Will Iran and energy prices call the favorable economic situation into question?

Link

What are the key takeaways from the market news on March 06, 2026? Xavier Chapard provides some insights.

Overview

► The evolution of the situation in Iran and its inflationary impact through energy prices continue to dominate the markets. Uncertainty remains extremely high as bombings persist on both sides, the United States and Iran have clearly stated they will not back down, and the Strait of Hormuz is effectively almost closed, even though the Americans and some allies are working to restore open energy flows as quickly as possible. As things stand, oil and liquefied gas prices are up by 15 dollars per barrel (close to 85) and 15 euros per MWh (around 50), which is significant but relatively contained given the uncertainties.

►We are not experts in geopolitics, military affairs, or energy markets. However, given the rather unclear war objectives of the United States and the fact that the Iranian regime is now fighting for its survival, it seems to us that the fighting — and the negative impact on global energy supply — could last somewhat longer than in previous conflicts with Iran (perhaps a few weeks?).

Since market reactions have been fairly reasonable and uncertainty is likely to encourage central banks to adopt a wait-and-see stance, we remain cautious in the very short term.

That said, the risk of a major and lasting energy shock (similar to 2022) still seems limited to us, given the favorable fundamentals of the oil market before this shock and the political interests at stake (notably the upcoming U.S. midterm elections).

We therefore remain fairly optimistic about the macroeconomic outlook and markets over a 3–6 month horizon — especially as markets have historically rebounded very quickly once geopolitical risks begin to subside.

►Unsurprisingly in the face of an energy shock, European and Asian assets are significantly underperforming U.S. assets, and the dollar has emerged as the main beneficiary this week. These movements were also supported by investor positioning before the outbreak of the war, which had been dominated by themes such as dollar weakness, a shift from U.S. equities to the rest of the world, and the continuation of disinflation.

This explains why gold and long-term yields, which are usually safe-haven assets, have corrected this week.

Given the uncertainty surrounding future developments and the more neutral investor positioning after this week’s adjustments, we continue to favor geographical diversification and agility in our equity allocations.

►In any case, the economic data just before the Iranian shock confirmed a fairly broad-based improvement in the economic environment. The global PMI reached in February its highest level since mid‑2023 (53.3), consistent with global growth slightly above 3%, notably thanks to the recovery in the industrial cycle. In the United States, the services ISM surged in February above 56 for the first time since the start of the Fed’s rate‑hiking cycle in 2022.

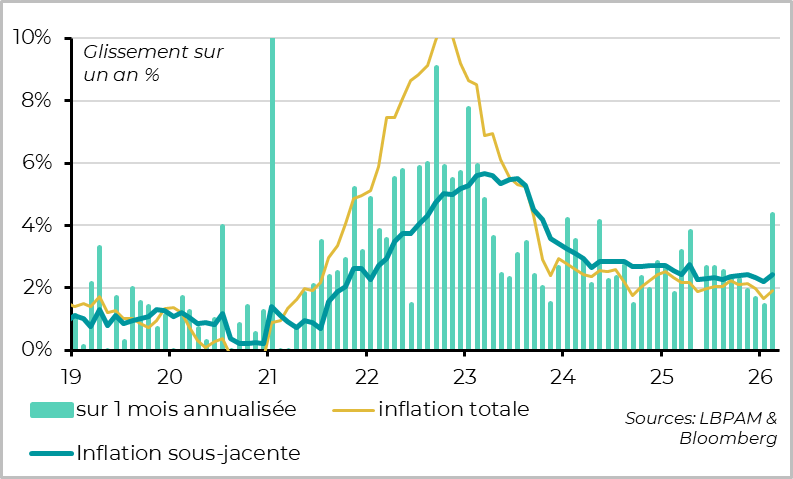

►In the Eurozone, inflation surprised to the upside in February, accelerating by 0.2 percentage points to 1.9% for headline inflation and 2.4% for core inflation. However, this negative surprise stems from temporary factors (the rebound in goods prices in France after the extended January sales, and the rise in services prices in Italy due to the Olympic Games).

The underlying trend remains consistent with inflation being close to target in the medium term, even though the recent increase in energy prices pushes back the prospects of inflation staying sustainably below 2% by 2027. Overall, the ECB should remain firmly on hold regarding interest rates.

