There’s a big gap between theory and practice

Link

What should we take away from market developments on june 05, 2026?

Insights from Xavier Chapard.

Overview

► Trump said this week that a deal with Iran is “in theory” close. At the same time, he said that such a deal could be reached as early as this weekend or in two to three weeks. Meanwhile, the Iranians say there has been no “tangible” progress in the negotiations. Political pressure is rising in the United States after the House of Representatives passed a resolution against the war with the support of four Republicans, even though the vote is only symbolic. At the same time, the United States is announcing a ceasefire agreement between Israel and Lebanon, provided that Hezbollah also stops the fighting.

►Overall, the situation remains unchanged. Both sides are seeking an acceptable way out that would allow the Strait of Hormuz to begin reopening quickly. However, at the same time, the Strait remains effectively almost closed, and the longer the situation drags on, the greater the risk for the economy and, ultimately, for the markets.

►Overall, the situation remains unchanged. Both sides are seeking an acceptable way out that would allow the Strait of Hormuz to reopen quickly. However, the Strait remains effectively almost closed, and the longer the situation persists, the greater the risk to the economy and, ultimately, to the markets.

► As our rather optimistic scenario is already largely priced in, we continue to believe that upside potential is limited and that the risks of a correction are elevated in the event of negative surprises. That said, we remain relatively constructive on markets over a several-month horizon, given the resilience of the economy, the strength of corporate earnings, and the potential for a modest decline in interest rates.

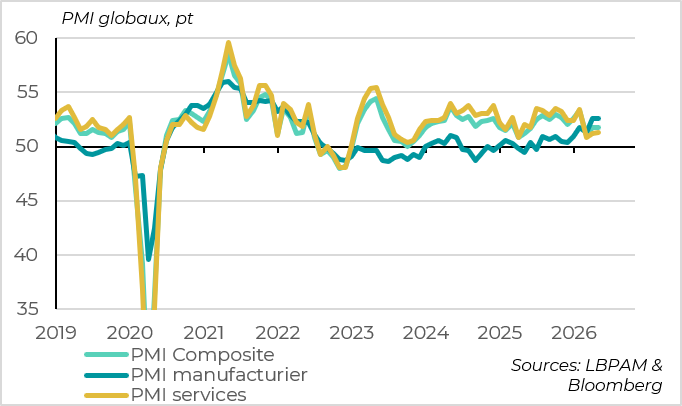

► Macroeconomic data were also rather reassuring this week. The global composite PMI remained stable in May, following a slight rebound in April (at 51.8), signaling only a limited economic slowdown. This positive surprise reflects an unexpected increase in Chinese PMIs as well as a smaller-than-initially-estimated decline in European PMIs. This reduces the risk of a recession this summer.

►In the United States, the strong increases in both the manufacturing and services ISM indices in May, along with the rise in job openings in April, continue to point to resilient economic activity and declining risks in the labor market. At the same time, the ISM price components and Fed surveys indicate that inflationary pressures are still increasing. In this context, we expect the Fed to keep its policy rates unchanged and to remove its easing bias for future rates in June, even though this will be the first meeting chaired by its new president appointed by Trump. That said, the risk of a Fed rate hike still appears limited to us, although it is not negligible.

►In the euro area, inflation increased as expected in May, from 3.0% to 3.2%. However, this rise was driven by a stronger-than-expected increase in core inflation, which accelerated from 2.2% to 2.5%. Although this acceleration in non-energy prices is mainly due to base effects and volatile components, it is likely to reinforce the ECB’s concerns about second-round effects from the energy shock. This makes a rate hike in mid-June almost inevitable and increases the risk of another rate hike this summer (even though our baseline scenario still incorporates only one rate hike this year).

►The European Commission did not single out any country currently under an excessive deficit procedure for its 2026 budget, not even France or Belgium, which are expected to maintain deficits above 5% of GDP this year. It also proposed an additional 0.3 percentage points of GDP in fiscal flexibility this year, providing some room for measures to cushion the energy shock. These decisions were expected but reduce the risk of political tensions over the summer. Despite limited risk premia, we believe that Southern European sovereign bonds offer attractive carry in the short term.

Going Further

Global: growth is slowing but remains resilient, according to May PMIs

The global PMI remains broadly stable in May

The global composite PMI, the best coincident indicator of global economic activity, remained stable in May at 51.8, following a slight rebound in April. This is above its March low (51 at the onset of the war), although still well below its pre-war level (53.3 in February). Overall, the global PMI over the first two months of the quarter is consistent with a continued slowdown in global growth in Q2, albeit a limited one, with growth just below 3% on an annualized basis.

