Towards a Rebound in the Global Economy

Link

What are the key takeaways from the market news on June 26, 2026? Sebastian Paris Horvitz provides some insights.

Overview

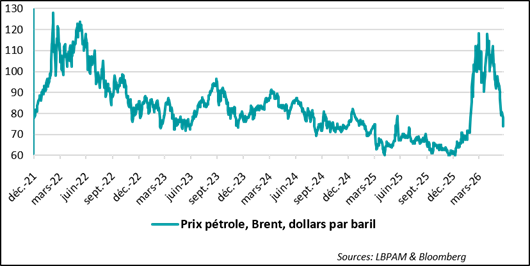

►Oil prices have continued to decline rapidly, as traffic through the Strait of Hormuz gradually returns to normal. While it is difficult to rule out potential disruptions, the most likely scenario remains a return to conditions close to those seen before the conflict, at least in terms of maritime traffic.

►Yesterday, the Iranian military reportedly slowed maritime traffic and even fired on a vessel. It is reasonable to assume that Iran will want to continue demonstrating its ability to control the Strait of Hormuz. Nevertheless, it will likely do everything it can to ensure that the region’s oil revenues flow back into the global market, providing the Iranian regime with much-needed financial resources.

►We expect oil prices to prove lower than previously anticipated. Brent crude could stabilize below $80 per barrel relatively quickly. Our forecast is for prices to settle around $75 per barrel by year-end. This outlook is based on the view that the oil market is likely to return to the supply surplus conditions that prevailed before the conflict.

►This outlook is subject to two key upside risks. First, and most obviously, a renewed escalation of tensions in the region. Second, oil demand could prove stronger than expected, driven by an acceleration in economic activity and the need to replenish strategic reserves.

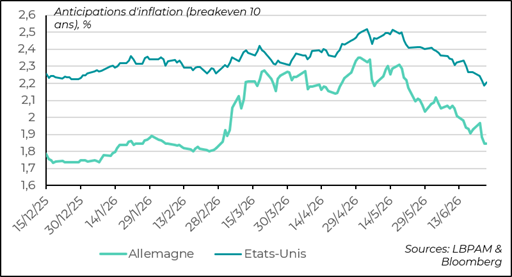

►A faster decline in energy prices would provide a welcome boost to economic activity, particularly in Europe given the region’s dependence on energy imports. More importantly, it would help reverse upward pressure on prices. This is already being reflected quite clearly in the sharp drop in inflation expectations as measured in bond markets. For 10-year government bonds, inflation expectations have fallen by more than 30 basis points from their May peak in the United States and by nearly 50 basis points in Germany, reaching either the lowest levels of the year (in the U.S.) or levels very close to them (in Germany).

►This scenario is supportive of risk-taking. Nevertheless, a degree of caution is warranted in the near term. We are likely to continue seeing significant volatility in technology stocks, particularly following the strong gains recorded by the sector in recent months. In addition, the outlook for central banks still needs to become clearer.

►In our view, it will be difficult for central banks to ignore these developments, even under more conservative assumptions regarding energy prices. Inflation expectations appear to remain well anchored in financial markets.

►In Europe, whether in the United Kingdom or the euro area, the energy price reversal is likely to bring inflation back onto a downward trajectory relatively quickly. In the euro area, the concern highlighted by the more hawkish central bankers is that second-round effects may already be taking hold. Given the weakening of demand across the region, however, we believe it would be premature to jump to such a conclusion. The European Central Bank is therefore likely to keep interest rates unchanged through the end of the year.

►In the United States, the situation is considerably more complex for the Federal Reserve. Unlike the ECB, inflation has never successfully converged to the 2% target, and the recent uptick in inflation could prove more persistent. Indeed, domestic demand has been among the most resilient to the energy shock. In our view, there is a significant risk that the Fed will raise its policy rates before the end of the year.

