To put an end to the war

Link

What are the key takeaways from the market news on March 17, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► President Trump seems to want to end the war he initiated. However, Iranian officials appear reluctant to engage in dialogue and continue carrying out attacks in the region. This repeatedly leads to the blockage of the Strait of Hormuz, which keeps Brent crude oil prices above 100 dollars.

►At the same time, American attacks are also continuing. This weekend, U.S. forces bombed Iranian military infrastructure on Kharg Island. The threat involves destroying the country’s main oil export terminal. If that were to happen, Iran would be almost unable to export. However, such destruction would only further worsen the conflict.

►At this stage, the American president is trying to call on other NATO countries to help reopen the Strait of Hormuz. For now, he does not seem to be gaining much support. Likewise, China, which is the main importer of Iranian oil, does not appear willing to get involved in the conflict. As a result, President Trump has decided to postpone the summit with Xi Jinping, the Chinese president, that was scheduled for the end of the month.

►It seems difficult to imagine this deadlock lasting. The most likely outcome appears to be a U.S. withdrawal. Indeed, the economic and political cost within the country risks becoming too high as the war drags on, especially with the midterm elections on the horizon. It will be up to Donald Trump to find the right victorious rhetoric to exit the conflict—highlighting that Iran’s military capabilities have been significantly reduced, while nevertheless abandoning some of the objectives he had set for himself, such as regime change.

►In this scenario, even if disruptions could persist in the oil and gas (LNG) markets, as well as for other commodities while the Strait of Hormuz gradually reopens, it is reasonable to expect a return to normal maritime trade during the spring, along with a consequent decline in energy prices.

►Of course, a more adverse scenario is possible, though in our view less likely. If the conflict were to continue well beyond the summer, it would have far more negative consequences for growth and would keep inflation well above central bank targets for an extended period. The impact on the market would be significantly more negative than what we have seen so far.

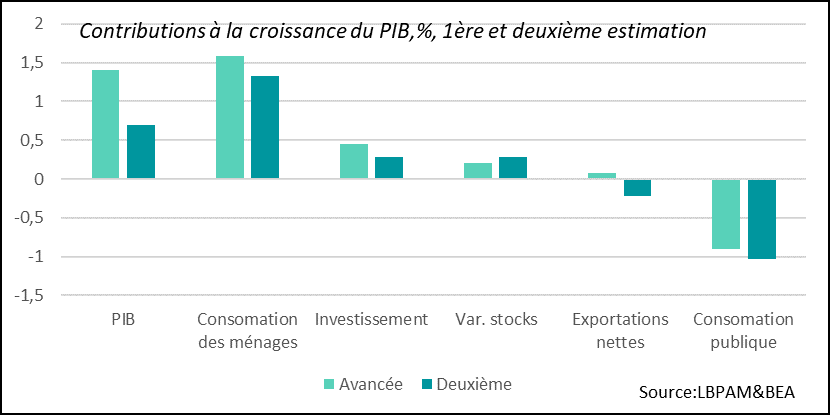

►While the war continues, economic data does not yet clearly show its scars. Indeed, as we saw with the activity indicators (PMIs), growth remained well oriented through February. However, in the United States, the momentum at the end of 2025 was far weaker than expected. U.S. GDP growth dropped sharply in Q4 2025 to 0.7% at an annualized rate, meaning the expansion was cut in half compared with the first estimate. Almost all demand components saw their growth revised downward. This highlights the risk of an energy shock hitting the U.S. economy at a time when demand has slightly weakened.

