Convertible Bonds: A Dynamic Market at the Heart of Innovation Financing

Link

Christine Delagrave and Philippe Garnier, convertible bond managers at LBP AM, take a closer look at the dynamics of the convertible bond market. Following an exceptional year in 2025, they analyze the continuation of this trend in 2026, the factors supporting activity in the primary market, and the key role of this asset class in financing innovation.

After an exceptional year in 2025, is the momentum of convertible bonds continuing in 2026?

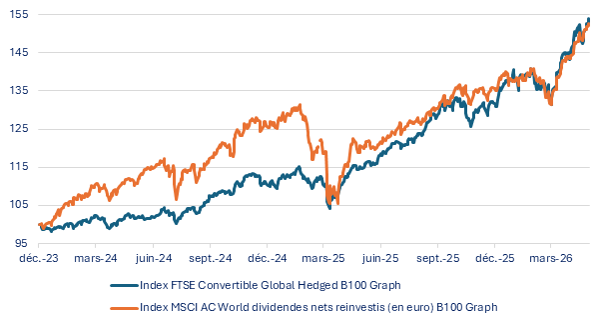

The answer is affirmative: the momentum in convertible bonds is continuing and even strengthening in 2026, following a remarkable year in 2025. Convertible bonds have maintained a strong performance trajectory, delivering approximately +16% in less than six months as of mid-June* (compared with +10% for the MSCI World).

Beyond performance, this asset class has demonstrated its ability to mitigate downside risk, reinforcing its relevance in environments characterized by market volatility and geopolitical uncertainty. As illustrated in the chart, in March 2025 — during “Liberation Day”* and the announcement of tariffs by the Trump administration — the MSCI declined by 18%, while convertible bonds showed greater resilience, with a more limited decline of 6.5%.

Similarly, in February 2026, despite heightened tensions in the Middle East and their impact on oil prices, convertible bonds remained resilient and delivered solid performance, in line with the MSCI World.

Sources: LBP AM, Bloomberg as of May 29, 2026. Past performance is not indicative of future results

Looking ahead to the end of the year, numerous events could impact markets, including the U.S. midterm elections this autumn and continued investment momentum. In this context, convertible bonds offer strong adaptability.

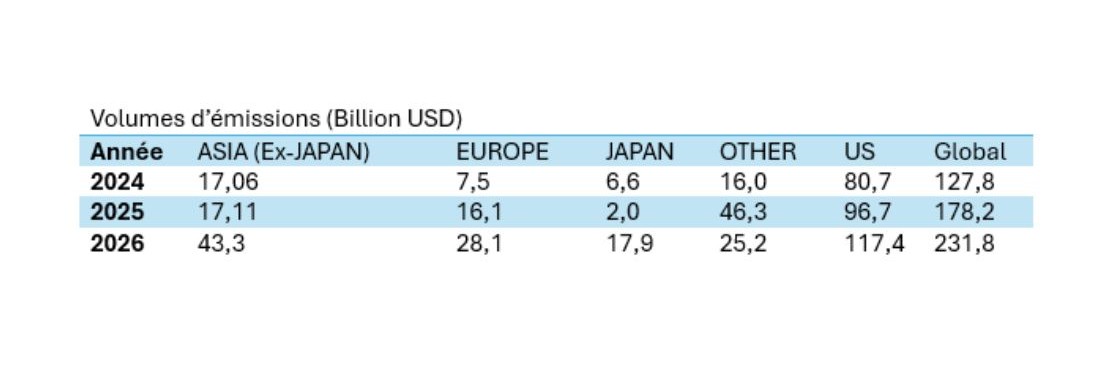

This dynamic is also clearly visible in the primary market, with issuance volumes rising sharply.

Global issuance has accelerated over the past two years, from $128 billion in 2024 to $178 billion in 2025, with nearly $232 billion expected in 2026 — representing annual growth of around 20%.

The market remains largely driven by the U.S., which continues to be the main engine. However, the momentum is now more global: Asia is accelerating rapidly - Europe is also showing a strong rebound.

The result: a deeper and more geographically diversified market

What factors explain the strong activity in the primary market?

In one word? Innovation.

This asset class naturally attracts growth and innovation sectors, making the convertible universe a mine of future themes.

In the 19th century, this asset class played a major role in financing railways, in 2000, in the creation of the internet, and in 2020, during COVID, in the digitalization of our economies.

In the current environment, financing needs are numerous and in strategic sectors... Whether it is defence, energy transition or technology, these instruments offer an attractive solution to companies seeking capital for their growth.

It is a mechanism that can be beneficial for both parties: the issuer benefits from a financing cost generally lower than a traditional bond, the investor, can participate, to some extent, in the upside potential of the equity if the project succeeds.

Convertible bonds therefore stand out as a preferred financing tool for innovation. And today, it is difficult to talk about innovation without talking about AI, the current technological revolution.

AI implies massive investments, and hyperscalers (such as Amazon, Google, Meta, Microsoft…) generate huge demand to develop data centers. But it goes far beyond that…

Let us not forget that while semiconductors, memory, and data storage are at the core of this revolution, data centers still need to be built, and around 50% of investments concern more traditional industrial needs: energy (electricity), cables, cooling systems, lasers, etc. This entire value chain constitutes, in our view, the main winners of this first phase.

It is on this value chain that we have chosen to focus our investments. However, not all players in this value chain will benefit equally, so it is important to be selective and rely on an experienced team.

Can you present your expertise in convertible bonds?

Our expertise is:

- More than €2bn in assets under management (as of end-May 2026)

- A first fund launched in 2004

- A senior team (with more than 20 years of average experience), supported daily by multidisciplinary analysts: credit, ESG, and equities, which allows us to obtain an in-depth analysis of companies.

- Proprietary tools and advanced quantitative research to support our investment decisions

- And finally, a responsible management approach, with all our offering labelled ISR V3*

Disclaimers / mentions légales à afficher: This promotional video has been produced for information purposes only and does not constitute an offer or solicitation, nor a personalised recommendation within the meaning of Article D321-1 of the Monetary and Financial Code, nor a provision of research, within the meaning of Article 314-21 of the AMF General Regulation, nor a financial analysis, within the meaning of Article 3, 1°, 35) of the EU Regulation No. 596/2014 of 16 April 2014 on market abuse (MAR), with a view to subscribing to LBP AM mutual funds. The information contained in this document is provided for information purposes only and has no pre-contractual or contractual value. LBP AM also informing the investor that it cannot be held responsible for any investment decision, whether or not it is based solely on the information contained in this document. Indeed, the investor's attention is drawn to the fact that: every investment has its disadvantages and advantages, which must be assessed in the light of each investor's individual and studied profile (desired return, risk that can be borne, etc.), and that, prior to any investment, and in order to avoid an investment in a UCI which does not correspond to his profile, the investor must carefully read the legal documentation of the UCI which is provided to him and, if he considers it necessary, must contact his adviser to obtain further information on the planned investment in relation to his own investor profile. This document is intended solely for the persons to whom it was originally addressed and may not be used for any purpose other than that for which it was designed. It may not be reproduced or transmitted, in whole or in part, without the prior written authorisation of LBP AM, which may not be held responsible for any use that may be made of the document by a third party.