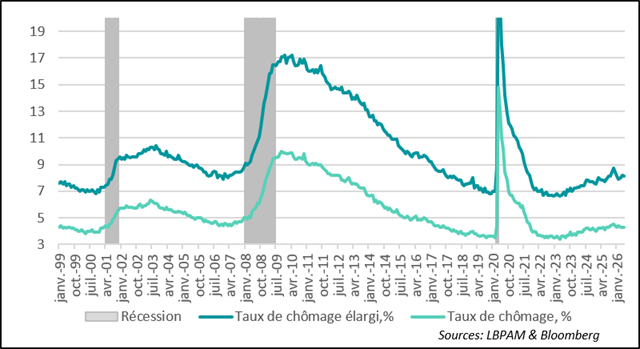

The unemployment rate remains low and stable in May

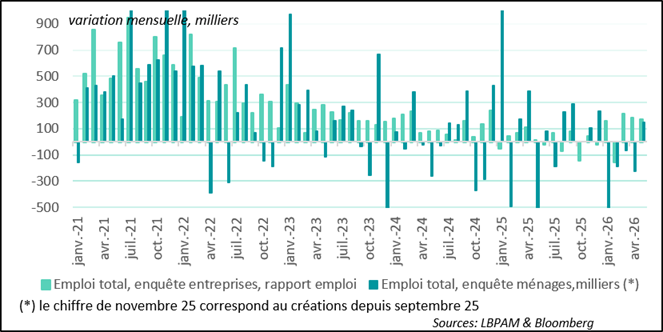

The May employment report surprised significantly to the upside, with job creation coming in at twice the expected level, totaling 172 thousand net new jobs. Moreover, the unemployment rate remained stable at 4.3%. This positive momentum is part of a rebound in job creation over the past three months. Indeed, job gains for the previous two months were revised upward.

An increase in employment in both the household and establishment surveys

Unlike in previous months, both the establishment and household surveys showed an increase in job creation. Moreover, the household survey, which is used to calculate the unemployment rate, indicates that the number of new entrants to the labor market was relatively high, but was largely offset by job creation. This explains the stability of both the participation rate (61.8%) and the unemployment rate.

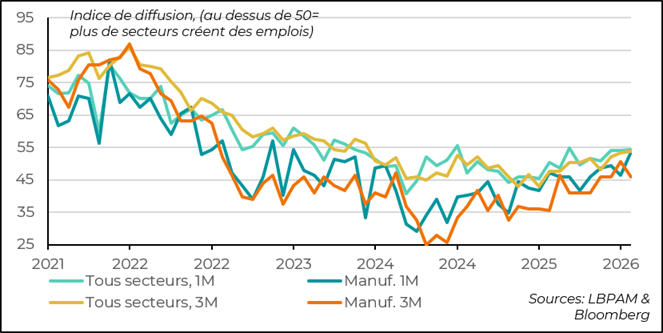

La majorité des secteurs créent des emplois sur le dernier mois

Moreover, the statistical office publishes a so-called diffusion index to assess the breadth of job creation across the economy. Thus, over the past month, the majority of sectors contributed to employment growth. This is encouraging, although this performance remains somewhat below the historical average.

It is in the industrial sector that the recovery in hiring is slower, as indicated by the diffusion index when measured over a three-month period.

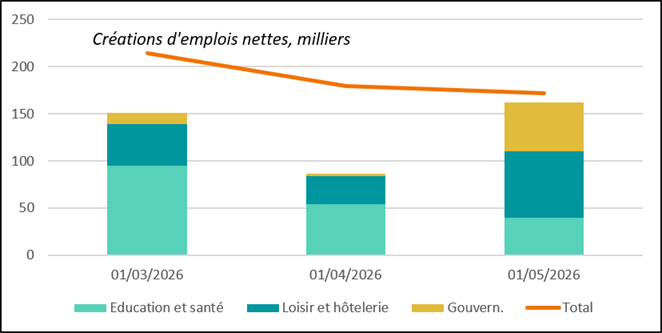

Some sectors continue to make a very strong contribution

At the same time, some sectors continue to be major contributors to job creation. This is notably the case in healthcare and leisure, particularly in the restaurant industry. Healthcare remains by far the main driver of employment, reflecting growing needs for personal care services due to an aging population.