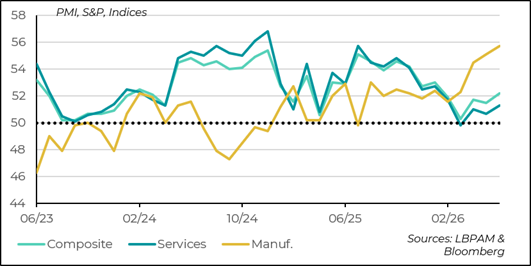

►Indeed, the latest S&P Global PMI surveys for the United States showed that economic activity is holding up much better than in other regions, albeit at a moderate pace. Manufacturing activity, particularly in sectors linked to artificial intelligence, remains highly dynamic. In addition, consumer spending data for May came in relatively strong, partly offsetting the weakness recorded in the previous month.

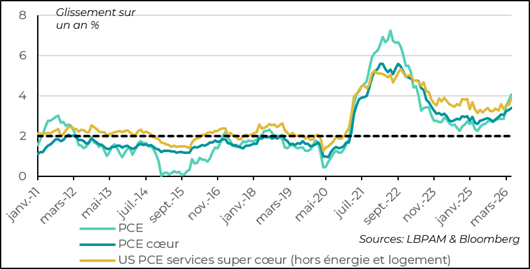

At the same time, inflation, as measured by the Personal Consumption Expenditures (PCE) price index—the Federal Reserve’s preferred inflation gauge—accelerated as expected in May, reaching 4.1% year-on-year, while core inflation rose to 3.4%. Nevertheless, trend indicators are sending mixed signals regarding the inflation outlook over the coming months.

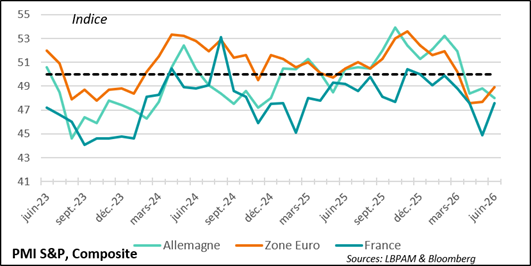

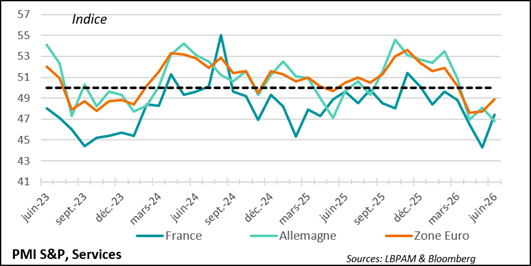

►In the euro area, the message from the preliminary S&P Global PMI surveys for June remains rather weak, although conditions are improving. The composite PMI (covering both services and manufacturing) edged higher, signaling a modest rebound in activity. However, it remains in contraction territory, suggesting that overall economic momentum is still subdued.

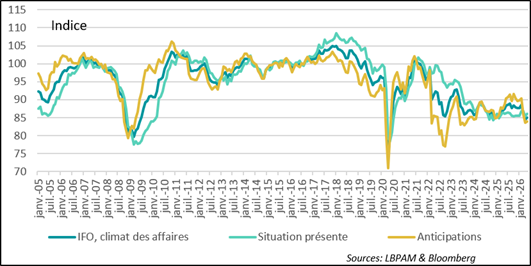

►The main disappointment at the start of June was the sharp deterioration in Germany’s services sector, even as manufacturing activity proved more resilient. The services PMI fell to its lowest level in more than three and a half years. However, this weakness may be overstated, as the IFO business climate survey pointed instead to a modest improvement in business conditions.

Going Further

Oil: A Decline That Could Reinforce a Global Economic Rebound by Year-End

A Very Rapid Decline in Oil Prices

In just a few weeks, oil prices have fallen dramatically. The prospect of the reopening of the Strait of Hormuz gradually set this trend in motion. However, over the past two weeks, the decline has been particularly striking. Indeed, Brent crude is already approaching $70 per barrel, only around 10% above the level that prevailed before the conflict.

Markets recognize that the path toward the full normalization of maritime traffic through the Strait of Hormuz is unlikely to be entirely smooth. Nevertheless, the overall direction is clearly one of normalization.

As a result, the oil market could, in the coming months, return to the situation that existed before the conflict—that is, a market characterized by excess supply.

The market balance will, of course, depend on the pace at which traffic through Hormuz returns to normal and, more importantly, on the evolution of demand.

