To test the market’s patience

Link

What are the key takeaways from the market news on March 31, 2026? Sebastian Paris Horvitz provides some insights.

Overview

► The attacks on Iran by the United States and Israel continue, as do the Iranian retaliations affecting the entire region and the blockade of the Strait of Hormuz. In short, the war goes on. At the same time, D. Trump keeps sending mixed signals, at times announcing promising discussions with the Iranians to put an end to the war, only to soon after shift to a much more belligerent tone, as he did recently by promising to destroy all of Iran’s energy infrastructure. This lack of consistency may gradually erode the markets’ patience.

►Until now — and this includes our own view — many market participants had anticipated that this conflict, with its unclear objectives, would not last more than one to two months. The main reason for this, for the vast majority, is that a severe disruption in the global supply of hydrocarbons would have harmful consequences for the world economy. In particular, for President Trump, a sharp shock to Americans’ purchasing power could significantly undermine the Republican Party’s chances in the midterm elections scheduled for the end of the year.

►In our view, this scenario remains valid and still the most likely one. However, the more adverse scenarios for the global economy are gaining probability, especially following the U.S. decision to deploy additional ground forces with the potential objective of conducting direct military operations on Iranian territory. It is the rising likelihood of these scenarios that continues to weigh on risk-taking, particularly affecting countries and regions that are most dependent on energy supplies.

►Nevertheless, the market is still far from shifting toward worst‑case scenarios, as reflected in the relatively moderate declines in major countries’ stock indices. This is partly due not only to the reasonable expectation that the conflict will eventually come to an end, but also to the limited measures available to mitigate the current energy shock. In particular, beyond the OECD countries’ commitment to use their strategic oil reserves on an unprecedented scale, some countries are already attempting to rely on the fiscal space they still have. But these stopgap measures remain limited.

►That said, if this war becomes bogged down, markets could shift toward far more extreme scenarios, going well beyond a temporary shock to hydrocarbon supplies. However, it still seems difficult today to understand why the Trump Administration would take the risk of becoming trapped in a prolonged conflict in Iran. The economic and political costs appear prohibitive. Yet one must acknowledge that time is ticking, and that an oil price remaining above 100 dollars per barrel for too long would change the equation.

►We are maintaining cautious positions in the very short term given the high level of uncertainty. However, we still consider that our central scenario — a time‑limited energy shock — should ultimately be supportive of risk‑taking. In this context, we also believe that central banks should be much more cautious about any potential tightening of their policy in response to price increases driven by a temporary rise in energy costs.