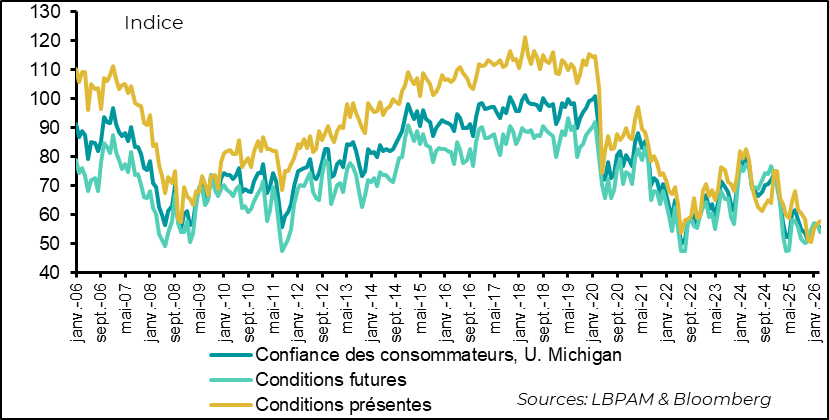

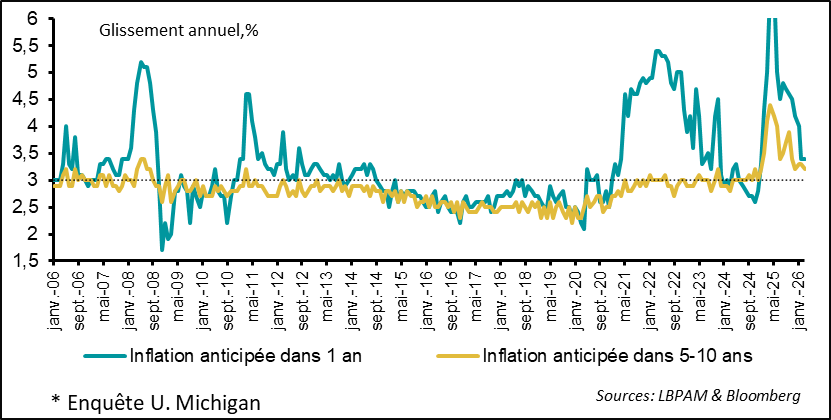

►At the same time, the preliminary survey on household confidence for March from the University of Michigan shows a relapse. However, the decline appears to be very modest. It seems the survey did not fully capture the negative effects of the energy shock. In fact, paradoxically, despite the very sharp increase in gasoline prices in March, inflation expectations appear to have eased, even as gasoline prices are soaring.

►We will see tomorrow what the Fed’s assessment of the current situation will be. We continue to believe that the status quo will be maintained and that the Fed will remain cautious throughout the year, with only one rate cut expected by early summer.

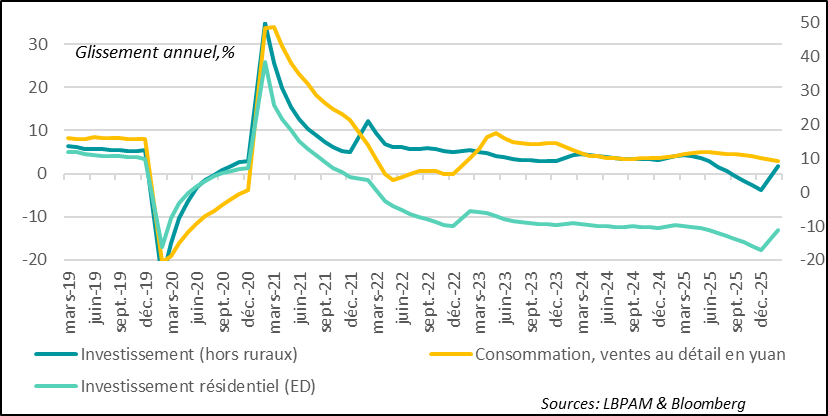

►Moreover, China has shown signs of a rebound in domestic demand over the first two months of the year. This recovery has been driven by investment and consumption, while external trade remains resilient, in turn supporting industrial production. As investment in technology is a major objective for the authorities, the government will also need to continue providing support to consumption in order to meet the new GDP growth target (4.5%–5%).

Going Further

United States: American growth is holding up, but the energy shock is weakening it

Growth momentum at the end of 2025 was much weaker than expected

We know that the latest activity surveys for February were relatively favorable in the United States, especially in the services sector. Nevertheless, the latest revision of U.S. GDP figures for Q4 2025 shows that the economy’s momentum was much weaker than previously estimated. Indeed, growth — already weak in Q4 2025 — was revised down by half in the latest estimate, to 0.7% at an annualized rate.

Admittedly, a large part of this revision reflects the negative impact of the government shutdown at the end of 2025. However, all components of demand were revised lower. We still expect the economy to rebound in Q1 2026, thanks to a reversal of the drastic adjustment in public spending at the end of last year. But this rebound will depend heavily on how households and firms react to the surge in energy prices in March.

For now, as mentioned earlier, before the war, companies were providing rather positive signals in the ISM activity surveys. However, the key point will be household behavior, as their appetite for consumption appears to have slowed. This deceleration can partly be attributed to a labor market that has weakened, with unemployment rising in February. This seems to reflect firms’ wait‑and‑see attitude on hiring decisions. In addition, the persistence of relatively high inflation is eroding purchasing power and is therefore another factor weighing on consumption.

