Until when?

Link

What are the key takeaways from the market news on April 28, 2026? Sebastian Paris Horvitz provides some insights.

Overview

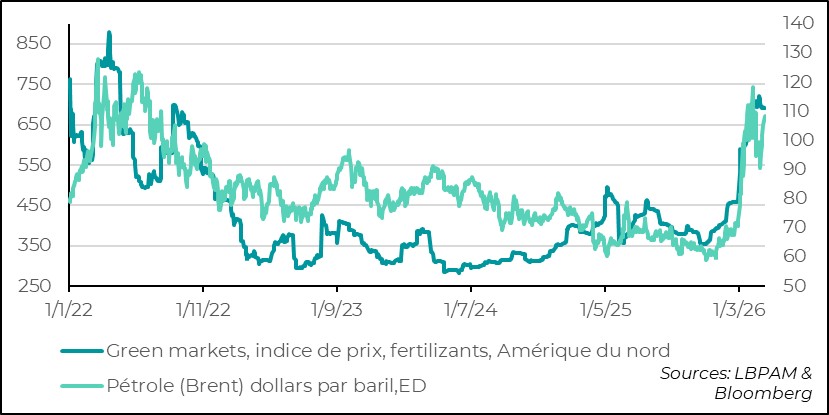

► Since negotiations between the United States and Iran were halted last week, the situation has shown no change. While one can certainly take some comfort in the fact that the war has not resumed, peace is, for the time being, not in sight. At the same time, for the global economy, the continued closure of the Strait of Hormuz, resulting from the Iranian and American deadlock, represents a very negative shock. This is reflected first and foremost in the price of a barrel of oil (Brent), which has returned well above 100 dollars. Moreover, signs of shortages of petroleum products are emerging in certain regions. Announcements by airlines suspending flights in order to save fuel are a striking example. In addition, tensions persist in the prices of other crucial raw materials, particularly for agriculture (fertilisers).

►As we have indicated since the beginning of this conflict, the magnitude of the shock and its duration are the key factors in determining its impact on the global economy. As the conflict approaches its second month, global growth is likely to be more affected than we initially anticipated. Nevertheless, the stabilisation of the Brent crude price around 100 dollars and, for Europe, of gas prices around 40 euros somewhat limits the scale of the shock. Obviously, a resumption of hostilities would very likely trigger a much more severe shock. However, we continue to assign a lower probability to this scenario, given the significant negative effects it would entail for both parties to the conflict.

►The prolongation of the crisis will weigh on economic growth and exacerbate inflationary pressures. A further deterioration in the economic outlook, without necessarily leading to a recession, could fairly quickly weigh on risk-taking, which has dominated market dynamics in recent weeks. While the energy sector could continue to prove resilient in equity markets, segments that have rebounded strongly, such as semiconductors, could come under pressure, even if only temporarily. In this new environment of heightened uncertainty, we are therefore adopting a tactically somewhat more cautious stance in the very short term.

►Central banks will be key players in managing this crisis. Our central scenario remains that most central bankers will adopt a very cautious stance. At this stage, in the major economies, the acceleration in inflation is mainly the result of the mechanical effect of rising energy prices, without giving rise to a broad-based spillover to other prices. As a result, market indicators continue to show that inflation expectations remain well anchored, that is, close to central banks’ targets. On the growth side, the impacts are not yet of a massive magnitude. Nevertheless, with almost all major central banks meeting this week, it will be crucial to analyse how they assess the situation.

►On the Fed side, the monetary policy committee meeting will be held under particular circumstances, as it is expected to be the last one chaired by Jerome Powell. Indeed, following the decision by the Department of Justice to drop the charges brought against him in connection with the renovation work at the Fed’s buildings in Washington, Republican Senator Thom Tillis—who had been blocking the nomination of Kevin Warsh—announced that he was prepared to vote in favour of Warsh’s confirmation at the head of the institution. As a result, J. Powell will step down from the presidency as early as May. A new chapter will therefore open at the Fed. Kevin Warsh, the new chair, will immediately come under close market scrutiny regarding his ability to assert the institution’s independence in the face of pressure from the U.S. president.

►The Bank of Japan (BoJ) has decided to leave its policy interest rates unchanged. Nevertheless, the vote within the board of governors was split, with three out of nine members voting in favour of a rate hike. This likely represents an important signal regarding the future direction of monetary policy. As expected, the BoJ highlighted the uncertainties linked to the war in the Middle East to justify its decision. However, it has indicated that it stands ready to raise rates should its economic forecasts materialise. Thus, barring a deterioration in the situation in Iran, we believe that the BoJ should resume the normalisation of its monetary policy as early as its June meeting.