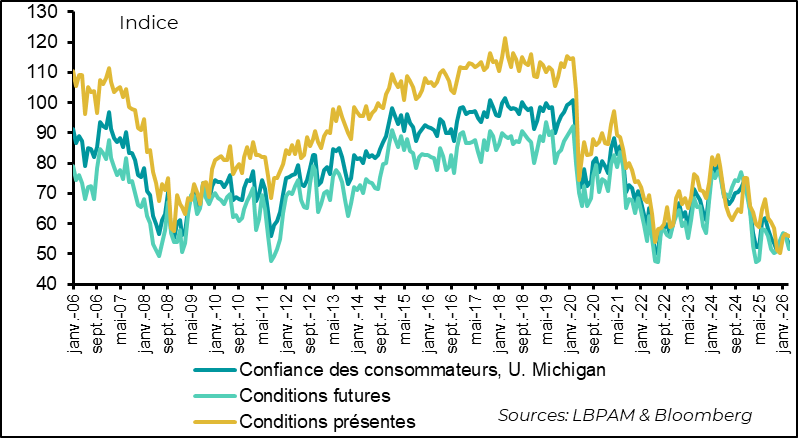

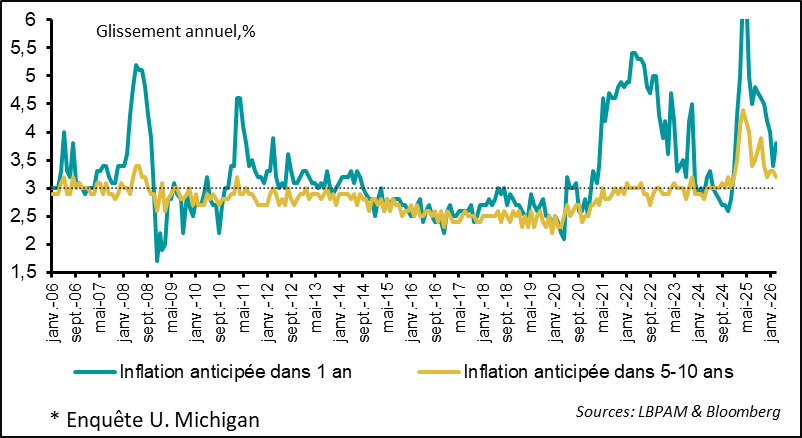

►At the same time, in the United States, the data remain fairly resilient. For example, household confidence, as measured by the University of Michigan, surprisingly declined only slightly in March, even though it remains historically low. This can partly be explained by long‑term inflation expectations (5–10 years) that remain contained, while short‑term expectations have risen more noticeably. This is not surprising given the surge in gasoline prices, which are now close to 4 dollars per gallon, up more than 30% over the month.

►Long‑term inflation expectations remaining contained among households is certainly good news for the Fed. In fact, yesterday, J. Powell, the Chair of the institution, while remaining cautious about the current situation, emphasized that inflation expectations remain well anchored, even though it is still too early to know what impact the war might have. More importantly, he reiterated that the Fed can do little in the face of a supply shock, such as a rise in oil prices. This is clearly an indication of the Fed Chair’s inclination to prioritize supporting growth (employment) rather than fighting the inflationary effects of this type of shock.

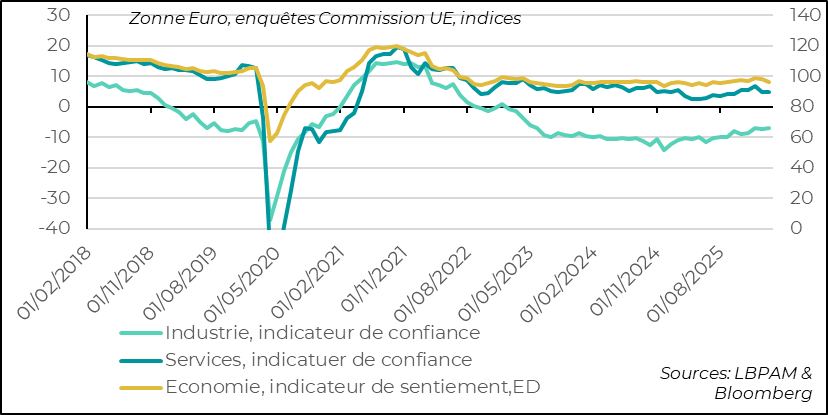

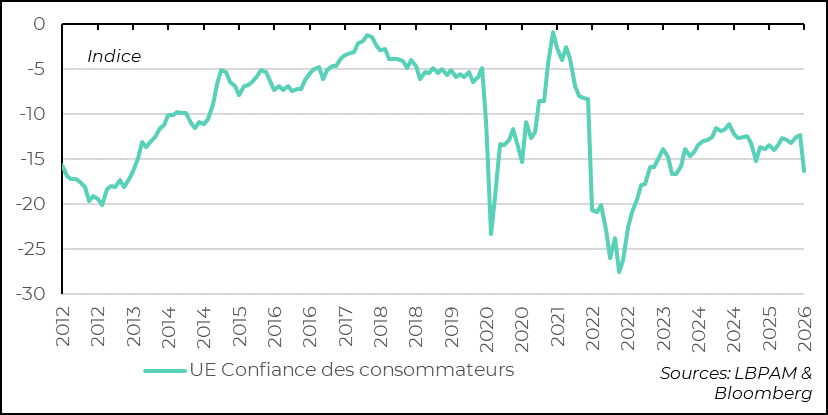

►In the Euro Area, the European Commission’s surveys on the state of the economy for March showed the negative impact of the war—although a moderate one—confirming the message from the PMI surveys. However, on the consumer side, the final consumer confidence survey confirmed the initially negative signal, with a sharp decline that broke the improving trend observed since the beginning of the year.