Inflation remained elevated at the start of the year

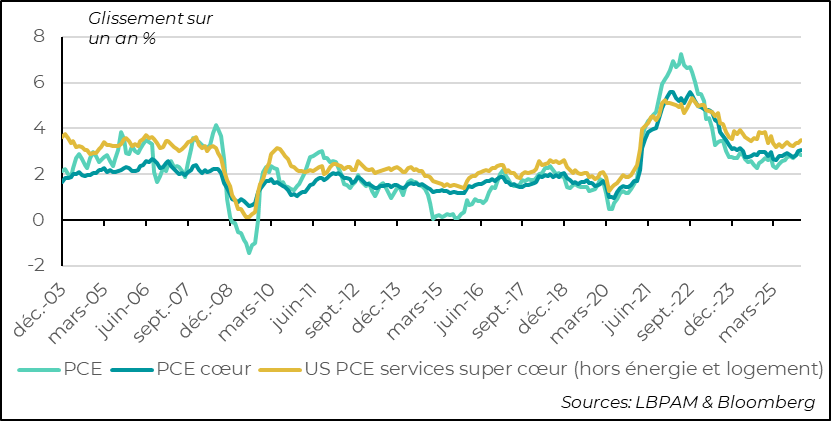

Indeed, the personal consumption expenditures (PCE) price deflator, the Fed’s preferred inflation gauge, remained elevated at the start of the year. Although it edged down slightly in January compared with the previous month on a year‑over‑year basis — 2.8% versus 2.9% — it is still high. More importantly, the decline was driven by lower energy prices. As for core inflation (excluding food and energy), prices accelerated to an annualized rate of 3.1% in the first month of the year.

This level remains high and is one of the reasons the Fed is likely to remain cautious. At the same time, it is important to highlight that underlying price dynamics remain relatively favorable. The Dallas Fed trimmed mean inflation indicator, which excludes extreme price movements, continues to point toward a downward trend ahead.

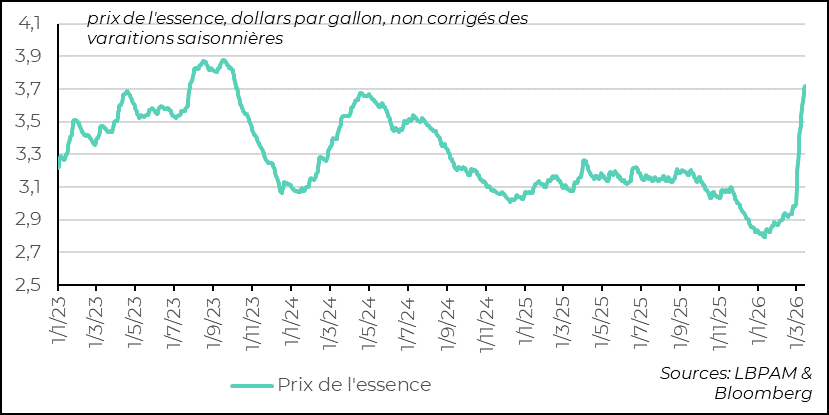

The rise in oil prices is strongly pushing gasoline prices higher

But since then, the oil shock has pushed gasoline prices sharply higher. In March alone, gasoline prices have risen by more than 30%. This is likely to push headline inflation upward and significantly constrain household purchasing power. As a result, the favorable momentum we have seen so far in the U.S. economic outlook could face a short‑term setback.

Household confidence not affected by the energy shock… for now

Paradoxically, the impact of this significant energy shock did not really show up in the University of Michigan’s preliminary consumer confidence survey for March. Although confidence remains historically low, it only declined slightly in March compared with the previous month.

Surprisingly, inflation expectations remain relatively stable

Above all, inflation expectations have even declined, which seems rather odd. Normally—at least for short‑term expectations (1 year)—households tend to extrapolate the trend following an energy shock. That is not the case here. It is likely that the final survey will deliver a somewhat different message.

Tomorrow, the Fed will give us its assessment of the current situation. In our view, given the prevailing uncertainty, the message is likely to be one of caution, signaling a continuation of the current policy stance. However, attention will mainly focus on the message conveyed by all members of the Federal Open Market Committee through their economic projections. We continue to expect only one rate cut in 2026, likely to take place by early summer.

China: A better‑than‑expected start to the year

A rebound in domestic demand over the first two months of the year

After a worrying trend at the end of last year, the Chinese economy appears to have rebounded at the start of the year. Indeed, the combined statistics for January and February (used to correct for distortions caused by the Lunar New Year holidays) showed that both consumption (measured by retail sales) and investment picked up over the period.

Total retail sales in yuan rose by 2.8% year‑over‑year, reversing much of December’s deceleration. Nevertheless, even if the energy shock for households is likely to be milder than in other countries, it could still have an impact in the coming months. In addition, the government has announced a reduction in certain consumption subsidies, which could also weigh negatively on consumer appetite. We will therefore have to wait for the next few months to see whether this rebound persists.

Investment also grew much more than expected, increasing by 1.8% year‑over‑year, with infrastructure investment rising by 11.4%. This latter figure shows that the strategy of the Chinese authorities has not changed: support for demand continues to rely heavily on public investment. This increase goes hand in hand with a renewed momentum in industrial production, which expanded by 6.3% year‑over‑year. Industrial production also continues to be supported by strong export dynamics.

The question now is how the Chinese authorities will manage the effects of the energy shock on their economy, and whether they will become involved in the war — at least as mediators with the Iranian regime — in order to achieve a ceasefire more quickly.

Sebastian Paris Horvitz

Director of Research