►Chinese authorities slightly lowered the growth target for 2026, from 5% to 4.5–5%, as we had anticipated. This somewhat reduces long‑term risks by giving policymakers more leeway to gradually rebalance the economy — away from external demand and debt‑funded investment, and toward domestic demand and productive investment.

However, it also means that authorities are unlikely to announce a massive and broad‑based stimulus plan in the short term, which limits the upside potential for Chinese assets in the near term.

That said, we remain positive on Chinese equities, which in our view retain medium‑term rerating potential.

Going further

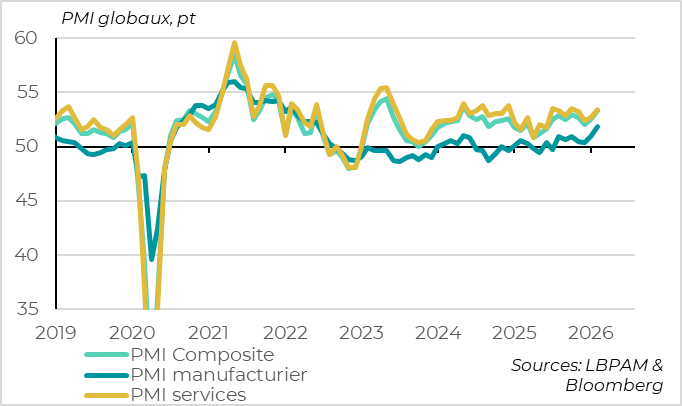

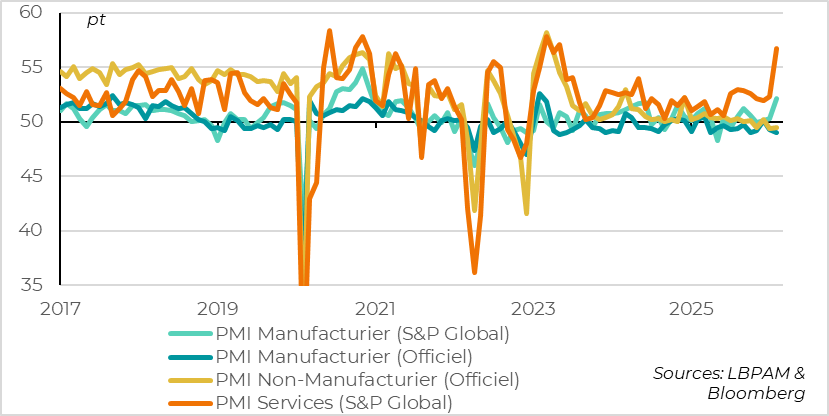

Global: Growth accelerated quite noticeably at the start of 2026

Global PMIs rose sharply in February

The global composite PMI, the best coincident indicator of world growth, rose sharply in February for the second consecutive month, reaching its highest level since mid‑2023. At 53.3, the index is consistent with global growth slightly above trend (3%).

And this early‑year rise in PMIs is broad‑based.

Both services and manufacturing PMIs increased by 1 point in February. The services PMI has returned to last summer’s highs at 53.4. Most notably, the manufacturing PMI reached its highest level since the mid‑2022 energy shock, at 51.9. This appears to confirm the recovery of the global industrial cycle, beyond just the tech sector. In addition, leading indicators (orders, expected output, etc.) improved in both sectors in February.

By country, S&P PMIs likely overstate the improvement in Chinese growth but also the weakening of the U.S. economy (see below). Overall, PMIs are rising in developed economies excluding the United States (in both Europe and Japan) and in emerging markets excluding China. The manufacturing PMI even increased in three‑quarters of the countries covered by the survey for the first time in two years.