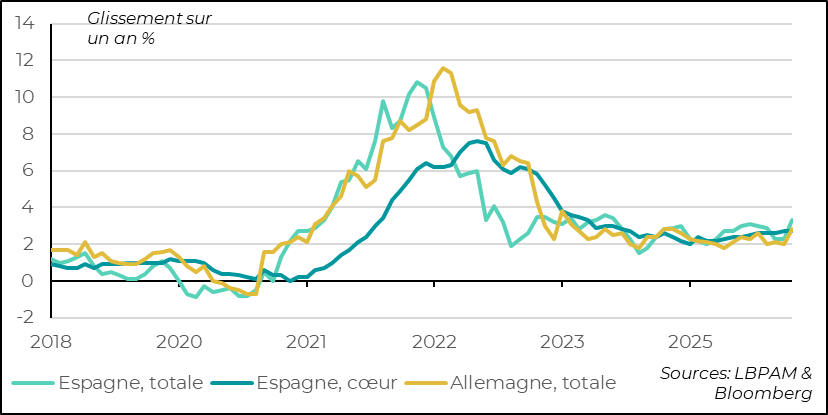

►Indeed, the first inflation figures for March show the impact of rising energy prices. In Germany, headline inflation, as expected, rose sharply over the month, reaching 2.8% year‑on‑year. This is mainly due to higher energy costs, which are up more than 7%. However, core inflation (excluding energy and food) is estimated to have remained unchanged at 2.5%. In Spain, inflation increased significantly, rising to 3.3% year‑on‑year from 2.5% previously. However, the rise was smaller than the expected 3.8%, largely due to the effects of VAT cuts on energy prices introduced by the government. This increase in inflation will naturally be reflected in the Euro Area inflation figure to be released today.

►Despite comments from the most orthodox ECB governors, calling on the institution to act quickly to counter the inflationary effects of rising oil prices, we still believe the ECB will remain cautious. We continue to expect, at most, a ‘preventive’ increase in policy rates in the spring, aimed at reinforcing the stability of inflation expectations, rather than a more forceful tightening such as the one still anticipated by the market for 2026.

Going Further

United States: Confidence Hit by Inflation and Uncertainty

Energy prices fluctuate according to the messages sent by the U.S. authorities

As expected, the final University of Michigan consumer sentiment survey came out more negative than the preliminary results. The confidence index declined again and remains at a historically low level. Nevertheless, there is no sign of a collapse. To a large extent, this drop in confidence is due to the surge in energy prices over the month. This is likely an important signal for U.S. authorities in an election year.

We will need to wait for the consumption data to assess the impact of these emerging concerns and better understand how this crisis is affecting growth. In addition, the employment figures to be released at the end of the week will shed light on how businesses are adjusting their hiring behavior. The risk is that companies continue to adopt a wait‑and‑see stance, thereby slowing down recruitment.

Short‑term inflation expectations are rising, but medium‑term expectations remain stable

Energy price increases played an important role in the decline in confidence. Indeed, gasoline prices rose by more than 30% in March alone. This was also clearly reflected in the sharp upward revision of short‑term (1‑year) inflation expectations, which climbed to 3.8% year‑on‑year from 3.4% previously.

At the same time — and this is reassuring — medium‑ to long‑term inflation expectations (5–10 years) remained stable at 3.2%. This seems to indicate that households expect the current situation not to last.

