We must wait and see, but be ready to act

Link

What are the key takeaways from the market news on March 20, 2026? Xavier Chapard provides some insights.

Overview

► As the end of the third week of war in Iran approaches, the escalation continues on the ground, with attacks on energy infrastructure by the Israelis in Iran and by the Iranians against their neighbors (including Qatar, which produces nearly 20% of the world’s liquefied natural gas). Despite calls from D. Trump and Netanyahu to avoid targeting energy facilities, as this would prolong the return to normal prices, oil and gas prices have reached their highest level since 2022. Our scenario of de-escalation after a few weeks and a decline in energy prices during the second quarter still holds, but the risks of a more negative scenario are increasing.

►Faced with uncertainty, central bankers have generally kept their rates unchanged and indicated that they are waiting to see (the magnitude, duration, and impact of the energy shock). However, overall, their messages have become less accommodative, for different reasons. This confirms the rise in market expectations since the start of the war.

►The ECB appears closer to a rate hike than we had anticipated, even though Christine Lagarde’s messages signal no urgency and the statement remains neutral. Indeed, core inflation would remain above the 2% target in all three scenarios presented by the ECB, while the impact on the economy would be relatively limited. Lagarde also indicated that the ECB would not wait to see second‑round effects before raising rates if the energy shock is significant, unlike in 2022. We maintain our scenario of stable rates this year, but it would only take energy prices remaining high in Q2 for the ECB to raise rates before the summer.

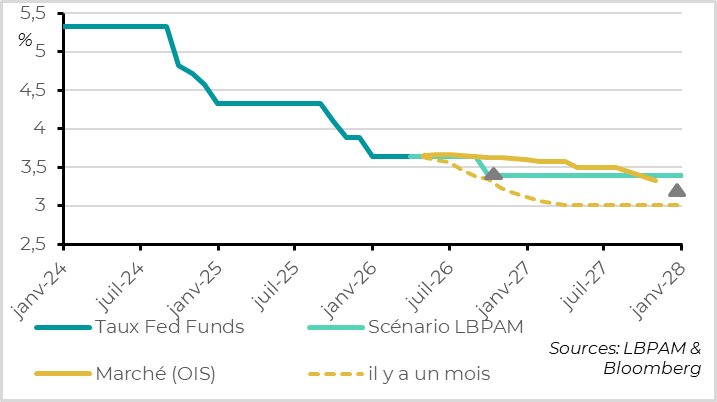

►On the Fed’s side, Powell reiterated that it will take time to assess the impact of the energy shock on the U.S. economy, without elaborating on possible scenarios. He also indicated that the Fed would need to see progress on inflation—particularly in the prices of goods affected by tariffs—before cutting rates. And while a majority of Fed members still expect a rate cut this year, they have also revised up their inflation outlook, growth projections, and their estimate of the neutral rate. We still believe the Fed could cut rates once this year, but probably not before the summer, and only if energy prices have clearly declined by then.

►The Bank of England’s tone is the one that has shifted the most, moving from a likely rate cut to possible rate hikes. The decision to keep rates at 3.75% was unanimous, whereas four members had voted for a rate cut in February. The reference to an upcoming easing was removed from the statement and replaced with the indication that the BoE ‘stands ready to act to ensure that inflation remains on track to return to the 2% target over the medium term.’ Yet the meeting minutes show that staff now expect inflation to be close to 3% this summer, whereas it had been expected to return to the 2% target. That said, Governor Bailey’s remarks remained fairly balanced. Overall, it is becoming likely that the BoE will not cut rates before the end of the year, although the three hikes currently priced in by the market seem rather aggressive.

►Finally, the Bank of Japan (BoJ) also kept its policy rate unchanged at 0.75%, but one member voted in favor of a hike, and the statement continues to indicate that the BoJ will raise rates if inflation evolves in line with forecasts. However, inflation could end up being higher if the energy shock persists. Ueda did not give any indication regarding the timing of the next rate increase but noted that further hikes were possible even if growth weakened somewhat in the short term. Overall, we continue to expect two rate hikes in Japan this year. It is now the only central bank for which we foresee higher rates than those currently priced in by the market.