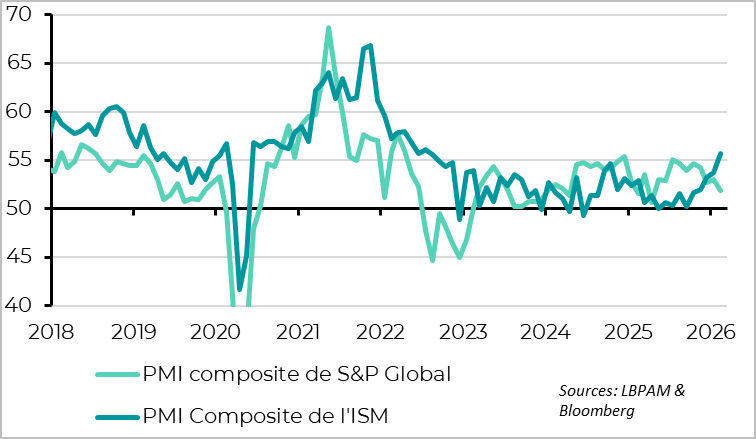

U.S. ISM surveys were very strong in February, which is reassuring

The only major disappointment in the S&P surveys is the U.S. PMI, which fell from 53 to 51.9 — its lowest level since last April’s tariff shock. But this disappointment is more than offset by the ISM surveys, which strongly surprised to the upside in February and suggest that business confidence is improving markedly after a slight slowdown at the end of 2025.

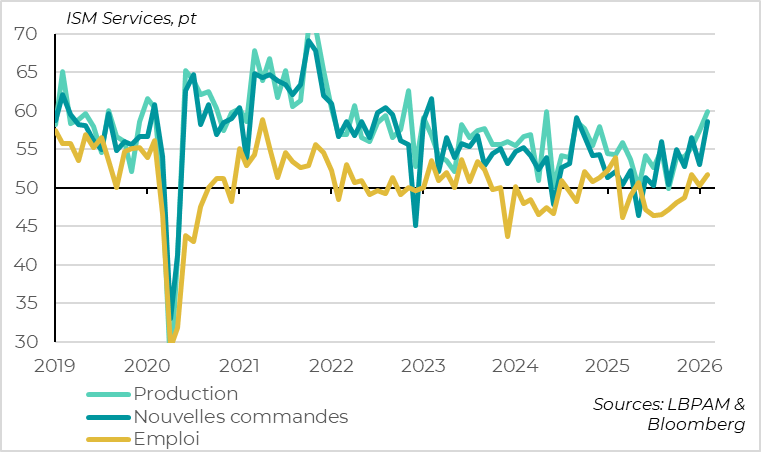

The ISM Services index jumped from 53.8 to 56.1, reaching its highest level since the start of the Fed’s rate‑hiking cycle in 2022. The details of the survey are solid.

The ISM Services index suggests that U.S. business confidence is recovering well

Beyond current output, orders also increased in February, including export orders. And the ISM price index fell to its lowest level since the start of the trade war, even if it remains high by historical standards.

Most importantly, U.S. service-sector firms confirm that employment is stabilizing. The ISM employment component clearly returned to expansion territory at 51.8, after spending nearly all of 2025 in contraction. Combined with the increase in private employment reported by ADP (+63,000 jobs in February) and with jobless claims stabilizing below last year’s levels, this confirms that downside risks to the labor market have eased in recent weeks.

The Fed’s Beige Book — the collection of anecdotes gathered by regional Feds before each FOMC meeting — also sends a reassuring message. It indicates that activity slowed only very slightly around the turn of the year, while employment remains stable and business confidence about the future is improving, notably thanks to reduced tariff fears.

The first data for 2026 therefore confirm the acceleration of global growth and the improvement in prospects beyond the tech sector at the start of the year, as we anticipated. Of course, the events in Iran and their consequences for the energy market could challenge the currently favorable environment. The risk is increasing by the day. But given the strength of the global and U.S. economies prior to the conflict, the energy shock would need to be both very large and long‑lasting to trigger a reversal of the global cycle. This is still far from being the central scenario.