By sector, global PMIs were stable in May in both manufacturing and services. However, after their strong divergence in previous months, this confirms that the shock has not, at this stage, undermined the strong rebound in the goods sector (PMI at 52.6, its highest level in four years), but has significantly reduced growth in the services sector (PMI at 51.3). At least, the latter is no longer deteriorating at the start of Q2.

Still significant regional divergences

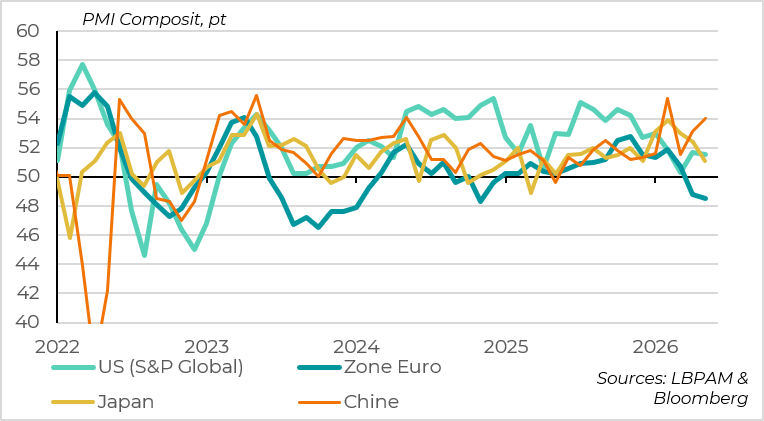

By region, PMIs are mixed but overall reassuring compared to last week’s preliminary releases.

The biggest surprise comes from China’s private-sector PMIs, which rose sharply in May to their highest level in two years (excluding volatility related to the Lunar New Year, at 54). This increase is reassuring after very weak real activity and credit data in April, although official PMIs are less robust (broadly stable at 50.5). Overall, we still expect growth to slow sharply in Q2 but remain broadly in line with the 4.5%–5% target for the year.

What reassures us the most is the revision of European PMIs compared to initial estimates, suggesting that activity is slowing significantly in Q2 but at least not collapsing. The euro area PMI declined again in May and remains in contraction territory (at 48.5), but the decrease was only 0.3 points, compared with 1.3 points initially estimated last week. Similarly, the UK PMI fell into contraction territory for the first time in a year, at 49.7, but the decline was less severe than initially estimated (48.5). This is more consistent with our scenario in which the energy shock leads to stagnation in European growth in mid-year, rather than a recession.

In the United States, S&P Global PMIs ultimately declined slightly in May but remained in positive territory at 51.5, consistent with a relatively moderate slowdown in activity this year.

United States: the Fed constrained by rising activity and inflation

Economic indicators remain solid in May

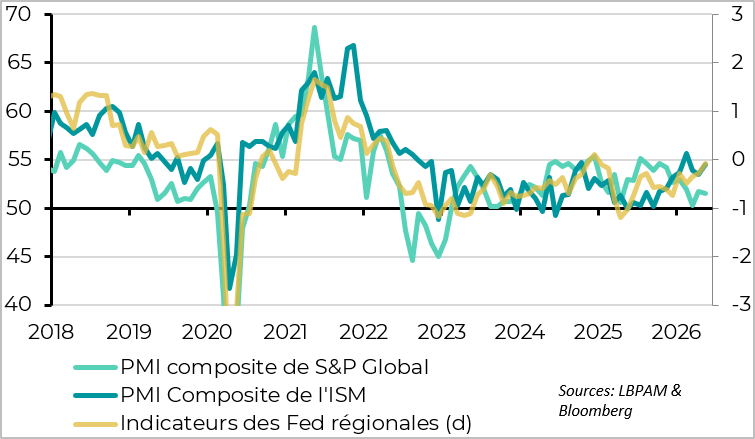

Beyond the S&P Global PMI, which is stable but at a relatively subdued level, ISM indices rose sharply in May in both manufacturing (to 54) and services (to 54.5). This is consistent with the increase in regional Fed indicators over the month and suggests that growth is picking up slightly after slowing to around 1% at the turn of the year.