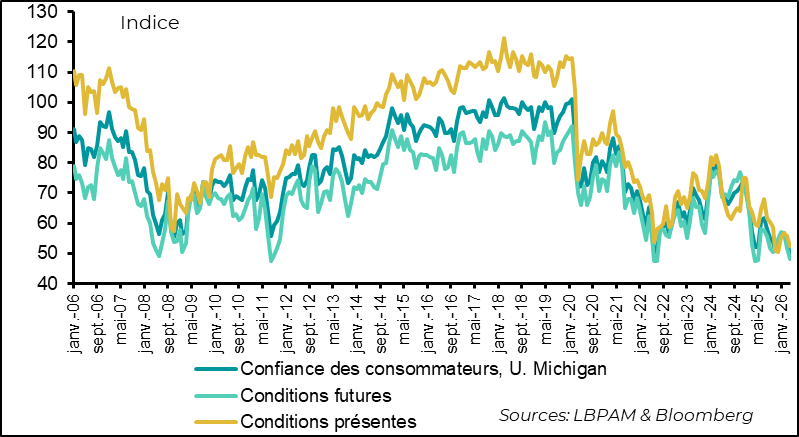

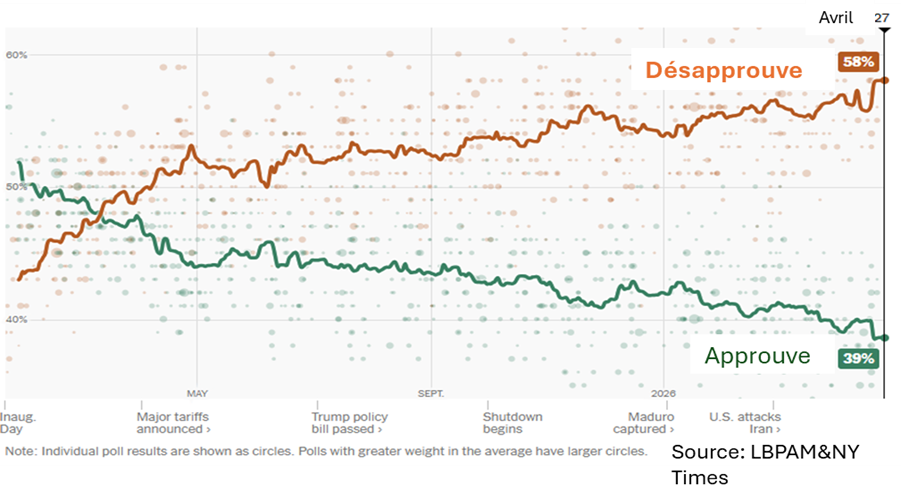

►One of the key factors explaining the strong incentive for U.S. authorities to reach a rapid agreement with Iran and to normalise energy costs lies in the direct impact on American consumers. Indeed, the final April reading of the University of Michigan’s consumer confidence survey, while slightly higher than the preliminary estimate, remains at a historical low. The decisive factor continues to be rising inflation driven by higher energy prices. This deterioration in confidence can be directly linked to the decline in President Trump’s approval rating, which has fallen to its lowest level in polls since the beginning of his term.

►In the euro area, the rise in energy prices—particularly gas prices, as reflected in the PMI indicators—has significantly affected economic conditions. In particular, the positive effects of the German stimulus plan are largely being offset. This is the message conveyed by the IFO survey, which declined again in April, notably due to a sharp drop in expectations. These deteriorating economic outlook elements will very likely need to be taken into account by the ECB when shaping the future path of its monetary policy.

Going Further

Middle East war: the continued closure of the Strait of Hormuz is keeping strong upward pressure on energy prices

Le prix du pétrole repasse au-dessus de 100 dollars et la pression s’accentue sur les fertilisants

The deadlock in negotiations between the Americans and the Iranians has resulted in the continued closure of the Strait of Hormuz. This situation is exerting additional pressure on oil and gas prices. As a result, the price of a barrel of oil (Brent) is approaching 110 dollars, while gas prices in Europe have risen back above 40 euros per MWh. These shocks have a direct and rapid impact on economic conditions.

Indeed, the latest economic indicators, particularly in Europe, clearly illustrate how this crisis has disrupted the favourable momentum observed since the beginning of the year.

We have already revised down our forecast for European growth in 2026 to take into account the negative effects of this energy shock, which is expected to materialise particularly in the second quarter of 2026. Nevertheless, the main risk remains that the crisis persists, which would call into question our assumption of a swift resolution. A prolongation, even if limited to a few months, would very likely significantly deteriorate growth prospects for the rest of the year. In this regard, developments over the coming weeks will be crucial, both for the economy and for financial markets.

This uncertainty leads us, from a tactical standpoint, to adopt a more cautious stance on the markets, especially as the rebound in risk-taking observed after the ceasefire has been particularly strong.

Finally, while the most visible shocks concern energy prices and supply, the growing impact on the prices of all goods transiting through this conflict zone should not be overlooked. This is particularly the case for fertilisers, which play a key role in agricultural production. As things stand, a significant negative impact can already be anticipated over the coming quarters.