In the very short term, demand is expected to recover gradually. Over the coming months, however, the broader economic recovery should provide additional support. Demand will also be influenced by the speed at which strategic reserves—particularly in the United States and China—are replenished.

On the supply side, oil availability is expected to become abundant once again and remain above demand. This is especially true as several Gulf countries are eager to increase their production quotas in order to offset the revenue losses incurred during the conflict. Iran, too, could boost production if, as envisaged under the current framework agreement, the sanctions affecting the country are lifted. Russia remains the main uncertainty, since it is still unclear whether the United States will reinstate all of the sanctions that were suspended during the conflict with Iran.

At this stage, we expect oil prices to settle below the levels we were forecasting only a few weeks ago. Brent crude could remain somewhat below $80 per barrel in the months ahead and gradually stabilize at around $75 per barrel by year-end.

Inflation Expectations Continued to Decline in Financial Markets

One of the most important consequences of the rapid decline in oil prices is its impact on the global inflation outlook.

Indeed, the downward trend that had already become apparent in bond markets over recent weeks has accelerated significantly. Inflation expectations, as measured by 10-year breakeven inflation rates derived from inflation-linked bonds, have fallen sharply. In fact, these expectations have now either dropped below the levels that prevailed before the conflict, in the case of the United States, or moved very close to them, as in the euro area, particularly in Germany.

It is possible that markets are becoming somewhat complacent regarding the future path of inflation. Nevertheless, these developments cannot be ignored by central banks. They suggest that policymakers should remain cautious about overreacting to the sharp increase in inflation recorded in recent months.

In the euro area, we believe it is far too early to conclude that the energy shock—even though it lasted considerably longer than initially anticipated—has already triggered significant second-round effects, meaning inflationary pressures extending beyond the direct impact of higher energy costs through mechanisms such as wage and price indexation. As a result, we believe that the European Central Bank should be careful not to overreact, particularly given that it has already tightened monetary policy through higher policy rates. We continue to believe that these rate increases should prove sufficient to keep inflation expectations well anchored.

The situation in the United States appears quite different. First, since the surge in inflation following the COVID-19 pandemic, inflation has never fully converged back to the Federal Reserve’s 2% target. More importantly, the U.S. economy has proven far more resilient to the recent energy shock than most other major economies. Consequently, while lower energy prices should contribute relatively quickly to disinflation, the process could remain gradual, with underlying inflationary pressures persisting.

Against this backdrop, we believe that the likelihood of a further increase in the Federal Reserve’s policy rate remains significant. This view has been echoed by a large number of members of the Federal Open Market Committee during recent meetings, many of whom have expressed support for additional monetary tightening. At the same time, Kevin Warsh, the Fed’s new Chair, has emphasized the importance of bringing inflation back toward the 2% target as quickly as possible.

United States: An Economy That Remains Resilient

Industry Still Driving the Resilience of the U.S. Economy

The preliminary S&P Global PMI surveys for June once again highlighted the greater resilience of the U.S. economy compared with other major economies. Indeed, the composite PMI moved back into growth territory. Nevertheless, economic strength continues to be driven primarily by the industrial sector. This partly reflects the dynamism of industries linked to artificial intelligence, ranging from semiconductors to the construction of data centers. The survey also continues to indicate that part of the support for demand is coming from precautionary inventory-building by companies, driven by supply-chain uncertainties related to the situation in the Middle East and rising costs. This factor is likely to begin fading over the coming months.

In the services sector, conditions appear to have improved in June, but the outlook remains less supportive due to the impact of the energy shock on household purchasing power. Encouragingly, this effect should ease significantly in the months ahead.

The less positive elements of the surveys relate to employment and prices. On employment, companies continue to report a cautious stance, with staffing levels generally adjusting downward. However, this does not fully align with the latest U.S. employment data. On prices, firms continue to report rising costs and, more importantly, a willingness to pass these increases on to customers.

Overall, while these figures show that economic activity remains resilient in the United States, the level of the indicators points to relatively modest growth by the standards of recent history.