Moreover, local governments made a strong contribution to job creation over the past month.

It is worth noting that the report does not show any significant signs of job destruction linked to the development of AI.

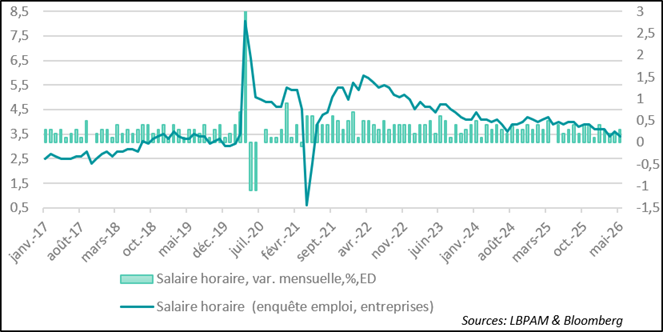

Wage pressures remain contained

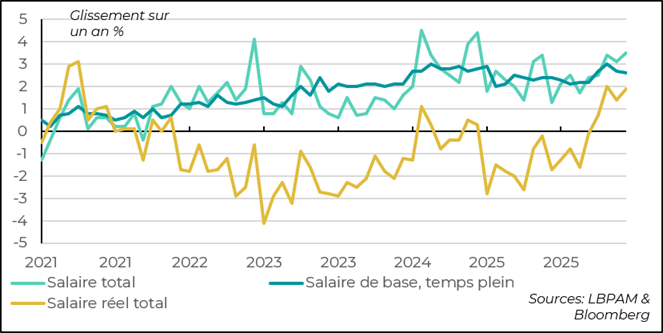

Regarding wages, the establishment survey shows that pressures remain contained, with wage growth slowing to 3.4% year-on-year. This is below the rate of inflation, indicating, based on this measure, that the inflation shock is eroding household purchasing power. Nevertheless, continued job creation is helping to mitigate the impact of this shock on consumption.

A sharp revision of the Fed’s rate hike expectations

One of the key consequences of this relatively strong employment report for the US economy has been a marked revision of expectations for policy rate hikes in the coming months. In particular, the market now expects a rate hike in 2026 and is close to pricing in a second one in 2027.

With inflation likely to remain elevated and the labor market recovering, the Fed will need to maintain a somewhat restrictive bias in the months ahead. For now, we maintain our long-held view that the Fed should keep its policy unchanged in the face of the inflation shock. However, it is clear that the likelihood of a rate hike is increasing, at least as a precaution, to ensure that inflation expectations remain well anchored.

The first monetary policy meeting to be chaired by K. Warsh, the new Fed Chair, will be a real challenge. Indeed, he will need to demonstrate the Fed’s independence and likely adopt a firm tone on inflation, while clearly resisting calls from President Trump, who would like policy rates to be lowered.

Japan: The BoJ is expected to raise its policy rates

Wages

Wage developments in Japan have provided further justification for the BoJ to continue normalizing its highly accommodative monetary policy. Indeed, total wages increased by 3.5% year-on-year in April, well above expectations. Base wage growth, a key metric closely monitored by the central bank, remained stable at 2.6% compared to the previous month.

However, with the government’s implementation of price controls, particularly on energy, which is restraining inflation, real wage growth has been very strong, rising by 1.9% year-on-year.

This should continue to support consumption, which was one of the drivers of GDP growth in Q1 2026.

As price controls will eventually have to be lifted, the BoJ will need to incorporate these wage developments into its medium-term inflation outlook. In our view, this should prompt it to act as early as next week, with a 25 basis point increase in its policy rate.

With ongoing depreciation pressures on the currency, this modest monetary tightening should help to ease these pressures.

Clearly, the BoJ will need to strike the right balance in its communication with the government in a still uncertain geopolitical environment in order to proceed with this policy adjustment. We believe this is the right time. A second rate hike will likely be needed by the end of the year.

Sebastian Paris Horvitz

Director of Research