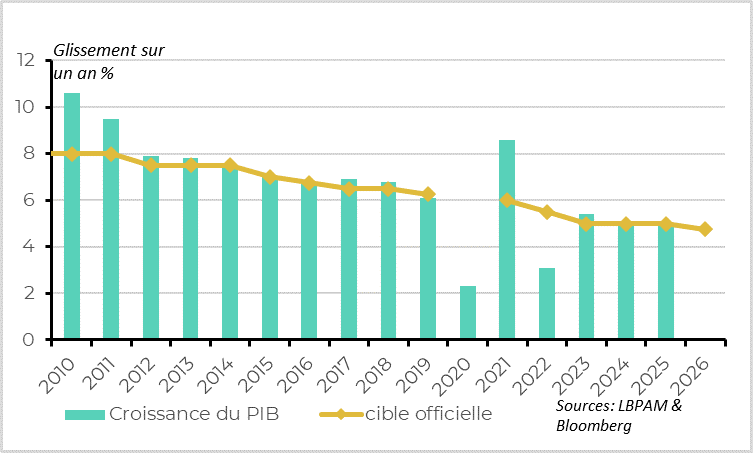

China: Authorities slightly lower the growth target for 2026

Authorities announce a 4.5–5% target after 5% in 2025

At the start of the ‘Two Sessions’, which will determine China’s economic objectives for 2026 and set the new Five‑Year Plan, the authorities announced a slight reduction in the growth target. They are aiming for growth between 4.5% and 5% in 2026, compared with 5% in 2025. This is the first decrease in the growth target since 2023 and marks the lowest target since 1991. But this is not a surprise, as it reflects the structural slowdown of the Chinese economy and remains more than sufficient to meet President Xi’s central objective of doubling China’s GDP between 2020 and 2035 (which requires at least 4.2% annual growth over the next 10 years).

On the one hand, this target remains relatively high while slightly reducing medium‑term risks. The authorities have maintained 5% growth for the past two years, but at the cost of widening imbalances that are increasingly unsustainable. For example, net exports contributed one‑third of growth — a level that is difficult for the rest of the world to tolerate now that China’s trade surplus exceeds 1% of global GDP. In addition, support for increasingly unproductive investment continues to push Chinese debt higher (now above 300% of GDP and higher than in most developed economies) and generates significant deflationary pressures. Premier Li acknowledges that transforming the economy is an ‘enormous’ challenge but one that is necessary given the ‘severe imbalances’.

On the other hand, accepting a lower growth target also means the authorities are unlikely to implement large‑scale stimulus measures. Instead, they will continue with targeted and incremental support policies. This is reflected in the other economic targets for 2026, which are not particularly ambitious. The inflation ceiling remains at 2%, but the authorities merely commit to ‘working to bring prices back into positive territory’ after three years of deflation. On the fiscal side, both the central deficit target (4% of GDP) and the quota for special bond issuance are unchanged as a share of GDP from last year, even though they remain very elevated. Finally, regarding real estate, the authorities still aim to ‘stabilize’ the property market rather than revive it.

Overall, we believe China should be able to achieve the 4.5–5.0% growth target this year without major difficulty, supported by targeted measures and strong export competitiveness (particularly after the rollback of reciprocal U.S. tariffs), even though the structural slowdown continues.

Chinese PMIs were very mixed in February

In the short term, China’s economic situation is hard to read, even though activity appears to be picking up slightly thanks once again to external demand.

The absence of hard data before mid‑March and the seasonal distortions linked to the Chinese New Year holidays always make China’s first‑quarter analysis difficult. But this year, uncertainty is further amplified by the wide dispersion in February’s PMIs.

On the one hand, private PMIs jumped in February after slight increases in January, reaching their highest levels since the post‑Covid reopening in both manufacturing (52.1) and services (56.7).

On the other hand, official PMIs stagnated after declining in January, remaining in contraction territory for manufacturing (49.0) and for the broader economy (49.5).

Overall, the average of the PMIs edged up slightly after falling in the second half of 2025, and we are placing somewhat more weight on private PMIs than official ones early in the year, as the latter are likely more affected by the slightly longer holiday period this year.

This is why we see the glass as half full for now — although this will require confirmation, and we expect more of a stabilization than a re‑acceleration of China’s economy this year.

Eurozone: Inflation surprised to the upside in February, due to temporary factors

Inflation rose sharply in February, surprising to the upside

Unlike in previous months, Eurozone inflation surprised to the upside in February, rising from 1.7% to 1.9%. While a slight increase was expected due to base effects from energy and headline inflation remains below 2%, the real surprise came from the acceleration in core inflation, from 2.2% to 2.4%. This reflects a 0.35% month‑on‑month increase in prices excluding energy and food — the strongest monthly rise in three years.