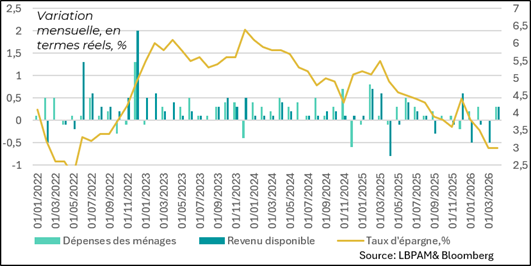

Consumer Spending Rebounded in May

On the demand side, consumer spending rebounded in May following a rather disappointing April. These figures suggest that consumption remains resilient, albeit at the cost of a significant decline in the savings rate. This is likely to act as a moderating factor for consumer spending in Q3 2025.

That said, inflationary pressures may prove weaker than current data suggest, particularly in light of the substantial downward revision to consumer spending in the first quarter that was incorporated into the latest GDP release.

Inflation Continues to Erode Purchasing Power

The main factor weighing on consumer spending is, of course, higher inflation. The Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures (PCE) price index, accelerated as expected in May to 4.1% year-on-year, while core inflation also rose to 3.4%.

Clearly, most of this increase is attributable to energy. However, price increases are also accelerating in the services sector, excluding energy and rents. This is a trend that should be a source of concern for the Federal Reserve.

Trend Measures Are Not Necessarily Reassuring

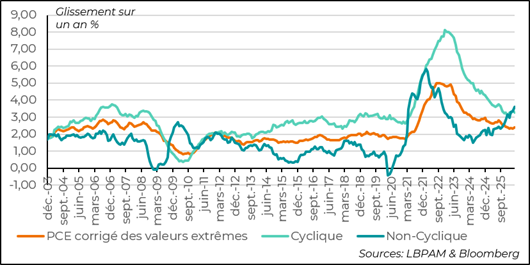

Trend measures are not particularly reassuring, especially when looking at the evolution of prices that are typically relatively stable (acyclical prices). Similarly, the Atlanta Fed’s measure, which excludes the most extreme price movements, has resumed an upward trend.

These developments are likely to encourage the Federal Reserve to maintain a relatively hawkish stance in its communications.

Euro Area: Activity Stabilizes, but a Rebound Has Yet to Materialize

Activity Improved in June, but the Region Remains Stuck in Low Gear

The S&P Global PMI survey for June showed a slight improvement in economic activity across the euro area. Nevertheless, the composite PMI (covering both services and manufacturing) remains in contraction territory. The easing of energy prices should help reverse part of the ground lost in recent months, particularly by supporting a recovery in confidence.

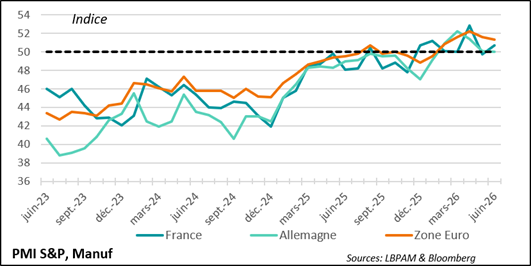

Industry, as Elsewhere, Is Holding Up Better

Industrial activity shows that, as in many countries, the sector remains one of the key supports for economic growth. Public support measures in this area are substantial, particularly those coming from Germany. We expect lower energy prices to provide a further boost to industrial activity in the coming months, especially if German government spending accelerates, as we anticipate.

Services Remain the Weak Link

The survey showed that the services sector remains in contraction territory, reflecting the impact of the shock to household purchasing power. However, the most disappointing development came from Germany, where activity fell sharply and somewhat unexpectedly. Germany’s services PMI has now dropped below France’s, despite France having previously been regarded as the weakest major economy in the region.

Confidence Rebounded in June After Being Severely Hit Since March

However, this rather negative signal from Germany may be somewhat overstated, as the IFO survey for June paints a much less pessimistic picture. Admittedly, both the headline indicator and its subcomponents remain deeply depressed, but there is no sign of a renewed downturn.

The most concerning element remains expectations, which have yet to regain meaningful momentum. In this respect, the German government will have an important role to play in supporting demand and restoring confidence among economic agents. Furthermore, for German industry, the depreciation of the euro could provide a welcome boost in the months ahead.

Sebastian Paris Horvitz

Director of Research