We expect growth to remain positive but limited this summer, at around 1.5%, due to the decline in households’ real purchasing power. However, leading indicators point to upside risks to this scenario, supported by the boom in investment in AI and a somewhat accommodative fiscal policy.

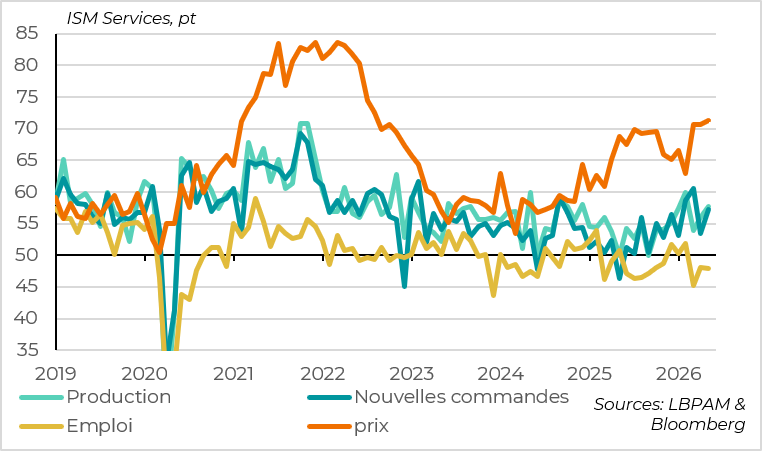

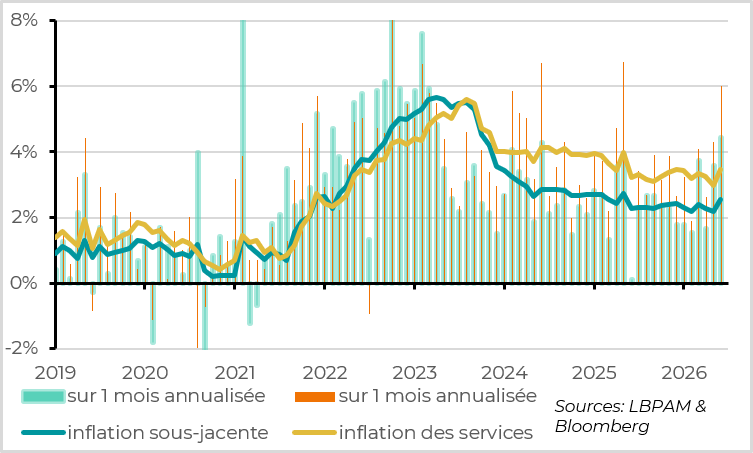

The ISM services index points to resilient demand but rising inflationary pressures

The breakdown of the ISM services index remains fairly strong. The increase in output and new orders suggests that demand remains robust, although the weakness in the employment component and the rise in inventories indicate that companies remain cautious.

At the same time, the ISM services price index rose again in May, reaching its highest level since mid-2022. This confirms that inflationary pressures remain significant, beyond energy-related prices, which increases the risk that inflation may not slow as expected from the summer onward.

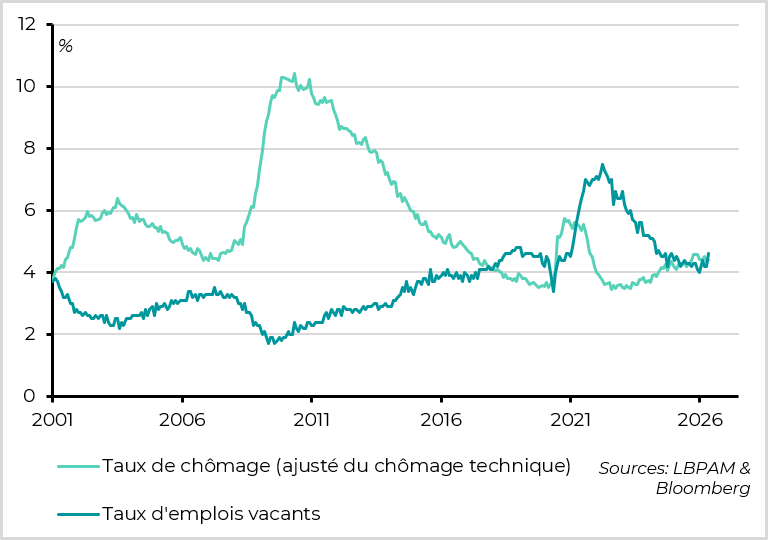

The job openings-to-unemployed ratio rose back above 1 in April

On the labor market side, the employment reports released today will provide further insights, but it would take a very negative surprise to call into question the underlying strength of employment. Indeed, the latest data show that job openings rose back above the number of unemployed in April for the first time in a year, and that private employment picked up slightly in May (122k according to ADP).