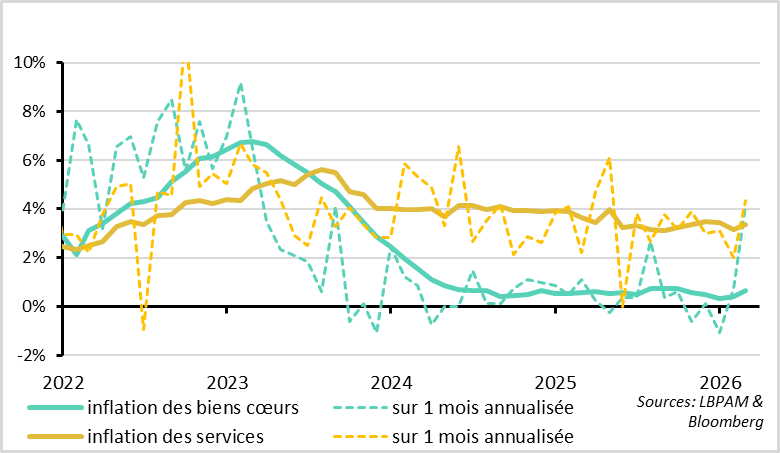

Both goods and services prices contributed to the upside surprise

The sequential acceleration in core inflation in February appears broad‑based, with both core goods and services prices picking up. However, it is actually being overstated by two components that should prove temporary:

Goods prices in France, which rebounded from −0.9% to 0.1% year‑on‑year. But this mainly reflects a normalization after unusually low prices in January, likely driven by the seasonality of extended winter sales. Industrial goods prices should not continue rising at the pace seen in February in the coming months.

Services prices in Italy, which jumped from 2.7% to 3.9% in February. This increase, concentrated in tourism (+6.1% for hotel and restaurant prices), is very likely linked to the Turin Olympic Games and therefore temporary.

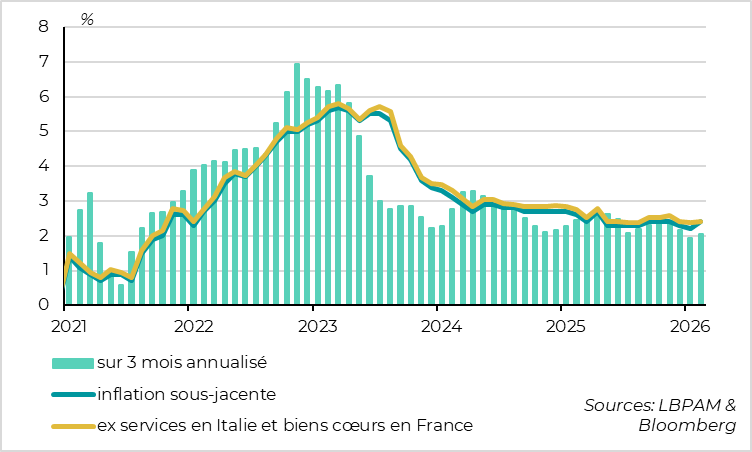

But the convergence of inflation toward 2% was not called into question before the shock linked to Iran

Overall, excluding services in Italy and goods in France, Eurozone core inflation was stable in February at 2.4%. And even fully accounting for the strong price increase in February, the three‑month trend in core inflation remains consistent with the 2% target. Finally, despite the temporary unfavourable factors in February, both headline and core inflation remain broadly in line with the ECB’s forecasts for the first quarter (1.9% and 2.4% respectively). In fact, the upside surprise in February merely offsets the downside surprises seen in December and January, leaving inflation prospects largely unchanged.

It therefore appears that Eurozone inflation was still on a slightly downward trajectory in February, one that should have brought it slightly below 2% during the course of this year. Of course, this was before the shock related to Iran, which increases inflationary risks through its impact on energy prices (oil and gas). That said, in a scenario where tensions and uncertainty remain elevated for several weeks but normalise relatively quickly after about a month, we estimate that the inflationary impact would be limited (around 0.3 percentage points on average in 2026), mostly concentrated in the first half of the year, and would spill over very little into core inflation. This would push back the prospect of core inflation falling below target to 2027, but would still remain consistent with the ECB’s scenario of inflation around 2% over the next two years. In such conditions, and given the high level of uncertainty, we think the ECB should be even more cautious in the near term and keep rates firmly unchanged.

Naturally, a larger energy shock (oil above 100 dollars per barrel) and, above all, a more persistent one (affecting energy supply for more than three months) would push inflation clearly away from 2% and would spill over into core inflation and possibly into inflation expectations. This would then force the ECB to consider rate increases. But this remains a risk scenario rather than the central one at this stage.

Xavier Chapard

Strategist