Going further

ECB: ‘well positioned’ to raise rates if necessary

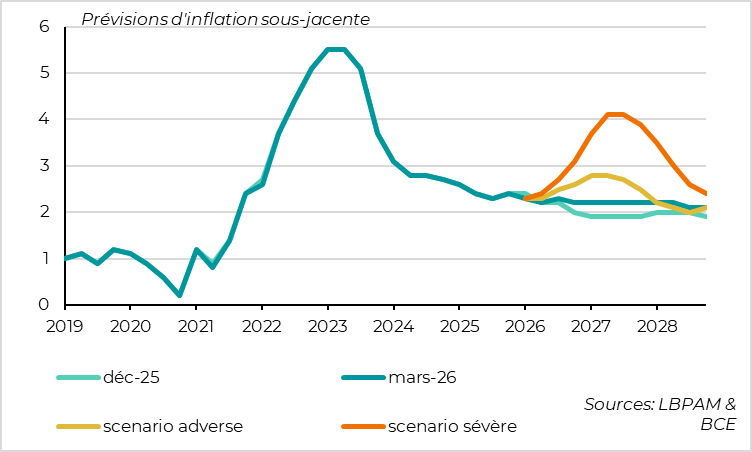

The ECB expects inflation to remain above target in all its scenarios

As we expected, the ECB kept its rates unchanged for the sixth consecutive meeting. The statement remained fairly neutral given the uncertainty (‘The war in the Middle East has made the outlook significantly more uncertain, creating upside risks to inflation and downside risks to economic growth’), and Christine Lagarde confirmed that the ECB stood ready to respond to rising energy prices, while avoiding giving the impression that it was in a hurry to raise rates immediately.

In summary, Christine Lagarde avoided saying—as she had in the previous two meetings—that the ECB is ‘in a good position,’ and instead stated that it is ‘well positioned’ to navigate the uncertainty.

That said, this meeting suggests that the ECB may be closer to raising rates than we previously thought. Or at least that it wouldn’t take a much larger energy shock for the ECB to trigger rate hikes relatively quickly.

Indeed, the statement notes, regarding the energy shock, that ‘its medium‑term implications will depend on both the intensity and duration of the conflict.’ And during the press conference, Lagarde suggested that if the shock were significant and prolonged, the ECB would not wait to see whether second‑round effects materialize before raising rates.

Furthermore, the ECB’s baseline scenario now projects that core inflation will remain above target through the end of the forecast horizon (at 2.3% in 2026, 2.2% in 2027, and 2.1% in 2028), whereas in the December projections it was expected to return to target this year. Growth has also been revised down, though only slightly and temporarily (from 1.2% to 0.9% for 2026). Notably, this scenario is based on early‑March energy prices rather than mid‑February, meaning it incorporates the impact of the war in Iran. This indicates that the ECB sees inflation risks as significantly greater than growth risks at the moment—justifying a more restrictive policy stance.

Finally, the ECB presents two alternative scenarios, both based on larger and more persistent energy shocks than in the baseline. These scenarios also confirm that the shock is more inflationary than recessionary. The bias in scenario design (no scenario of faster easing) and the balance of risks pointing toward inflation in all scenarios argue against waiting too long before raising rates.

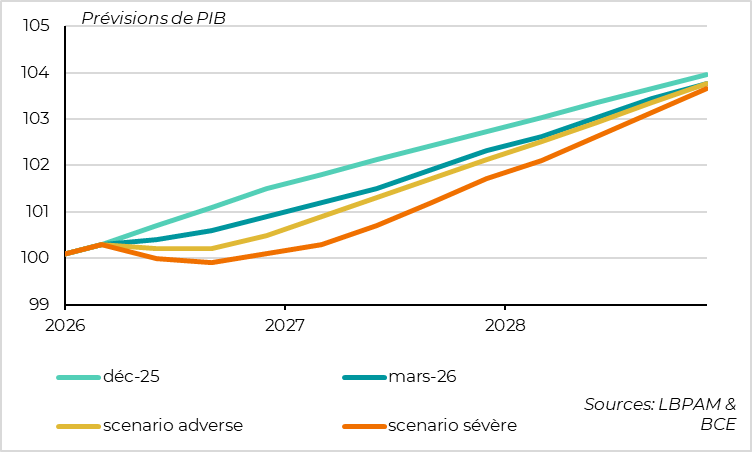

The ECB is optimistic about the economy’s ability to withstand the shock

In the adverse scenario, which assumes oil and gas prices reach USD 120/bbl and EUR 90/MWh in Q2–Q3 before gradually normalizing over the following year, the economy would avoid a recession (with only a mid‑year stagnation). At the same time, inflation would exceed 4% in the second half of the year, and core inflation would rise to 2.8% by early 2027.

In the ‘severe’ scenario, which assumes oil and gas prices of USD 150/bbl and EUR 110/MWh in Q2 and remaining high thereafter, the euro area would experience only a limited recession in Q2–Q3 and would almost fully recover thereafter. At the same time, inflation would exceed 6%, and core inflation would surpass 4% by early 2027.