These conditions—resilient activity, declining risks in the labor market, but rising inflationary pressures—do not argue for an accommodative Fed. This is all the more so as the Beige Book confirms a slight improvement in activity and a rise in price pressures since the Fed’s last meeting.

This should force Warsh, the new Fed Chair appointed by Trump, to remove the easing bias from the Fed’s communication at his first meeting in two weeks. This is a challenging position for someone appointed by Trump and with midterm elections approaching, but it is justified. That said, unlike the market, we continue to believe that the likelihood of a rate hike this year remains very limited—at least as long as the unemployment rate does not fall back toward 4%, or inflation does not continue to accelerate after the summer (which is not our baseline scenario).

Euro area: the rise in inflation in May seals the case for a rate hike in June

The increase in inflation in May is driven by core inflation

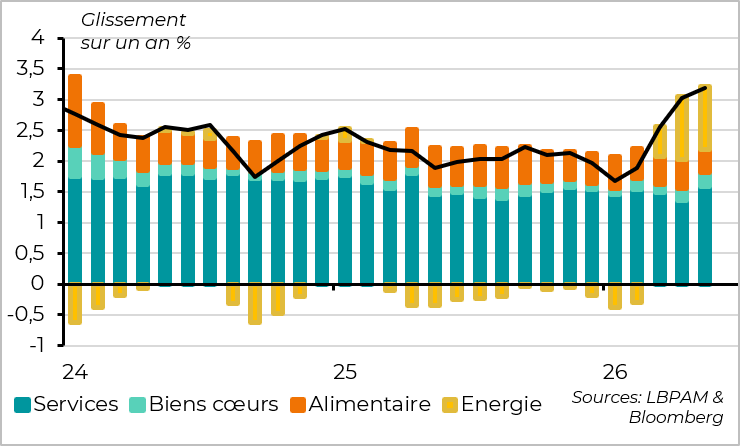

Inflation continued to accelerate in May, as expected, rising from 3.0% to 3.2%. However, the breakdown of this increase is unlikely to please the ECB.

Indeed, unlike in the first two months of the war in Iran, the increase in inflation in May was not driven by energy. Energy inflation remained broadly stable at 10.9% in May, after 10.8% in April, as energy prices fell by 1.1% over the month following a 10% increase in March–April. Beyond the stabilization in market prices, this largely reflects the reduction in taxes in Germany, which offsets higher gas retail prices.

The positive surprise is that the rise in inflation did not come from food either, as food inflation slowed more than expected, from 2.4% to 2.0% in May, its lowest level since 2021. At the very least, the pass-through from energy prices to food prices remains absent for now (although it is still expected to materialize with a lag of around six months).

The increase in inflation is therefore due to core inflation (i.e., excluding energy and food), which rose more than expected in May, from 2.2% to 2.55%. This is its highest level in a year, after having slowed during the first two months of the war, and it may suggest that higher energy prices are starting to feed through to the prices of other goods.

Services prices have been reaccelerating for the past two months

On the one hand, the rise in core inflation in May is overstated, as it mainly reflects an unfavorable base effect (due to the stagnation of services prices in May 2025) and an adverse calendar effect this year. The detailed breakdown in the final release should show that the increase in services prices is largely driven by volatile tourism-related components.

That said, goods prices are also rising more than expected (+0.9% year-on-year), and sequential price momentum has picked up significantly over the past three months (+2.9% over three months, annualized).

We continue to expect inflation to stop rising in the coming months (provided energy prices do not increase sharply again) and to return toward the 2% target over the course of next year.

However, for the ECB, the fact that both inflation and oil prices are slightly above its March forecasts at the start of Q2 is likely to lead it to revise its projections somewhat in June, thereby reinforcing its determination to raise rates next week. We expect the ECB to adopt a more balanced communication going forward, as inflation risks would be limited if the energy shock fades and the impact on activity is already clearly negative. Nevertheless, the acceleration in prices in May could lead hawkish members to maintain a more tightening bias in their forward guidance.

Xavier Chapard

Strategist