États-Unis : la dégradation de la confiance va-t-elle peser sur les autorités américaines pour parvenir à un accord de paix ?

Consumer confidence at a record low

The final reading of the University of Michigan’s U.S. consumer confidence survey for April came in slightly above the preliminary estimate, but it remains at a record low, at 49.8. While the divide remains very pronounced along political lines among respondents, a large majority nevertheless view the economic situation as highly deteriorated.

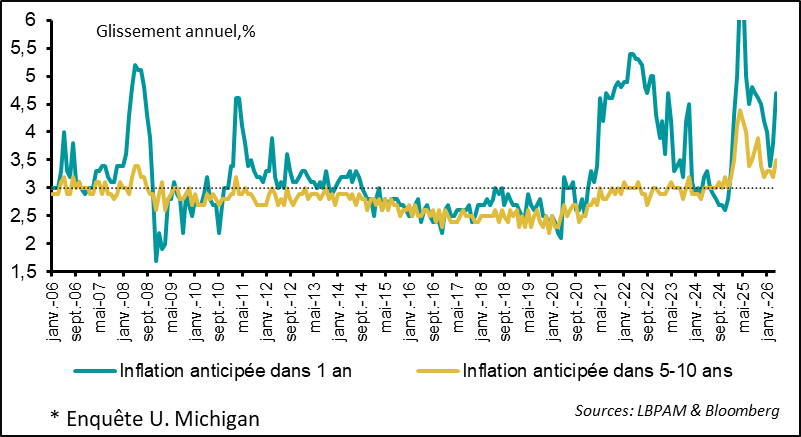

Inflation expectations on the rise

Le facteur le plus important expliquant cette situation est évidemment la hausse du coût de la vie. En effet, le prix du gallon d’essence demeure au-dessus de 4 dollars, soit son niveau le plus élevé depuis l’invasion de l’Ukraine par la Russie en 2022. Dans ce contexte, les anticipations d’inflation, notamment à moyen terme, sont de nouveau reparties à la hausse.

President Trump’s popularity at a record low in the polls

This deterioration in confidence is likely one of the key factors that could push U.S. authorities to reach an agreement with Iran in order to normalise the situation in the Strait of Hormuz. Nevertheless, at this stage, there is no indication that President Trump is adopting a more constructive tone or a more conciliatory stance with a view to negotiating a lasting agreement with Iran. The coming days will therefore be critical in assessing whether a shift in attitude—one that could reassure markets and economic agents—is likely to take place.

What is certain, however, is that President Trump’s popularity has continued to deteriorate in recent weeks. According to a polling average published by The New York Times, his approval rating now stands well below the level observed at the same point during his first term.

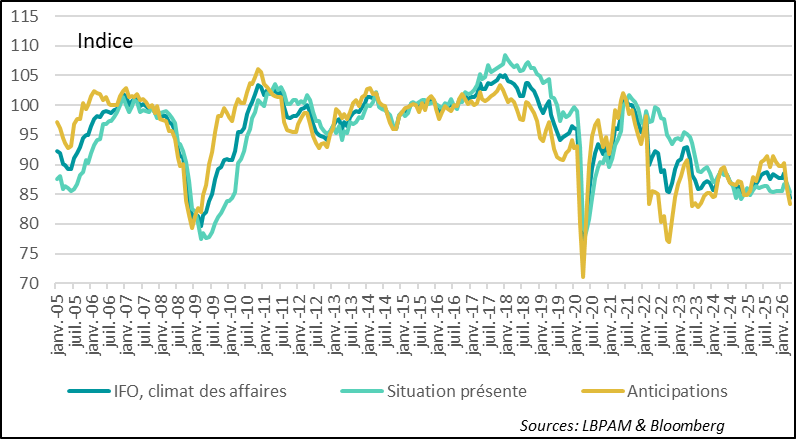

Germany: economic conditions are weakening amid rising energy prices

Germany heavily affected by the war in Iran

The April IFO survey confirmed the deterioration in the momentum of the German economy in the face of the energy shock triggered by the war in Iran. It is clear that this crisis has disrupted the favourable momentum observed at the beginning of the year, significantly undermining business confidence in the economic outlook.

As a result, the positive effects of the stimulus plan implemented by the German government are set to be largely offset by the consequences of this crisis. The most striking aspect of the IFO survey lies in the very sharp deterioration in expectations, with a significant decline in the indicator measuring confidence in future conditions.

As we have already indicated, should this shock persist in its current form, the economic consequences would be more severe than we presently anticipate. We have already carried out a substantial downward revision of our euro area growth forecast for 2026, now set at 0.8%. This estimate could nonetheless be revised further downward in the absence of a rapid move towards a resolution of the crisis.

In this context, the ECB will need to factor in this new environment when shaping the future orientation of its monetary policy. In our view, the growing risks weighing on economic conditions should prompt the central bank to adopt—or maintain—a particularly cautious stance.

Sebastian Paris Horvitz

Director of Research