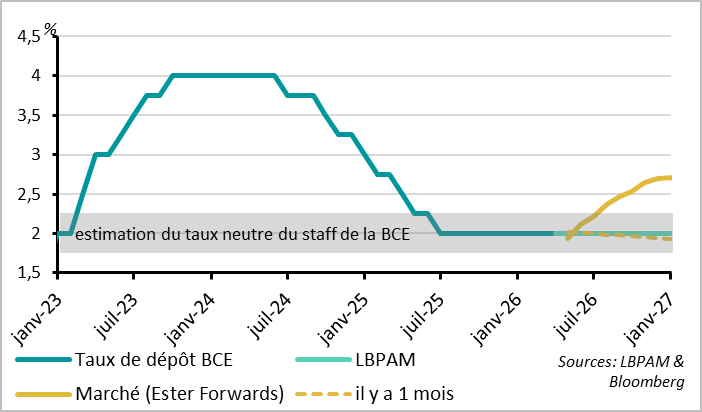

Markets now expect more than two rate hikes

Following the ECB meeting (and the renewed increase in energy prices), markets continued to price in additional rate hikes. They now expect more than one hike by June and more than two hikes by the end of the year.

For our part, we maintain our central scenario, which does not include a rate hike before next year, because our scenario assumes a fairly rapid decline in energy prices during the second quarter (faster than in the ECB’s baseline scenario). That said, the risk of the ECB raising rates before the summer is higher and more immediate than we previously thought. Indeed, it appears that if prices do not begin to fall significantly before the end of April, the ECB may consider rate hikes.

We remain positive on European rates, as the market is already pricing in a relatively aggressive ECB path, and because a stronger energy shock would increase recession risks, which would offset the additional inflation‑related pressure on long‑term yields.

Fed: more than ever in wait‑and‑see mode

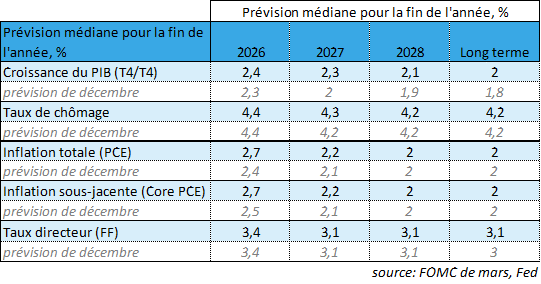

FOMC members revise up both inflation and growth

The Fed kept its policy rate unchanged at 3.5–3.75% for the second consecutive meeting, with only one member this time supporting a rate cut (still Governor Miran, appointed by Trump).

And unlike other central banks, it neither specified nor even discussed how it might respond to the ongoing energy shock. The statement remained almost unchanged, adding only that the impact of the Middle East crisis on the U.S. economy was uncertain. It maintains a fairly neutral stance, indicating that the Fed remains attentive both to upside risks to inflation and downside risks to employment. Powell temporarily closed the debate during the press conference, stating that ‘it is too early to know the scope and duration of the potential effects on the economy,’ before repeating four times that ‘we are just going to have to wait and see.’

That said, the meeting sent an overall message of a Fed less inclined to cut rates, for reasons unrelated to the energy shock.

In the well‑known dot plot, the median projection of Fed members still shows one rate cut this year and another next year, as in December. But seven of the nineteen members still do not expect any rate cuts this year, while only five now expect two or more cuts (compared with eight in December).

Moreover, Fed members revised up their inflation forecasts (even excluding energy) and their growth outlook, which does not argue for a more accommodative monetary stance. They also slightly raised their estimate of the neutral rate (from 3% to 3.1%), suggesting that current rates are only marginally restrictive.

Finally, Jerome Powell indicated that the Fed needs to see ‘progress on inflation’—particularly in goods affected by tariffs—before cutting rates later this year. This suggests that the threshold for resuming rate cuts is somewhat higher than before. He also noted that the impact of AI on GDP is positive (likely the reason long‑term growth estimates were revised from 1.8% to 2.0%), but that its impact on inflation is uncertain. This does not support the idea of preventive rate cuts based on expectations of a deflationary effect from AI, as some have hoped.

The market no longer expects any rate cuts this year

Overall, the Fed remains in wait‑and‑see mode in the short term (even more so given the uncertainty linked to the energy shock). It still maintains a slight easing bias, but one that is more limited and more conditional than before.

In our central scenario, we continue to expect one Fed rate cut this year, assuming the energy shock eases in the coming months and that the new Fed Chair is slightly more dovish than Powell. However, this cut is unlikely to occur before the end of the summer, and the risk that the Fed does not cut rates at all has increased.

In fact, the most interesting part of this meeting was probably the information Powell provided about his own future. He indicated that he would remain Chair of the Fed until his successor is confirmed by the Senate (and Warsh’s confirmation could be delayed beyond May), and that he would remain on the Fed’s Board at least until the end of the investigation launched by the administration. This suggests that Powell could retain significant influence within the Fed even after his term as Chair ends in May, which would limit his successor’s room for maneuver.

Xavier Chapard

Strategist