Of course, in a scenario where the conflict drags on, things could change dramatically. At this stage, despite the risks, we are not in that situation.

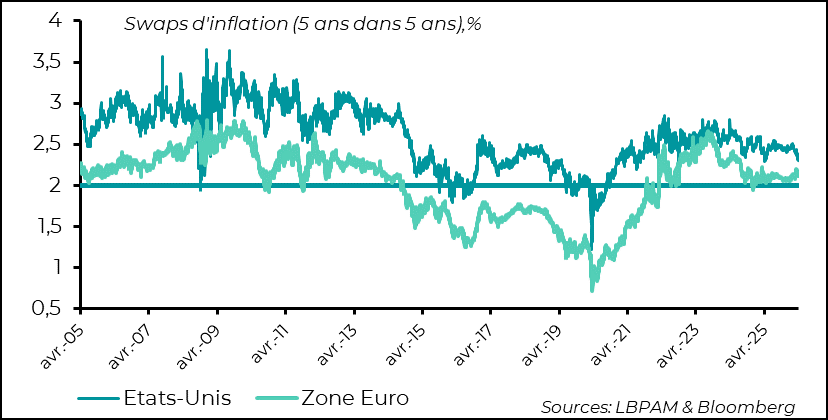

Market inflation expectations remain well anchored

Similarly, it is worth emphasizing that despite significant concerns about the inflationary effects of the war — not only on energy but also on certain production chains — market‑based inflation expectations remain well anchored on both sides of the Atlantic.

This was also reiterated yesterday by J. Powell, the Chair of the Federal Reserve, who stressed the need for caution when assessing the impact of the war in monetary policy decisions. He notably reminded that the central bank can do little in the face of supply shocks, such as a temporary spike in oil prices. In line with the Fed’s traditional approach and its mandate, the institution should therefore remain primarily focused on the potential negative effects on the labor market rather than on the inflationary impact of the current shock — while not ignoring it entirely.

Euro Area: Surveys Reveal the Negative Effects of the War

Euro Area: European Commission Economic Surveys Decline in March

Unsurprisingly, the European Commission’s economic surveys sent a negative signal regarding the impact of the war on the region’s economy. The Economic Sentiment Indicator therefore declined in March, breaking the previous recovery momentum. This is consistent with the message conveyed by S&P’s preliminary PMI indicators.

The only piece of good news is that industrial confidence remained relatively well oriented, likely supported by growth prospects linked to the German fiscal stimulus plan. However, this positive momentum could weaken if the conflict in the Middle East persists.

Households Hit by the Energy Shock

On the household side, the final consumer confidence survey for March confirmed a sharp decline. This development is clearly explained by the uncertainty generated by the ongoing war, but also very directly by the surge in energy prices.

Consumer Prices Reflect the Rise in Energy Costs

The sharp rise in energy prices since the beginning of March is already clearly reflected in the inflation figures now being released for the Euro Area.

In Germany, as expected, headline inflation increased to 2.8% from 2% the previous month. This was mainly driven by a more than 7% rise in energy prices. At the same time, it is worth noting that core inflation (excluding energy and food) likely remained unchanged at 2.5%.

In Spain, inflation also rose sharply, climbing to 3.3% year‑on‑year from 2.5% previously. However, this increase was significantly smaller than economists had anticipated. This is largely due to measures already implemented by the Spanish government to cushion the energy shock, particularly through a VAT reduction in the sector.

Today, the inflation figure for the Euro Area as a whole will be released. It is expected to show a sharp acceleration, estimated at 2.6% compared with 1.9% the previous month. However, core inflation should remain unchanged.

We continue to believe that it would be a mistake for monetary policy to react too quickly to this energy shock. In our scenario, we still expect only one ECB policy rate increase in 2026. This would serve as an insurance measure to help anchor inflation expectations. Accordingly, we expect the Governing Council to adopt a more moderate stance than that suggested by some of its more orthodox members.

Sebastian Paris Horvitz

Director of Research